Main Street turns against Wall Street

A populist backlash is changing America's political climate. Inflamed by the financial crisis and bailouts, a form of class warfare could haunt business leaders for years to come.

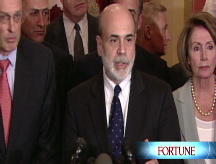

NEW YORK (Fortune) -- In one frenzied month Treasury Secretary Henry Paulson and Federal Reserve chairman Ben Bernanke remade Wall Street. Along the way they may also have recast American politics. A month of historic government interventions shows signs of triggering a political version of climate change - unleashing a new era of class fury that could hurt U.S. companies, business leaders, and wealthy investors for years.

"A potential calamity," predicts Democratic pollster Doug Schoen. "If the reactions we're seeing hold, we could have real spasmodic anger directed at businesses and corporations." And the timing will have consequences, says financier and onetime GOP presidential candidate Mitt Romney: "Unfortunately, politicians have seized on the politics of envy," he told Fortune, "and they are stoking it this election year like I've never seen in my lifetime."

Compared to this, Enron was a warm-up exercise. For all the public outrage over accounting scandals seven years ago, the result in Washington was limited to a financial reporting rule that most Americans have never heard of (though many in the business community still consider Sarbanes-Oxley a destructive overreaction).

By contrast, the implosion of Wall Street, followed by Paulson's escalating series of multibillion-dollar rescues, has fired up populist sentiments that were already building in American politics, promising to reshape legislative battles over everything from tax and trade policies to federal regulation. Union leaders like the AFL-CIO's John Sweeney suddenly sound as if they're in the mainstream of public opinion with statements like this: "One thing is certain. No one - no politician, no investment banker, no television commentator, no economist - should be able to say again with a straight face that here in the United States we just let markets do whatever markets do and everything works out for the best."

Washington hath no fury like Middle America scorned - and there's reason to think it will only get uglier. The government's massive new financial commitments will severely tie the next President's hands in addressing middle-class concerns.

"The next President will have to temper expectations a lot," says Middlebury College economist David Colander, "far beyond what either of the candidates has been willing to talk about."

If that means Republican John McCain gives up on letting the upper middle class keep the Bush tax cuts, it also means that Democrats will have to stop promising ambitious spending programs. Barack Obama rightly says it would be "irresponsible" not to review his spending menu - which includes making health care universal - in light of this new fiscal reality. As for problems like Medicare and Social Security? They'll have to wait.

***

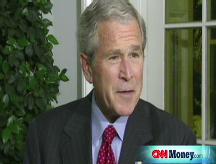

On the cool fall morning that Paulson, Bernanke, and Vice President Dick Cheney first trekked to Capitol Hill to persuade a skeptical Congress to pass an unprecedented $700 billion federal buyout of troubled bank debt, White House spokesman Tony Fratto tried valiantly to get his message out to reporters: "This is a rescue plan for the American economy," he insisted.

Despite the dire warnings of financial calamity from the White House and a few high-profile business leaders, much of Middle America wasn't buying the story that their own livelihoods were linked to the fate of the rescue package. Instead, average workers read the plan as the "big guys bailing out their friends," says former House Speaker Newt Gingrich, who commissioned a bipartisan survey on the subject. Gingrich's poll - conducted by Schoen and Republican Kellyanne Conway - found that a majority of Americans don't want Congress to use taxpayer dollars to bail out financial institutions, even if their collapse means a rocky ride for investors in the stock market.

The White House was knocked off-balance by potent blowback over the plan - not from the expected (read: liberal) quarters but from shopping-mall America. Morning talk-show hosts like Regis and Kelly shook their heads in disgust. Constituents in rural southern Illinois - a Republican district - phoned in their opposition to Congressman John Shimkus in a ratio of 200 to 1.

While Senators grilled Paulson and Bernanke on one side of the Capitol, House members on the other side were offering colorful translations of their constituent views, calling the plan "socialist" and accusing Paulson of handing over "the keys to the liquor cabinet," as Democratic Texan Lloyd Doggett put it. Within three days more than 2,000 people had logged their mostly angry opinions on CNNMoney.com.

During the unveiling of the plan, Paulson and Bernanke had exuded confidence that everyone would understand the urgency and that Congress would approve it quickly. "If it does not pass now," Paulson intoned, "then heaven help us all." They banked on public fear of a financial crash; instead, they ran into a fear from lawmakers who had to face down the folks back home angry at having to bail out Wall Street's masters of the universe.

Capitol Hill brimmed with calls for limits on pay for any executive who wanted taxpayer help. Warren Buffett, with his $5 billion bet on Goldman Sachs (GS, Fortune 500), emerged as an example of what the government could do for taxpayers if it drove a harder bargain with the banks to collect a piece of the upside. Bush's team was already facing criticism for playing the fear card, but to get his package through, the President had to take to the airwaves to make concessions and warn his nation of doubters. "We are in the midst of a serious financial crisis. Our entire economy is in danger."

-

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More -

This group of companies is all about social networking to connect with their customers. More

This group of companies is all about social networking to connect with their customers. More -

The fight over the cholesterol medication is keeping a generic version from hitting the market. More

The fight over the cholesterol medication is keeping a generic version from hitting the market. More -

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More -

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More -

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More -

Once rates start to rise, things could get ugly fast for our neighbors to the north. More

Once rates start to rise, things could get ugly fast for our neighbors to the north. More