|

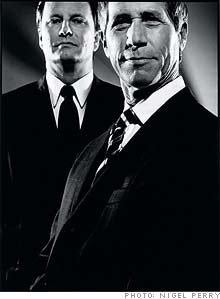

Last of the indies Lions Gate, which brought you Crash, is the hottest little movie studio in Hollywood. Now buyout rumors are swirling. Can it still survive on its own? Does it want to? (Fortune Magazine) -- The movie is bad, and everyone in the screening room knows it. But Jon Feltheimer, CEO of Lions Gate Entertainment, isn't fazed. "Just because it sucks doesn't mean we can't make a few bucks with it," he says. He turns to Peter Block, head of acquisitions: "What kind of deal are they offering? With that kind of opportunistic thinking, Feltheimer and vice chairman Michael Burns have built nine-year-old Lions Gate (Charts) into the Southwest Airlines (Charts) of the movie industry: a disciplined, no-frills, profitable independent studio. Last year the 18 films the company released grossed $344 million at the nation's box office, and 15 of them made a profit, a phenomenal success rate in Hollywood.

The slasher Saw II (tag line: "Oh yes, there will be blood") cost $6 million to make but grossed $87 million. Actor-director Tyler Perry's comedy "Diary of a Mad Black Woman" cost $5.5 million to make and brought in $50 million. The ensemble drama "Crash," which Lions Gate acquired for $3.3 million, generated $54 million and, as you may have heard, beat out odds-on favorite "Brokeback Mountain" to win the Academy Award for best picture last March. The all-business Feltheimer and the decidedly more Hollywood Burns "are quite simply the best in the business," says Sherry Lansing, former longtime head of Paramount Pictures. "They aren't afraid to take a chance, nor are they afraid to bring fiscal discipline to a business that, well, doesn't tend to do business that well." Indie budgets Lions Gate keeps its bets small, producing or acquiring inexpensive niche pictures. It markets them cheaply but aggressively and relies on one of the industry's largest film and TV libraries to provide enough cash to ride out the ups and downs. It's a smart plan, and Feltheimer and Burns have executed it well. Their biggest problem now could be too much success. Smart little studios have a way of first prospering and then flaming out. That's what happened to two other guys who came to Hollywood and made it big playing the movie business version of small ball. Bob and Harvey Weinstein's Miramax Films started with little pictures. But as the Weinsteins succeeded, they began to make progressively larger bets each time out. When you bet big, you can lose big. Miramax's "Cold Mountain" and "Gangs of New York" were both star vehicles that cost more than $100 million to make and lost money. Lions Gate now finds itself at much the same crossroads (although temperamentally Feltheimer and crew couldn't be more different from the famously egocentric and hands-on Weinsteins). Should Lions Gate stick with what has worked, or does it double-down and play the game the way the big studios do? Or do they try to sell the business? Long a subject of takeover speculation, Lions Gate has attracted suitors but no bridegrooms. Recently Carl Icahn bought a 4% stake in the company. "For us, it's about where do we go from here?" says Steve Beeks, the company's president. "We've done a lot, but there is only so much we can do with our current businesses. We're making 18 films a year. Maybe we could do 20, but the whole place would creak. Television can grow from $140 million to $200 million, but that's overly optimistic. And we're not going to produce $50 million pictures. So we're pretty much maxed out." A few minutes later, three doors down in Lions Gate's cramped, nondescript, and very unglamorous Santa Monica offices, Feltheimer hears about Beeks's remarks, spins around in his chair, and shouts to his assistant, "We need to start a job search for a new president!"-and chuckles. But he doesn't seem all that amused. "Really, he said that? I don't agree with that at all." Buying into the business The Lions Gate story starts like that of most other independent film companies: Rich guy wants to be a Hollywood player. Usually these stories end rather quickly-with an empty bank account. Canadian investment banker Frank Giustra founded the company in 1997 and took it public the following year. Lions Gate, named after a landmark Vancouver bridge, even had some hits, notably American Psycho and Dogma, but it was far from profitable. In late 1999, Michael Burns, the gregarious former head of Prudential Securities' (Charts) Los Angeles office, joined the company's board. It was through Burns that Lions Gate came to the attention of Gordon Crawford, media stock investor for Capital Research & Management and an old fly-fishing buddy. Crawford, famous for having advised the likes of Sumner Redstone and Ted Turner, proposed that Lions Gate should raise cash from Wall Street, then use it to build a film library by buying smaller companies. Revenue