Which options sins are committed most?

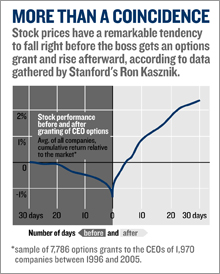

An expanded version of my post a couple weeks back about "spring-loading" and "bullet-dodging"--options practices that are less obviously illegal than backdating but still smell a little bit like insider trading--is now available in the pages of the Nov. 27 Fortune and online. One question that I didn't address in the article, mainly because I could find no clear answer to it, is exactly how widespread "spring-loading" and "bullet-dodging" really are. To quote from my article (all self-respecting bloggers must quote from their previous work): Bullet-dodging means "delaying options grants until just after the release of bad news (or moving up the release of bad news to precede an already scheduled grant)," while spring-loading means "timing an options grant to precede the announcement of good news (or delaying the happy announcement to follow an already scheduled grant)." Finance and accounting scholars began talking about this stuff way back in 1995, when NYU's David Yermack circulated a paper that showed the same pattern visible in the chart above: Stock prices tend to drop in the days before a CEO gets an options grant, and rise afterward. Yermack speculated that spring-loading and bullet-dodging were the causes. A couple years later, David Aboody of UCLA and Ron Kasznik of Stanford documented the same stock price patterns around regularly scheduled grants, which they interpreted to mean that executives who couldn't move their grants found ways to move the news instead. In 2004, though, the University of Iowa's Erik Lie suggested that some companies were setting their options grant dates after the fact, and lying about it in their financial statements and on their tax forms. A 2002 rule change brought on by the Sarbanes-Oxley Act, decreeing that options grants must be reported within two days, gave Lie additional research fodder. He found that companies that reported their grants late were far more likely to have the tell-tale v-shaped stock chart--thus convincing him that backdating explains most of the strange pattern in stock returns around options grants and that spring loading and bullet dodging "play a minor role." As Lie writes on his website: For example, if spring-loading and bullet dodging played a major role, we should observe pronounced price decreases before grants and increases after grants irrespective of whether they are filed on time, but we don't. Thus, it appears that either (a) spring loading and bullet dodging are not widespread or (b) these practices typically fail to lock in substantial gains for the option recipients. Lie says he has no idea which of these two explanations is closest to the truth. But Stanford's Kasznik has "a thought" on this, and I think I agree with him. Here's how he put it in an e-mail last week: Given that backdating is essentially an outright accounting (and tax) fraud--if not properly disclosed and accounted for--I doubt that so many companies and executives would engage in this kind of activity. The other mechanisms, i.e., spring-loading and bullet-dodging, perhaps do not have the same magnitude of impact as backdating but are "less risky" from the corporate and executive perspective. But, again, this is just a thought. Empirically, as Erik Lie also points out, it is hard to disentangle these effects for a large sample (unlike the SEC which has access to documents and other evidence not publicly available).

CNNMoney.com Comment Policy: CNNMoney.com encourages you to add a comment to this discussion. You may not post any unlawful, threatening, libelous, defamatory, obscene, pornographic or other material that would violate the law. Please note that CNNMoney.com makes reasonable efforts to review all comments prior to posting and CNNMoney.com may edit comments for clarity or to keep out questionable or off-topic material. All comments should be relevant to the post and remain respectful of other authors and commenters. By submitting your comment, you hereby give CNNMoney.com the right, but not the obligation, to post, air, edit, exhibit, telecast, cablecast, webcast, re-use, publish, reproduce, use, license, print, distribute or otherwise use your comment(s) and accompanying personal identifying information via all forms of media now known or hereafter devised, worldwide, in perpetuity. CNNMoney.com Privacy Statement.

|

|