When a takeover battle goes nuclear

What happens behind the scenes when one energy company refuses to be swallowed by a bigger rival?

|

| Mapping Strategy: NRG chief Crane meeting with his team of advisers in November during an industry conference in Phoenix, where NRG pointedly rejected Exelon's bid, deriding it as "low-ball." |

|

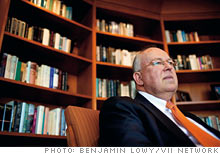

| Shopping for value: Exelon's Rowe, in his office overlooking Chicago's Loop, wants to add NRG's 44 power plants to his giant utility, which already operates America's largest fleet of nuclear facilities. |

(Fortune Magazine) -- David Crane, CEO of NRG Energy and a father of five, was standing in a stubby cornfield in Bucks County, Pa., one windy evening last October when his BlackBerry began to stir. He checked his in-box, but he didn't respond, not right away. It was Sunday night, and he was on an outing with his family, waiting in line for a Halloween hayride. Nor did he respond an hour later on his way to the Amtrak station to catch a train to Washington, D.C. How could he, when he drives a Mini Cooper with a stick shift? You need both hands to manage a car like that. So it wasn't until after nine at night, having found a quiet corner of the waiting room behind a Dunkin' Donuts kiosk, that Crane finally got around to calling back John Rowe.

Rowe, CEO of Exelon Corp. (EXC, Fortune 500), picked up Crane's call at his big-windowed aerie in Chicago's Chase Tower, 54 stories above the Loop. Rowe told Crane that his board had met that afternoon, and he had some news: Exelon, the country's biggest electric utility, was hereby offering to buy NRG (NRG, Fortune 500), the country's fastest-growing independent electricity merchant -- it sells wholesale power to utilities -- for stock in a deal worth $6.2 billion. Term sheet to follow, press release within the hour. "Offer" was a euphemism; this was a hostile act.

Crane was stunned, less by Rowe's uninvited bid (his lust for NRG was no secret) than by his choosing to publicize it instantly. Protocol dictates that a classic bear hug, as the M&A world defines the ritual, begin with a warm embrace, in private, with an eye toward achieving mutual consent. Rowe wasn't even pretending to be nice. Crane could imagine why. NRG was secretly pursuing two deals of its own with Houston-based power companies: one code-named Doris, for Dynegy (DYN), the other Rodeo, for Reliant. Either would create regulatory obstacles that could block Exelon. Somehow Rowe had gotten wind of them. Neither was imminent, Crane says now ("He had a lot more time"), but Rowe didn't know that.

Their conversation lasted only a few minutes. Crane asked Rowe if he had his debt financing in place. Both men understood that a change of control would trigger an immediate requirement to pay down $8.5 billion in NRG loans. "Not yet," said Rowe, "but we're working on it." Crane wanted nothing to do with this deal: not with Rowe, whom he barely knew; not with Exelon, which he views as stodgy, bureaucratic, and otherwise "ill suited" to run an entrepreneurial enterprise like NRG without "suffocating" it; and definitely not at that price, which he would soon be describing to anyone who would listen as tantamount to "stealing the company." Nevertheless, he tried to be civil as he concluded the call, promising Rowe, "We'll give this serious consideration."

So much for his scheduled trip to Washington. Crane called Jonathan Baliff, NRG's M&A specialist, and reached him at home. "You're not gonna believe this," he said, still not quite believing it himself. "John Rowe just called to wish me a happy Halloween."

Hostile takeovers, you see, are almost unheard of in the electric power industry. It's a hidebound realm, tightly regulated, defined by collegiality, cooperation, and respect for the other guy's territory. Moreover, dealmaking has its seasons, and right now we're in a drought. M&A activity in the U.S. is off 45% by dollar value in the first half of 2009, compared with the first half of last year, according to Dealogic. Not since the dotcom bust at the turn of the century has the field been so fallow.

This battle, then, is the one to watch, with all the elements of a classic fight: warring visions of the future, corner-office egos, a seesaw battle, and billions at stake. During the eight months that have passed since the first shot was fired, Fortune has gone behind the scenes to chronicle this case of modern corporate warfare -- eight months of fiery press releases and dueling investor presentations, with millions of dollars diverted to lawyers, investment bankers, and strategy advisers, and perhaps billions lost to missed business opportunities. There's been a tender offer on the table since November, extended three times, and come July 21 there will be a proxy vote at NRG's annual meeting on four proposals designed by Exelon to stack the board and, Rowe hopes, end the stalemate and deliver NRG to Exelon. Betting on a speedy resolution, however, would not be wise.