from the library would generate cash flow to fund the production or purchase of new movies. (One problem with the film business is that while it takes a lot of upfront money to produce and release a film, it can be years before returns filter back.) Even better, as the library grew and became more valuable, it would make Lions Gate a desirable acquisition for a big entertainment industry player. It just so happened that at about the same time, Crawford was doing some career counseling for Feltheimer, who had recently resigned as head of Sony (Charts) Pictures Entertainment's television operations. Crawford put him together with Burns, and they quickly lined up a $33 million preferred stock offering and a $200 million credit line. (Giustra stepped down as president in 2000 and left the company in 2003.) Their first move was spending $50 million for Trimark Holdings in 2000, a Marina del Rey, Calif., studio whose films included the Leprechaun horror series. Lions Gate had a harder time earning credibility with producers, not to mention actors and directors. Cassian Elwes, co-head of the independent-film division of the William Morris Agency, remembers that it was even hard to find its office. "You had to know to turn left at the Jiffy Lube on the corner," he says. He tried to interest them in the drama Monster's Ball in 2000 only after every other studio had said no. Initial signs for the picture, which Lions Gate made for $4 million and which opened at the end of 2001, weren't good: Reviews were mixed, and the movie was showing in only two theaters. But as word of mouth spread and Halle Berry won the Academy Award for best actress, it became a hit, eventually showing on almost 1,000 screens and grossing more than $30 million. Making the cut More important, that success made it possible for Lions Gate to get the credit to buy the larger Artisan Entertainment, locking up a catalog that includes "Basic Instinct," "Total Recall," and "Dirty Dancing." "If we were debutantes, that [film] would have been our coming-out party," says Burns, "and Halle Berry would have been queen of the ball." In the spring of 2004, Michael Paseornek, who heads film production at Lions Gate, was looking through a tall stack of scripts in his office. One caught his eye. It had a note scribbled by an agent that read, "Tyler Perry has sold $100 million in DVDs." Tyler Perry? $100 million? None of the Hollywood insiders he quickly called had heard of Perry either. "Then I asked one of our black employees," says Paseornek. "'Oh, yes,' he said. He had seen every one of his DVDs and been to dozens of his plays." It took only a couple of days for Lions Gate to green-light Perry's first theatrical film. Three months later it was being shot. Convinced that Perry was a hot property, Lions Gate green-lit his next movie before the first one opened. That first movie, "Diary of a Mad Black Woman," in which Perry plays a gun-toting, pot-smoking grandmother, opened as the No. 1 film at the nation's box office, eventually grossing more than $50 million. The second film, "Madea's Family Reunion," did even better, pulling in $63 million. (Lions Gate is aiming for black audiences again with the upcoming Pride, starring Terrence Howard and Bernie Mac. Based on a true story, it's about a top swim team composed of inner-city Philadelphia kids.) Lions Gate moves fast and inexpensively. It makes and markets most of its movies for under $20 million, compared with the $100 million industry average. Lions Gate will usually acquire only finished art films, for example, because of the higher risk of execution. And even then it won't shell out much more than a couple million. "What we're really good at is figuring out how to position ourselves to make money most of the time, and if we lose money, not lose a lot," Burns says. Too hot to handle The studio has proved adept at making hits out of projects others don't want to touch. Take "Hostel," for example, a horror picture in which European bad guys attack touring American college boys with power tools. Sony had Lions Gate distribute it because it was so violent. (It later grossed almost $50 million.) And then there's "Saw," released in 2004, which begins with two people chained to a rusty pipe with only a handsaw to attempt escape. (The saw is too weak to break their steel shackles but just about right for flesh and bone.) Little money was spent on television or newspaper ads for the movie. Instead, Lions Gate created an Internet site that put fans into scenes from Saw, with the question "How fucked up is that?" It flooded comic-book and horror conventions with posters bearing images of severed limbs. It even organized an actual blood drive, advertised with a poster of a sexy nurse (actually a Lions Gate marketing executive) who was drenched in blood. Perhaps the topper was an amputee beauty pageant on Howard Stern's TV show. "My only