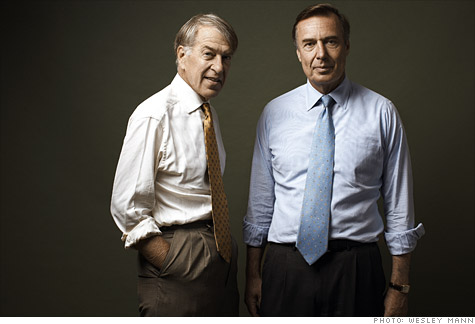

Roger Altman (left) launched Evercore in 1995 and shed the CEO title in May of last year when Ralph Schlosstein (right) took it and quintupled assets under management to $15 billion.

Roger Altman (left) launched Evercore in 1995 and shed the CEO title in May of last year when Ralph Schlosstein (right) took it and quintupled assets under management to $15 billion.

FORTUNE -- It's been a miserable few years for investment banks. Between epochal meltdowns, shotgun marriages, a federal pay czar, congressional investigations, reform legislation, and SEC lawsuits, even the proudest firms have been flayed (often for good reason). One of the less publicized results of that tumult has been an exodus of talent. But many bankers aren't fleeing Wall Street -- they're fleeing to the other side of the Street: small boutique firms that eschew the proprietary trading and lending to their clients that the giant banks emphasize. These younger firms hark back to a venerable model of financial firms, selling only advice.

The biggest and fastest-rising of these outfits is Evercore Partners (EVR), headed by Roger Altman, the ultraconnected former U.S. Treasury official, and Ralph Schlosstein, a superstar who joined the firm last year from BlackRock (BLK, Fortune 500). Evercore shuns risk -- no trading for its own account, no lending -- and prides itself on avoiding everything that brought the Citigroups (C, Fortune 500) and Goldman Sachses (GS, Fortune 500) to grief. Instead, Evercore's main service is providing advice to CEOs on mergers and restructurings.

Its success marks a major shift in the balance of power on Wall Street. Says Ed Nicoll, ex-CEO of Instinet, who enlisted Evercore on its $1.2 billion sale to Nomura in 2007: "The crisis badly tarnished the reputations of the big banks. Now the very best bankers are crossing the street to join the Evercores, and their best customers go with them."

Lest you think that a firm with just $314 million in revenue is a bit player, look at Evercore's megadeals. In 2009, Evercore worked on the year's largest merger, counseling Wyeth on its $65 billion sale to Pfizer (PFE, Fortune 500); the biggest restructuring, guiding the $80 billion rescue of General Motors; and the highest value leveraged buyout, representing private equity shop TPG in its $5.2 billion acquisition of IMS Health.

From the start of 2009 to mid-2010, Evercore ranked seventh in the U.S. in the total value of its M&A deals, ahead of Credit Suisse (CS) and Deutsche Bank (DB). It accomplished that with a mere 48 senior bankers, one-tenth the total in most big shops. Overall, the boutiques, a group that includes such names as Houlihan Lokey and Greenhill (GHL), now capture 20% of M&A fees in the U.S., four times their share in 2000.

Evercore is the only investment bank to substantially grow its advisory business in the recent rocky markets. From their 2007 peak to 2009, announced M&A transactions dropped from $4 trillion to $2 trillion. Yet in 2009, Evercore's fees soared 61%. Evercore not only punched far above its weight in M&A, but benefited enormously from the rash of bankruptcies. That's because Altman shrewdly built a restructuring arm that prospers precisely when the economy weakens and mergers retreat. Today Evercore's restructuring business is the world's third largest, ranking far short of the leader, Lazard (LAZ), but close behind No. 2 Blackstone (BX).

