Buffett vs. Bernanke: The inflation showdown

The billionaire investor says inflation is 'exploding,' but the Fed believes commodity price shocks should subside.

|

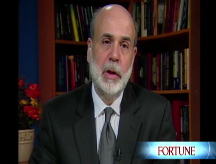

| Warren Buffett (left) and Ben Bernanke don't see eye to eye on the risks of inflation to the U.S. economy. |

NEW YORK (Fortune) -- Even Warren Buffett is wrong some of the time. Federal Reserve chairman Ben Bernanke is hoping this is one of them.

Buffett, the billionaire investor behind Berkshire Hathaway (BRKA, Fortune 500), fingered "exploding" inflation Wednesday as the biggest risk to the economy. "I think inflation is really picking up," Buffett said on CNBC. "It's huge right now, whether it's steel or oil," he continued. "We see it everywhere."

Indeed, the prices of gasoline and milk have shot past $4 a gallon, and Dow Chemical (DOW, Fortune 500) has announced twice in the past month that it's raising prices to offset soaring commodity costs.

Yet Bernanke's Fed signaled Wednesday that, after nine months of interest rate cuts and expansive lending to the financial sector, it isn't eager to reverse course and push rates higher to try to tamp down rising prices.

Why? Because the Fed remains skeptical that high commodity prices will ripple through the economy, leading to broad price hikes and big wage increases.

"The committee expects inflation to moderate later this year and next year," the Federal Open Market Committee said in holding the fed funds rate steady at 2%, though it did note that "uncertainty" remains high and suggested inflation concerns could rise.

In part, the Fed's decision turns on a distinction economists make between inflation and "relative-price changes." The former is a general loss of purchasing power that's caused, or at least exacerbated by, overly lax monetary policy (such as keeping interest rates too low for too long). The latter are price hikes driven primarily by fundamental shifts in supply and demand.

If demand for commodities is spiking because of strong worldwide growth, the thinking goes, prices should rise accordingly, until consumers react by reducing consumption - a process that isn't apt to be influenced by interest rate changes.

The Fed is betting that rising prices won't feed through to higher general inflation expectations unless workers start demanding raises and companies start raising prices.

But wages haven't been rising sharply, and declining unionization means workers have less bargaining power than they did during the inflationary 1970s, economists say. And while some processors of commodities, like Dow, are charging more, their customers in turn have generally been unable to pass along those costs to consumers.

So even as some members of the Fed's policymaking body, such as Dallas Fed President Richard Fisher, warn of the need to take quick action against inflation - Fisher dissented for the third straight meeting in Wednesday's vote, this time advocating a rate increase - committee members' inflation forecast for 2010 has risen only slightly since October, despite surging oil prices.

"Oil prices have ratcheted up over the past nine years and the dollar has depreciated for more than six years. Nevertheless, as long as a central bank is not creating an excessive amount of money, these relative price pressures ought to be transitory," Sandra Pianalto, president of the Federal Reserve Bank of Cleveland and a voting member this year of the Federal Open Market Committee, explained in a speech last month.

"As consumers spend more money for higher-priced petroleum and agricultural goods," she continued, "they eventually have less money to spend on other goods and services. Other relative prices must then fall."

To be sure, there are other factors at work in the Fed's move to the sidelines. Bernanke & Co. wants to measure the stimulative effect of the rate cuts it's already made. The rate cuts of the past nine months - the Fed has slashed its overnight bank lending rate by 3.25 percentage points since September - will take time to impact the economy. If possible, the Fed wants to wait before making another move on rates.

And while fears of a marketwide meltdown seem to have eased, a weak housing market, rising unemployment and increasing loan losses at banks mean the risk of a sharp economic pullback remains substantial.

"In an environment of dislocated funding markets, a rate cut would not produce a recovery but a rate hike could trigger a recession," writes Tullett Prebon economist Lena Komileva.

Indeed, while inflation is the buzzword right now, the surge in fuel costs is hurting growth in some key industries. Airlines such as United Airlines, a unit of UAL (UAUA, Fortune 500), and Continental (CAL, Fortune 500) have set plans to eliminate thousands of jobs in response to soaring fuel costs.

Automakers Ford (F, Fortune 500) and General Motors (GM, Fortune 500) have slashed their production schedules as well, as consumers stopped buying the fuel-guzzling sport utility vehicles that were once a huge source of profits for Detroit. The loss of high-paying pilot and autoworker jobs will only add to existing weak wage and job trends.

None of this makes the recent price shocks easier to bear, of course. But for policymakers, if not for media darlings such as Buffett, the distinction is an important one. "While sometimes devastating," Pianalto said in her speech last month in Paris, "these global relative-price pressures are not the same thing as inflation." ![]()

-

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More -

This group of companies is all about social networking to connect with their customers. More

This group of companies is all about social networking to connect with their customers. More -

The fight over the cholesterol medication is keeping a generic version from hitting the market. More

The fight over the cholesterol medication is keeping a generic version from hitting the market. More -

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More -

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More -

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More -

Once rates start to rise, things could get ugly fast for our neighbors to the north. More

Once rates start to rise, things could get ugly fast for our neighbors to the north. More