rule is, don't get arrested," says Tim Palen, Lions Gate's co-president of theatrical marketing. All told, "Saw" cost $1 million to produce and $18 million to market. It made $55 million at the box office and spawned a lucrative franchise. (DVD sales have already topped $70 million.) "Saw II," which opened exactly one year after the first film and cost $6 million to make, trounced "The Legend of Zorro" (which cost an estimated $75 million) at the box office. "Saw II" brought in $87 million in theaters and another $90 million in DVD sales. "There is no one else in Hollywood who could have made and marketed these films better," says Saw producer Mark Burg, taking a break from the set of Saw III, which will be released on Halloween. "There are even Saw conventions now." Not every stunt has paid off. Take Lions Gate's recent movie "Akeelah and the Bee," about a young girl from the inner city who dreams of winning a national spelling bee. Lions Gate made it for $8 million and made a deal with Starbucks (Charts) to promote the movie in its 5,185 U.S. stores, a first for the coffee retailer: green drink jackets with spelling words, flash cards on the walls, baristas who had seen and could talk up the movie. But "Akeelah" brought in only $6.3 million on its opening weekend, and market surveys showed the Starbucks campaign had had little effect. (Still, the studio expects a small profit.) Lions Gate has been protected from box-office disappointments by the revenue generated from its film library, which pulls in more than $200 million each year - enough to cover the company's annual overhead. But as DVD sales flatten and the number of new libraries left to purchase dries up, the question arises: How can Lions Gate keep its cash flow, its lifeline, from drying up too? More important, how can it continue to grow? One way is to start making bigger movies with bigger potential upside - call it the Miramax model. Another way is to start growing by acquiring other lines of business, such as TV syndication. Both have a fundamental risk: They start to make Lions Gate into something it has never wanted to be - big. The studio has shown some signs of diverging from its original business plan, like building its own production studios in New Mexico and going ahead with a $35 million movie with martial-arts action star Jet Li. Small is beautiful Feltheimer and Burns insist they aren't breaking from the "small is beautiful" model that has worked so well for them. They point out that Lions Gate will risk less than $10 million on the Jet Li picture (they've presold the foreign rights and brought in partners) and that real estate partners and the state of New Mexico are paying most of their studio construction costs. "We have $200 million in the bank," says Feltheimer. "The possibilities are endless." All that leaves Wall Street generally bullish on the company but split on whether it's fully valued or not. The stock is down 25% from last year, when it hit its all-time high of $11.63. The most optimistic analysts now have $13 to $15 price targets. That's been a rumor for years; Paramount has twice considered buying it but balked at the pricetag. But after corporate raider Carl Icahn revealed he'd amassed a 4% stake in Lions Gate in May, sale rumors started all over again. While Icahn won't comment, he's probably mainly interested in the value locked up in the company's 5,500-title library, by far its most valuable asset. Viacom (Charts) sold DreamWorks' 59-title library to a group led by Soros Strategic Partners for $900 million earlier this year. And in late 2004, Sony and a group of partners paid $4.8 billion for MGM's 4,000-title library. Using the same valuation method, Lions Gate's library would be worth about $960 million - more than the company's market cap at the moment. "[Icahn] simply wants to make money," says David Miller, an analyst with Sander Morris Harris. "This is the last remaining public film library. He recognizes the scarcity value of these assets." Feltheimer says no deals are imminent but adds, "We've had a number of conversations with Icahn, and our sense is that they believe our company is undervalued. They put a lot of value on the library, and we agree." For all this talk of assets and valuation, though, there are and always have been some aspects of the movie business that can't be reduced to items on a balance sheet. Like charm, or the halo effect that comes from being considered hot. Take Burns' wedding bash a few weeks ago at Hollywood's famed Chateau Marmont hotel. That was reserved for 400 friends: Jackson Browne on the microphone. Kevin Spacey on a couch. Sushi from Matsuhisa. Champagne everywhere. One A-list movie star said, "Look around. Everyone here wants to work for them. Everyone here wants to be their best friend. How often do you hear that about independent studios who pay crap?" From the July 24, 2006 issue

|

|