The rescue of CIT (CIT) was especially remarkable. Evercore restructuring specialist David Ying guided the small-business lender through a solution that had never worked before for any big financial company: a prepackaged bankruptcy. Normally insolvent banks are either taken over by the FDIC and sold off in parts, or liquidated in bankruptcy. But Ying persuaded the majority of CIT's several thousand creditors to take 70¢ on the dollar, plus equity, for their bonds, a feat most experts thought was impossible. He even forged a compromise that persuaded Carl Icahn, not known for his pliability, to vote for the deal. CIT spent just 40 days in bankruptcy, emerging sturdy in 2010. The stock has jumped, virtually restoring the creditors' stake in a company that looked doomed just a year ago.

Evercore's gains are driven by Altman's skill in poaching superstar bankers. To be sure, independent firms have been attracting talent for years. Lazard long since graduated from the boutique category because of its immense scale in M&A, restructuring, and asset management. But its basic model of providing counsel remains the template for boutiques like Evercore. Indeed, Altman was hiring marquee bankers well before the financial crisis: Among long-serving stars are Eduardo Mestre, former chief of investment banking at Citigroup, and Michael Price, arguably Wall Street's top telecom banker (not to be confused with the fund manager of the same name), who is advising CenturyLink (CTL, Fortune 500) on its $22 billion purchase of Qwest (Q, Fortune 500).

But since the start of 2008, Evercore has added nearly two dozen senior bankers, almost doubling the firm's ranks and adding expertise in real estate, energy, metals and mining, and chemicals. Last year Altman lured top transportation bankers George Ackert and Mark Friedman from Merrill Lynch, where the team generated an extraordinary $100 million a year in revenue. "We went through 18 months of turmoil at Merrill, including the merger with Bank of America (BAC, Fortune 500)," says Friedman. "We wanted to find a more stable environment." At Evercore, Ackert and Friedman immediately delivered big deals. Ackert landed his old client Burlington Northern Santa Fe, advising the railroad on its $36 billion sale to Berkshire Hathaway (BRKA, Fortune 500). Friedman is helping a number of shipping giants restructure.

Altman will spend years courting bankers who have strong ties to important CEOs and will pay top signing bonuses -- often $5 million or more, chiefly in stock -- to attract them. "Getting the best banker in an industry will generate two to three times the revenue of the second best," says Altman. Though Evercore is publicly traded, it resembles an old Wall Street partnership: The employees own more than half the shares. Altman, 64, values gray hair, an increasing rarity at financial firms; around half of his top bankers are in their fifties or sixties.

Bankers like the way Evercore lets them concentrate on dealmaking. When they were at big firms, most had to push products to a long list of clients. "Evercore is attractive to bankers who want to practice the art of the deal and don't want to be cogs in a bureaucracy," says Kenneth Griffin, chief of hedge fund Citadel, who worked with Evercore on Citadel's $2.6 billion bailout of E*Trade (ETFC) in 2007. Says Ackert: "At Merrill we were selling high-yield debt offerings, equity, and many other products. We'd work on many deals at a time, running around arranging multiple financings. It's a great luxury to concentrate on the intellectual challenge of giving advice and mapping all the possible outcomes of where that advice might lead."

CEOs are thrilled by the hands-on role of Evercore's senior bankers. "We get a higher level of service," says Maggie Wilderotter, CEO of Frontier (FTR), who engaged Michael Price to advise on the $8.6 billion acquisition of mostly rural telephone networks from Verizon last year. "At the big firms, the actual work is done by the more junior people. At a boutique like Evercore, the senior people do the actual work, from start to finish."

Clients are also comforted that Evercore offers only counsel, so the firm lacks the conflicts that plague big investment banks, which advise on deals even as they provide financing for them. "That can be a valuable service," says Bruce Van Saun, CFO of Royal Bank of Scotland, an Evercore client when he was CFO of the Bank of New York Mellon (BK, Fortune 500). "But you also must make sure that the bank is offering unvarnished advice."