The battle lines were drawn early, and they haven't budged. It's a standoff between an aggressive buyer with a value investor's mentality, Exelon, looking to pick up a prize collection of assets at a bargain price, and a deeply reluctant seller with a persuasive growth story to tell, NRG, determined not to sell its future short.

How you handicap the outcome depends on how you view the broader prospects for the economy. V-shaped cycle, you think? Advantage NRG, which as a wholesale power merchant with ambitious growth plans would benefit disproportionately from a sharp, sustainable recovery; Exelon would have to boost its bid or walk away. U- or L-shaped? Advantage to the bigger, better capitalized Exelon, whose willingness to pay up for a growth company in hard times may look better and better to NRG's battered shareholders the longer the downturn lingers.

To describe this as a fight between two power companies, however, would vastly fail to do justice to the matchup between the principals: Crane, the new-breed power merchant, alert to every exploitable angle in the wide-open era of deregulation, and Rowe, the old-style utility exec, whose mantra is "We just deal in what keeps the lights on at a price consumers will pay." Opposites in every way, each a perfect embodiment of the forces he represents.

Crane, 50, is a lean, fidgety, fast-talking product of Princeton, Harvard Law, and Lehman Brothers. When he was recruited six years ago from International Power in London to lead NRG out of bankruptcy, it was more for his finance chops than his knowledge of alternating current. He's good with debt, good with hedges, good with deals -- "things that we respect and admire and can learn from," Rowe admits (although Rowe has already told Crane there will be no place for him at Exelon if the deal goes through). And he's out front on climate change. NRG may be one of the dirtiest power companies in America, measured by CO2 emissions, but Crane has big ambitions to do good and prosper in the coming carbon-constrained world by deploying revolutionary clean-coal technologies, investing in solar and wind, and building the first new nuclear power plant in America in more than a generation.

Rowe, 64, is jowly, bespectacled, and bald. He wears nice suits and keeps his jacket on. He doesn't talk; he orates, in complete sentences. His farmer dad had hoped he'd come home to tiny Dodgeville, Wis., after college and law school in Madison, but Rowe had other plans. He loves power plants the way some people love trains, although coolly and without illusions. "They're not new ideas that multiply," he says. "They're big, complicated assets that take space, that sometimes annoy their neighbors, and that have to be run with great precision." Rowe formed Exelon in 2000 by merging Philadelphia's PECO Energy and Chicago's ComEd. Today he presides over a power industry colossus with $19 billion in annual revenues, 5.4 million electricity customers, and the nation's largest fleet of nuclear power plants.

Significantly, all those nuke plants were built by CEOs more willing than Rowe to make risky, long-term strategic bets. "There are always places where the great visionary wins," Rowe says, alluding to Crane and his schemes, and implying that this is not that place. "This is fundamentally a value industry, and neither our investors nor NRG investors will wait a long time to see a return. They don't see this as a place where somebody's inventing the next chip, or the next drug, or the next airplane, or something exotic. This is a business where it's all about how much can you make out of assets."

Rowe covets NRG's assets: NRG's 44 power plants, especially its 44% stake in South Texas Project (STP) 1 and 2, two giant nuclear reactors on the coastal plain 90 miles southwest of Houston that together provide power to two million homes. Add the fact that the two companies' territories don't overlap much, which lowers the regulatory threshold, and you understand why it has long been obvious to people in the industry that NRG would tuck neatly into Exelon's empire.

Obvious to Crane, too, and after all, who was he to snub a wealthy suitor like Exelon? Crane is widely credited with having turned NRG into a "free-cash-flow machine," as the analysts say. The stock was up 300% from late 2003 through last summer. That said, Crane reports to a board of directors that was put in place by shell-shocked bondholders as NRG emerged from bankruptcy. His job is to realize the value he has repaired, not sit on it. If Exelon wants to talk, Crane must listen; he understands that.

