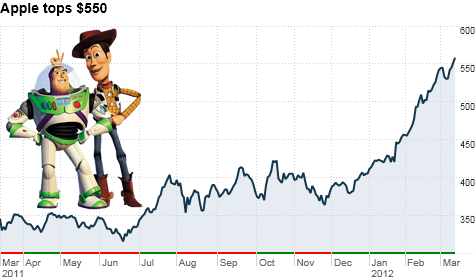

With Apple's stock climbing higher and higher, it may not be a shock if an analyst soon pulls a Buzz Lightyear and slaps an infinity target on it. Click chart for more on AAPL

NEW YORK (CNNMoney) -- Many investors thought Apple was due for a post-iPad sell-off last week. How could Apple live up to the considerable hype?

And when Apple finally unveiled its latest tablet simply as the new iPad, it seemed more likely that shares would finally fall from their lofty perch.

Nope. Shares of Apple hit a new all-time high Tuesday of about $560.

The stock is up 5% since CEO Tim Cook debuted the iPad nearly a week ago. Shares are up more than 10% since I last wrote a column on the stock, a fitting Valentine's Day ode to its greatness when Apple first topped $500. And Apple is now up 38% this year.

Still, Wall Street analysts continue to fawn over the stock. Jefferies & Co. analyst Peter Misek boosted his price target to $699 Tuesday morning.

Last week, Goldman Sachs analyst Bill Shope raised his target on Apple to $660. Barclays Capital's Ben Reitzes lifted his target to $710. And FBN Securities analyst Shebly Seyrafi upped his target to $730.

At this point, it wouldn't shock me if an analyst soon raised his or her price target on Apple to infinity. If Buzz Lightyear from the "Toy Story" movies were an analyst, his Apple target might even be infinity and beyond.

Is this finally getting a little ridiculous? Perhaps. Apple is now trading at a point where investors clearly expect earnings to top consensus estimates by a fairly wide margin.

Apple's stock price has outpaced the increase in profit projections from the start of the year. According to data from Thomson Reuters, analysts were expecting Apple to earn $34.67 a share for the fiscal year ending in September. The consensus forecast is now $42.86. That's an increase of "only" 23.6%

If stocks are supposed to track earnings, then you could argue that investors buying Apple now are likely expecting earnings of about $47.84 -- a 38% increase from the start of the year.

Can Apple hit that target? It seems doable. Earnings per share of $47.84 is nearly 12% higher than current forecasts.

But other than a blip where Apple missed estimates in its fiscal fourth quarter of 2011 -- the one that ended in September, which meant many consumers were waiting for the October release of the next iPhone -- Apple has routinely beat consensus earnings targets by much more than 12%.

So after all is said and done with Apple, the stock is only slightly more expensive now -- trading at about 13 times earnings estimates for 2012 -- than where it was a few weeks ago. And that's still a low multiple for a high growth stock.

As long as investors aren't getting ahead of themselves with expectations for just how robust new iPad sales will be, the stock may still have room to run.

Keep in mind that no legitimate competitor to Apple has emerged in the tablet race either. Research in Motion's (RIMM) PlayBook has been an unmitigated flop. And the tablets running on Google's (GOOG, Fortune 500) Android, such as the Xoom from soon-to-be Google subsidiary Motorola Mobility (MMI) and the Galaxy from Samsung, have failed to make a dent in the iPad's sales either.

Sure, Amazon's (AMZN, Fortune 500) Kindle Fire may do well thanks to its bare-bones approach and lower price point. It's not trying to be more sexy than the iPad. But the Kindle is more a Dr Pepper to iPad's Coke as opposed to being Pepsi.

Finally, It's also worth remembering that Apple is likely to launch other new products -- like the still (for now) mythical iTV. And any revenue and earnings from yet-to-be-released iThingys may not yet be factored into estimates.

I hate to sound like an apologist for Apple's constantly rising stock price. Yes, the pace of appreciation will inevitably slow ... but it may not substantially do so until Apple's earnings growth rate finally cools off.

And for all the bears who think this can't end well, I just don't see how that's the case. I covered the tech crash of 2000. This is not remotely similar.

Apple is producing real tangible products that people want to buy, and it is generating gobs of cash and profits in the process.

It's not a hype-fueled stock hoping to "monetize eyeballs" through online advertising, cash in on B2C (or even better B2B) e-commerce, or ride the wave of any of the numerous other empty tech buzzwords of the dot-com bust. Remember when Internet incubators were hot and the New England Patriots played at CMGI Field? Oy.

If you want to cry about tech stocks at unreasonable valuations, look at the current crop of social media stocks. Facebook at a $100 billion valuation as soon as it goes public? Please.

But don't call Apple a bubble.

Best of StockTwits: A rare earth miner is popping on news that the U.S. and Europe want to crack down on China's export restrictions. And Urban Outfitters (URBN) is showing how tough and fickle the business of retail can be.

MWM: $MCP this is rediculous, Rare Earth talk all over the news, why selloff? Shorts trying their best to keep it under $30...

The shorts don't appear to be winning anymore. Molycorp (MCP), a leading miner of rare earths in the U.S., reversed the day's earlier losses and was up nearly 5% in late morning trading to above $31.

I discussed Molycorp more in today's Buzz video. But it appears investors are betting that if the U.S. and other nations are successful in getting China to export more rare earth minerals, that should ease some supply concerns and benefit Molycorp. But are traders also betting on a takeover?

Julian_SanDiego: good opportunity for a japanese company to acquire $MCP given strong yen and to limit dependence on chinese rare earths, possibly hitachi.

Interesting. Not sure if this deal will get done but more Japanese companies are purchasing U.S. assets. An arm of Sumitomo announced Tuesday it is buying auto repair chain Midas (MDS). And on Monday, health care equipment company Zoll Medical (ZOLL) agreed to sell out to Japanese chemical conglomerate Asahi Kasei.

OptionsHero: $URBN turning into the Best Buy of the retail world. crappy layout, horrible selection, and bad customer service...hmmm.

TALENTEDBLONDE: $URBN VERY close to repeating the sins of $ANF. What was once cool and differentiated is tired . . .and EXPENSIVE.

I thought Best Buy (BBY, Fortune 500) was the Best Buy of the retail world. But I get the point. And Abercrombie & Fitch (ANF) is not exactly a flattering comparison either.

It just shows that being a top-notch retailer may be even harder than staying on top of tech. You have to constantly reinvent yourself and competition is brutal ... all for the "reward" of tiny profit margins. Retail is not the business for me.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()