That's what Evercore specializes in. Its bankers are even known to tell a client not to do a deal. Mitch Caplan, former CEO of E*Trade, recalls Jane Gladstone, who heads Evercore's financial institutions group, telling him to walk away. E*Trade's board members were flying into New York the next day to approve a multibillion-dollar acquisition of another brokerage. "We became uneasy about the transaction," recalls Caplan. "Jane said to me, 'If I'm sitting in your seat, I wouldn't do this deal.'" Caplan avoided a swamp, and Gladstone walked away from a multimillion-dollar fee. But she won it back, and more, when E*Trade chose her to lead its restructuring with Citadel.

Evercore's approach takes Altman back to his early career at Lehman Brothers in the 1970s. He is an intense intellectual -- Altman compares M&A to "mastering game theory" -- who toils relentlessly at forging and nurturing relationships. "Roger is one of the great new-business guys in the history of banking," says Tom Hill, vice chairman of Blackstone. (He also has an unusual hobby: Altman unwinds by riding show horses -- and jumping -- at equestrian events.) Raised by his librarian mother in Brookline, Mass., he learned the art of charming new acquaintances from his uncle George Frazier, a jazz critic, bon vivant, and columnist for the Boston Globe, who caroused with everyone from Errol Flynn to Frank Sinatra. "George was great fun to go drinking with at Sardi's or the El Morocco," recalls Altman. "We were very close. He knew everyone from the headwaiters to Elizabeth Taylor."

Altman spent two stints in Washington, first in the Carter administration, and then serving from 1993 to 1994 as deputy secretary of the Treasury under President Clinton. His tenure ended in an uproar when members of Congress accused Altman of leaking privileged information about a Whitewater investigation to the White House. Although Altman endured two days of grueling, televised testimony, a government ethics committee found he hadn't breached federal guidelines.

In 1995, Altman launched Evercore (the name was intended to evoke the idea of everlasting core values). Soon after, he made an unfortunate foray into private equity. One of Evercore's biggest investments was American Media, owner of the National Enquirer. The dignified Altman endured articles branding him the "Tabloid King." He reportedly fielded a distressed call from Elizabeth Edwards, wife of former Sen. John Edwards, attempting to block the story that would reveal her husband's affair and destroy his presidential ambitions. Altman declines to comment. Evercore made two investments in the company. The first was profitable; the second ended in 2009 when bondholders took control, erasing Evercore's stake.

Altman's firm may be thriving as a streamlined boutique, but he harbors grander ambitions. His goal is building a Lazard-style franchise by diversifying into profitable businesses that require little capital. Altman's main target is asset management. He recruited Ralph Schlosstein, who helped build BlackRock into the world's largest money manager. Since Schlosstein, 59, is about the same age as CEO Larry Fink, 57, he had no hopes of heading BlackRock. Last year he accepted a dual assignment: He succeeded Altman (who remains chairman) as CEO, and is assembling an asset-management franchise.

It's a smart move. Big deals tend to come in clumps. Asset management can provide steady cash flows. In less than a year, Schlosstein has quintupled Evercore's assets under management to $15 billion by acquiring medium-size fund managers. The tall, patrician Schlosstein has this to say about their division of labor: "My strength is building businesses. Roger's is doing deals. Why keep him behind a desk? He goes mad if he's not on a plane at 5 a.m. heading to Chicago or Dallas to pitch business." With CEOs ever more enamored of Evercore's approach, Altman is likely to be taking a lot of 5 a.m. flights for the foreseeable future. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates:

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

|

Bankrupt toy retailer tells bankruptcy court it is looking at possibly reviving the Toys 'R' Us and Babies 'R' Us brands. More |

Land O'Lakes CEO Beth Ford charts her career path, from her first job to becoming the first openly gay CEO at a Fortune 500 company in an interview with CNN's Boss Files. More |

Honda and General Motors are creating a new generation of fully autonomous vehicles. More |

In 1998, Ntsiki Biyela won a scholarship to study wine making. Now she's about to launch her own brand. More |

Whether you hedge inflation or look for a return that outpaces inflation, here's how to prepare. More |