Before the Halloween call, a foreshadowing of the conflict surfaced Sept. 24, 2008, after Rowe dispatched two J.P. Morgan bankers to Bobby Van's restaurant on Park Avenue in Manhattan for an exploratory lunch with Baliff from NRG. Lehman Brothers by this point was bankrupt. Commercial banks across the country had quit making loans, stocks markets the world over were collapsing -- a hard winter was setting in fast. Exelon was not immune. Its stock was down 25% from its midsummer peak, which would suggest that maybe this was not the moment to proffer a stock deal. Except that NRG's stock was down even more, almost 40%.

Baliff walked into the restaurant that day without a detailed agenda. He was new at NRG, recently recruited from Credit Suisse (CS). The bankers were old acquaintances of his. This was about building a relationship, maybe opening some doors at J.P. Morgan (JPM, Fortune 500). But just as Baliff was launching into a primer on NRG's happy prospects as a standalone company, the J.P. Morgan guys cut him off. John Rowe sent us, they said. He wants to talk to David Crane. Baliff and the bankers finished their steaks. They caught up on each other's kids. And the last thing Baliff said was, Don't have John call unless the price is right. "It better have a four handle," is how he put it.

Rowe called two days later, not yet in hostile mode, and told Crane, "We've looked at the numbers and we think we can offer you over $40 a share." In that case, said Crane, "Let's meet." They made a date for Tuesday, Sept. 30, four days later, at J.P. Morgan's offices in New York.

Four days, alas, during which the world as we know it nearly came to an end, with markets crashing and governments rushing into full bailout mode. Yet everyone showed up to talk about a deal: David Crane and two EVPs, Denise Wilson and Bob Flexon, for NRG; Rowe and Chris Crane (no relation) for Exelon. The bankers held the door, then retreated. This was principals only.

Rowe got right to the point. He bemoaned the state of the world. His stock, over $90 in July, had closed at $61 on Monday, down 9% in one day. Too shaky just now to use as acquisition currency. Therefore no offer would be forthcoming. "But why don't we start a due diligence process?" Chris Crane suggested. Sign a confidentiality agreement, exchange financial information, keep the dialogue going.

NRG's Flexon and Crane looked at each other as if to say, We came all the way to New York City to listen to this? "No," said Crane. "No. We're not prepared to start a due diligence process as an intellectual exercise. When you have something to offer, come back."

After that, for nearly three weeks Rowe was silent. Until he called to wish Crane a happy Halloween.

"Oh, crap, my spots are taken!" Crane is just back from lunch at Conte's, his favorite Princeton pizza joint. It's a cold, wet day in late October. A white substance more like rain than snow is falling heavily on this suburban office park, pelting the windshield of Crane's car. It's been a week since Crane learned that Exelon has NRG lined up in its sights, and clearly he doesn't like the idea now any more than he did then. "I don't know whether it's two years out or three years out, but there's going to be a time when NRG stock is going to go on fire," he's been saying. However, that's only if Exelon goes away. "I always say development is more an art than a science," he's chattering away, and "I don't think they have the ability in their big platform to capitalize on the opportunities I think we have," and "You need people who don't perform well in a bureaucracy-laden, committee-suffocated utility," when, as if on cue, he rolls his little blue Mini up to the front door of NRG headquarters and finds there's no place to park. Metaphor alert: NRG is a different kind of company. Cubicles for all, even the CEO. No reserved spaces. "I'm going to have to park across the street," he says apologetically.

All week Crane and his team have been plotting how best to retaliate. The bid is too low -- no disagreement there. It's a fixed-exchange offer, 0.485 shares of Exelon for each share of NRG. On the day it's delivered, that works out to a 37% premium for NRG shareholders, or more than twice the industry norm for an all-stock deal. Normally, to quote Rowe, "that's not just an attractive offer, it's a clean kill." Obviously, Crane disagrees. He's willing to sell, he says, even to Exelon, but not for what equates in his mind with "highway robbery," with "stealing the company at a fraction of replacement cost," and what's more, "just taking our growth -- our imbedded growth -- for free." The board agrees and quickly gives its unanimous approval to back Crane and reject the bid.

Now Crane and his team go to work on a three-pillar strategy to defend the company. One, be patient. A consensus soon develops around holding off on a response till the annual investor conference of the Edison Electric Institute (EEI), the utilities' trade association, two weeks away in Phoenix. Everybody with a stake in the outcome will be there. And if NRG were to publicly reject the offer on the eve of the conference? "I would be disingenuous if I didn't tell you there was a little payback in that," Crane admits.

