NEW YORK (CNNMoney) -- If the Obama administration really wants to save the housing market, it should speed up the foreclosure process -- not prolong the inevitable, experts say.

Four years into the housing crisis, the real estate market is still teetering on the edge. The Obama administration has tried one program after another to stem the tide of foreclosures with limited success. And it is continuing to look for ways "to ease the burden on struggling homeowners," though no new initiative is imminent, the White House said this week.

But some housing experts argue that the administration should go in a different direction than it has in the past. Instead, they say it's time to focus on pushing many of those delinquent borrowers through the foreclosure process and putting foreclosed properties back into use.

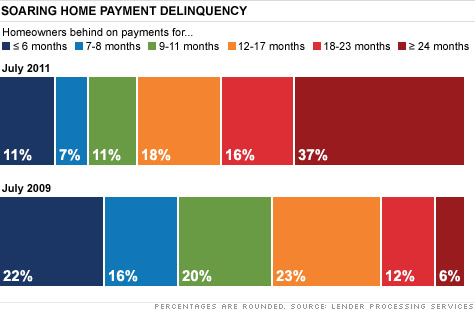

While some of the 2.2 million loans in foreclosure can still be saved, many are too far gone, they say. Some 37% have not made a payment in more than two years, while another 34% have not made a payment in 12 to 23 months, according to Lender Processing Services.

"Loans enter into foreclosure, but never come out," said Thomas Lawler, founder of Lawler Economic & Housing Consulting. "If this keeps going on, you have a continual overhang that never goes away."

Delaying foreclosure increases the percentage of homeowners who'll likely never catch up, Lawler said. In 2009, only 6% of delinquent borrowers were more than two years behind. And it means vacant properties still in limbo could fall even further into disrepair, hurting the value of the surrounding housing market.

Lawler is not the first to warn about the consequences of slowing the foreclosure process. Since the housing crisis began, several experts cautioned that foreclosure prevention efforts may only prolong the pain.

Accelerating foreclosures is tricky, however, especially since it is largely the purview of the states. But the administration could work with state officials to speed the process, especially on vacant homes, he said.

The push would come at a time when many mortgage servicers have slowed foreclosure efforts as they resolve shoddy paperwork practices. Foreclosure filings in July dropped to their lowest level since November 2007, due to processing delays and foreclosure prevention measures, according to RealtyTrac.

Another key to helping the housing market is facilitating the resale of homes that have already been foreclosed upon, experts said. This glut of vacant properties will continue to weigh on home values until they are sold.

"They can't be a glacier hanging over the market with everyone waiting for it to fall," said Jim Gaines, research economist at The Real Estate Center at Texas A&M University. "Those properties have to clear the market."

A first step could be to sell off the foreclosed properties owned by Fannie Mae, Freddie Mac and the Federal Housing Administration. Collectively, they own 248,000 homes, about 31% of the foreclosure inventory.

The administration and the Federal Housing Finance Agency, which regulates Fannie Mae and Freddie Mac, are already looking for ways to unload these foreclosed homes. Earlier this month, they put out a request for ideas, including possible bulk sales of inventory. Also, they are interested in turning many of these properties into affordable rentals, which are sorely lacking in many communities. Experts interviewed agree this would be a good move for the market.

To entice investors to purchase these homes, as well as other foreclosed properties owned by banks, the administration could advocate for changes to the tax code, Gaines said. For instance, more favorable capital gains or depreciation rules could attract buyers.

Of course, not everyone agrees that pushing people through the foreclosure process is the best solution to the housing crisis.

David Min, associate director for financial markets policy at the Center for American Progress, argues that there are many homeowners who can be saved if their payments can be adjusted to affordable levels or if some of their principal is forgiven. This particularly applies to those who are only a few months behind.

Foreclosure is very costly for servicers, homeowners and neighborhoods, he said.

"There are a lot of other options that make more sense" than foreclosure, Min said. "It's just so destructive to value. We should be pulling every lever we can."

Mediation, for instance, could help some homeowners avoid foreclosure, he said. Some 23 states and the District of Columbia currently have programs that require mortgage servicers to sit down with borrowers and discuss the homeowners' options, though many began only in the last year. More than 70% of mediations end in a settlement, often restructuring the mortgage to a sustainable level, according to the center.

Helping those still current with their payments can also give the housing market -- and the economy -- a lift, albeit a somewhat marginal one, experts said.

For instance, the administration could revamp its refinancing program aimed at allowing underwater homeowners to take advantage of today's lower interest rates. Improvements could include reducing some of the upfront costs and underwriting requirements.

Lowering borrowers' monthly payments would give people more money to spend. And, for those on the edge, it could make it more likely that they will stay in their homes.

"It would be helpful to some borrowers with high rates," Lawler said. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: