NEW YORK (CNNMoney) -- The nation is just days away from the debt ceiling deadline, and no one knows exactly what will happen when the borrowing limit is reached. But even in the worst case scenarios, many experts think investors will flock to U.S. Treasuries.

That possibility would mean lower borrowing costs for the government, not the spike in interest rates that many were expecting.

"Intuitively, this might not make sense because you would think there would be selling of Treasuries, but instead the Treasury market is well-supported," said Richard Bryant, head of Treasury trading at MF Global.

The experts admit they're not sure how markets will react if there is no solution by the Aug. 2 deadline. But many believe that stocks will suffer more in the uncertainty caused by a debt ceiling crisis.

"We'll have a liquidation of risky assets and a flight into quality," said Kim Rupert, Managing director of Fixed Income for Action Economics. "There really isn't an alternative [to Treasuries]."

U.S. Treasuries are such a massive market -- about $9.8 trillion -- that they dwarf the markets of other so-called "safe havens" such as gold, top-rated corporate debt or the bonds of other countries with AAA ratings.

And the expectation that the U.S. Treasury will continue to pay the principal and interest payments owed on existing debt, even in the case of a prolonged deadlock, will give investors a sense of confidence, even if there is a downgrade.

"I don't think a rating change will fundamentally change anyone's view about the likelihood of being paid back on Treasuries," said Josh Fienman, chief economist DB Advisors. "They will continue to think that Treasuries are 'money- good.'"

Fienman said that the U.S. debt ceiling crisis is widely viewed as less serious than the lingering worries about European sovereign debt. He said the U.S. needs to address its long-term government deficits, but that is a problem that needs to be solved in the coming decades, not coming days.

"This is a self-inflicted crisis. No one in the market is unwilling to lend to the U.S., " he said. "Some people find it galling, but no matter what the U.S. does, it's able to borrow at extraordinarily low interest rates."

Some worry about whether foreign investors will sour on U.S. Treasuries if there is a crisis. But countries with huge holdings of U.S. debt, such as China, have an interest in making sure that bonds stay strong during a debt ceiling crisis so as not to hurt the value of their existing holdings.

"We suspect that China would quickly pledge to continue purchases of Treasury securities, just as it has done for debt issued by governments in the eurozone, given the even greater risks to its own wealth from a financial meltdown in the U.S.," said Julian Jessop Chief International Economist for Capital Economics in a note Thursday. "China's own rating is currently AA-, so it would be odd for Beijing to make a big deal of a downgrade that would almost certainly still leave the U.S. rating higher."

A prolonged debt ceiling deadlock could quickly cause the government to stop making other payments , cutting paychecks to federal workers, contractors and citizens depending on payments such as Social Security.

Analysis by the Bipartisan Policy Center estimates that cut in spending could come to $134 billion in August alone, roughly the equivalent of cutting annual spending by $1.6 trillion. And that slashing in spending has many economists worried that the crisis could spark a new recession.

But a recession, while terrible for stocks and a country as a whole, can be good for bond prices, which move in the opposite direction of bond yields. Lower inflation expectations that typically accompany a recession lowers the returns that investors demand on a nation's debt.

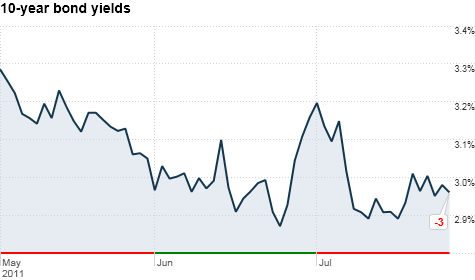

The record low yield for the 10-year Treasury of just above 2% came in December 2008, when the country teetered on the edge of a new depression. Rupert said yields could approach those lows, nearly a full percentage point below current levels, if another recession starts.

One other factor that could lift bond prices is that Treasury could be forced to stop selling new bonds, which would limit the supply available for investors. Limiting supply typically helps to lift prices.

Thursday's auction of 7-year Treasuries came in with a yield of 2.25%, the lowest rate Treasury has had to pay for notes of that term since last November.

-- CNNMoney's Blake Ellis contributed to this report ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates:

| Latest Report | Next Update |

|---|---|

| Home prices | Aug 28 |

| Consumer confidence | Aug 28 |

| GDP | Aug 29 |

| Manufacturing (ISM) | Sept 4 |

| Jobs | Sept 7 |

| Inflation (CPI) | Sept 14 |

| Retail sales | Sept 14 |