Two, develop other options: white knights that might outbid Exelon, including several large American and European utilities; and white squires that might want to bid on a piece of NRG and so raise the value of the whole. Among the latter: Japanese and European companies interested in partnering with NRG in Nuclear Innovation North America (NINA), a jointly owned development company (with Toshiba) that's moving ahead with plans to build two new nuclear-power plants in Texas, STP 3 and 4.

And three, articulate a fallback position, a "standalone plan," in Baliff's words, "that works and that is well communicated to the Street," emphasizing NRG's growth prospects and ample cash.

Crane knows he's playing not only for his own survival but also for the working lives of NRG's entire headquarters staff, some 400 souls. Usually, even in a hostile takeover situation, the aggressor will at least nod, however cynically, toward the so-called social issues. Not this time. "They're talking about us on a complete wipeout situation," says Crane. "They're not talking about this in terms of 'merger of equals' type language -- 'Let's get the two companies together, the best people will run it.' They're like, 'No, you guys are all dead. We just want your assets.'"

In fact, Exelon has made a couple of awkward stabs at addressing some of the social issues. One of them appears to have been a quiet attempt to enrich Crane and a handful of top managers at the expense of headquarters staff and NRG shareholders. It was allegedly conveyed by Paul Dabbar, managing director for global mergers and acquisitions at J.P. Morgan, in a late-night phone conversation with Baliff the day after Crane and Rowe met face to face in New York. Dabbar "basically said, 'Look, we know that you guys have value expectations in the mid-40s area,'" Baliff told Fortune, "'and we know that certain senior management are very incentivized at that level. I've been authorized to tell you that there are other structures by which senior management at NRG could receive compensation.'" ("I may or may not have talked to him the day after the meeting," says Dabbar. "I don't remember. But I do remember very specifically that we did not discuss things in any conversation -- either in person or on the phone -- the way it was described.")

If an offer as described by Baliff were made, "There are several things wrong with that," says Duke law professor James Cox. If the NRG execs take the money, that's what is "pejoratively referred to as a secret profit. They can't make any secret profits unless, one, they disclose it, and two, it's approved by the stockholders." If they got caught, says Cox, they'd have to "disgorge their ill-gotten gains." Exelon, meanwhile, could run afoul of the one-price rule. "If they make the offer at $25," says Cox, "and they're making at the same time this side payment, there is a precedent out there that says that the $40 has to be paid to everybody." To Baliff, the episode confirmed the prevailing view of Exelon by executives at NRG: "They're indelicate and they're heavy-handed." Baliff immediately relayed the conversation to his boss. Crane told Baliff to ignore it, informed his board, and moved on.

NRG's harshly worded formal rejection, when it finally arrives on Nov. 9, lands like a bombshell at the Phoenix conference. That night, at a private dining room in a Ruth's Chris Steak House (what is it with dealmaking and steaks?) where Crane is entertaining a group of NRG shareholders, the question that comes up again and again is, Why the belligerent tone? Was it really necessary to condemn Exelon as "opportunistic" for offering a "low-ball exchange ratio"? Did you have to say that you saw "no evidence of even a single senior executive at Exelon with any experience whatsoever" managing a company like NRG? Couldn't you have just politely refused and maybe left the door open a crack for a possible better offer?

Crane knows he's walking a tight line. He wrote a letter like this once before when faced with a far less threatening takeover attempt by Mirant (MIR), another merchant power company, and the impact was devastating. Mirant quickly withdrew. "They were left like a dead body in the road," one of NRG's bankers recalls admiringly, "like carrion." Does Crane really want that now? Well, he says, he's realistic. He knows that $40-plus is no longer a reasonable goal; he says he'd take something in the 30s. "But at $26.50, they're so far below our range that there's no way they can get it into a range where we would consider it, because then it would just look like he was chasing his own tail," says Crane. "Then he would just be totally crucified by his own shareholders."

Next day at the electric conference, the battle between NRG and Exelon is all anyone wants to talk about. "It's the personal dynamic here that is interesting," says a banker who doesn't want to be quoted by name. "John, he's been trying to get a big deal done for several years now and hasn't been successful, and this is a very public situation. I think one shouldn't underestimate the extent to which he will pursue this vigorously."

There's a brightly painted 2,600-year-old Egyptian sarcophagus in John Rowe's Chicago office. "I threaten to put vice presidents in there," Rowe jokes, while his press aide squirms. His wedding ring is an antique coin from the Turkish city of Tarsus in the time of Alexander the Great, adorned with an image of Athena. ("My wife permits me to have another woman's face on my wedding ring only because she did not exist.") His cuff links are also Greek coins. ("That's Athena too. Goddess of weaving and all these practical things.") "I love any kind of history," Rowe says, tenting his fingers, leaning back in his chair. "I think people haven't changed all that much over the past 3,000 years. We're all trying to cope with a lot of things that are beyond our control. Most of us are trying to make the best we can out of them. It never gets simple."

This business with NRG, for example. On the day Exelon announced its bid, S&P downgraded Exelon's credit rating to BBB, one notch above junk, to reflect the impact that absorbing a highly leveraged merchant power company would have on an otherwise excellent balance sheet. That's complicated; no utility wants to lose its investment-grade rating. Also, it's the middle of December already, and Exelon still hasn't been able to line up the financing it needs to turn over NRG's debt. In the midst of a global credit crunch, that's really complicated. But Rowe is undeterred. He says he was "the nerd" the year Dodgeville High was runner-up state champion in basketball: "My twisted personality was formed by being the only boy in school who could not put a round ball through a hoop." And he claims he's no Gordon Gekko: "I've never been a corporate raider before. It's kind of like a basset hound trying to make like a Doberman." But neither did he slink away when he received Crane's scathing Dear John letter at the EEI conference. Instead he countered with a tender offer that sidesteps NRG's board and management and appeals directly to the shareholders. And no, he did not raise his price. "My investors are very firm when they talk to me," Rowe says. "They want to make certain that I don't have too much ego in this. I look at them in a very reptilian fashion and say, 'Look, I've been about value for 25 years. I've built the most valuable company in this industry. You think I'm going to throw it away in one last round? I simply am not.'"

Again and again, Rowe comes back to his fundamental position on value -- both the value he wants to protect in Exelon and the value he recognizes in NRG. That company's value, he insists, has everything to do with its existing capacity and nothing to do with its ambitious plans for growth. He refuses to assign any value whatsoever to the nuclear plants NRG wants to build next, STP 3 and 4, even if they are among the first in line for billions of dollars in government loan guarantees. Any value there, he says, is so remote -- so contingent on political, economic, and environmental variables -- as to be meaningless.

Three months later, over dinner at the Chicago Club -- oysters, steak (more steak!), and a couple of tumblers of 25-year-old Macallan single malt -- Rowe will tell a story that hints at the depth of his discipline when it comes to defining value in the power industry. "In our business," he'll say, "I have seen CEO after CEO torture themselves with mistakes on power plants. Because you don't go into our business unless you like power plants and transmission lines. If what turns you on is cosmetics, you don't become a utility executive." He'll pause for emphasis, and then he'll go on. "The six plants that are making most of our money now were all built by a man named Tom Ayers [longtime CEO of Commonwealth Edison]. I went to his wake. I'm sitting there thinking, 'I've made a ton of money because of the plants you built, and I ought to be really grateful for your courage -- but you had Alzheimer's before they made any money!' I respect that immensely. But you can't afford to make decisions that don't pay until 20 years after you retire."

"So," says David Crane, kicking things off, "they've got 51%." Seven grim faces surround an NRG conference table in Princeton. It's 8 a.m. on Feb. 26. They've all just learned that 51% of NRG's shareholders have accepted Exelon's tender offer, up from 46% at the first deadline in January. It's not game over. The offer is highly conditional, and the conditions haven't been met. Still, not a happy day at headquarters. "I think people are a little tired," Crane concedes privately. "I don't know if they believe 50% is an important number from a practical point of view -- it's not -- but from a psychological point of view ..." His voice trails off. "Look, we would have loved to have won this round. You don't like to lose a round."

Later, on the way to Conte's, the pizza restaurant, Crane says he knows perfectly well what's going on here. The world was a scary place when Exelon made its offer. It's even scarier now, in February, weeks before Fed chief Ben Bernanke has uttered the phrase "green shoots." During the run-up to the second tender deadline, Crane was flying around the country, meeting with institutional investors, pleading his case and not getting anywhere. "The day I was in Boston," Crane says, "you get in with these fund managers, they come into the meeting and they've got like the thousand-yard stare. They've been looking at the computer screen all week, and they've just been seeing a sea of red. It's just very hard to talk to them about, you know, medium- to long-term value creation."

Tough times favor Exelon -- that's the reality. Crane still has tactical options, but at this point his most effective may be the simplest: stalling. He'll drag things out as long as he can and hope for signs of a turnaround in the economy -- anything that might begin to persuade enough shareholders to disassociate the G-word, growth, from the R-word, risk, and restore a little faith in NRG's future.

Already Crane is looking ahead to the next battleground, NRG's annual meeting, where one-third of NRG's board is up for reelection. Exelon has announced it will run its own slate to replace the four directors whose terms are up. Also, Rowe's advisers have come up with a complicated scheme to expand the board -- enough to secure influence ("to the point of paralysis," says Crane) if not actual control. NRG responds by delaying the annual meeting, originally scheduled for May, until midsummer. Crane knows that even if Exelon succeeds, it will still have "huge wood to chop to get this transaction done." Nevertheless, an orchestrated coup at his annual meeting? That's a gloomy prospect. "I guess this is what they say is sort of a classic bear-hug situation," says Crane, "a gradual, rolling dispiriting of the opposition. The whole idea of a bear hug is that it becomes an inevitable, self-fulfilling prophecy. And, uh, it's succeeding pretty well on that path."

"We continue to have our way on NRG," Rowe tells Fortune at the Chicago Club on March 19. Among the holdouts, he sees two types: those few who oppose the deal, period, and those who -- like David Crane, he believes -- just want more money. But Rowe is adamant: He will not raise his offer, even a little. "There isn't a one of us who doesn't hope we're going to be back to the amount of money we thought we had nine months ago," he says. "That includes my secretary with her 401(k) and me with my Exelon shares and options. And in David's case, the effect has been much more dramatic. I truly think David is motivated by an unrealistic view of when financial valuations are going to return. It's going to come much more slowly and much more painfully than any one of us would like."

Or maybe not. Ten days earlier, on March 9, the Dow closed at 6547, its lowest point since April 1997. Since then, it's up 850 points. A trend? It was still too early to tell. But over the next three months, it keeps climbing. Fund managers are less frightened, investors are making money again, and even though Warren Buffett still thinks the economy is in a "shambles," Wall Street, Main Street, wherever you go, the cloud seems to be lifting a bit. That's a boost to NRG. It's exactly what Crane was hoping for with his stalling strategy, and it seems to be working.

In fact, a lot seems to be working for NRG lately. Credit markets are thawing, allowing NRG to borrow $700 million on favorable terms. The version of the Waxman-Markey climate-change bill that passes the House includes a compromise solution to capping carbon emissions that is far less punishing to NRG than most analysts had feared. NRG buys Reliant's retail business for $290 million cash, a move the Street vigorously applauds. And in mid-June, the Energy Department picks NRG (and not Exelon) as one of four recipients of $18.5 billion in federal loan guarantees allocated for new nuclear plants. All of which seems to confirm the growth story Crane has been telling all along and sends investors rushing to buy NRG stock. It's up nearly 50% since the market bottom in early March, compared with 15% for Exelon. That wipes out the premium implied by Exelon's offer, leading NRG shareholders to abandon the proposed deal in droves. As of June 16, Exelon announces, tendered shares in hand total only 12%, a dramatic retreat from last winter's majority.

That leaves Rowe with two options, both of which he is loath to do: walk away or raise his bid. On June 30 he goes before his board and, after a four-hour discussion, receives unanimous approval to sweeten the exchange ratio to 0.545, a 12.4% increase.

The formal announcement comes two days later, right before the Fourth of July weekend. "We're making a bump here that is intended to close the deal," Exelon's legal chief Bill Von Hoene tells Fortune. "This is not at all an iterative process at this point." Crane, who gets the news from the SEC filing (Exelon doesn't bother to call or write this time), is noncommittal. "The board has to decide," he says for the record. "It's above my pay scale. They'll do so promptly." Whatever the board's decision, the war will go on. At least to the July annual meeting, and maybe beyond. That means more pizza, more steaks, and more drama. ![]()

-

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More -

This group of companies is all about social networking to connect with their customers. More

This group of companies is all about social networking to connect with their customers. More -

The fight over the cholesterol medication is keeping a generic version from hitting the market. More

The fight over the cholesterol medication is keeping a generic version from hitting the market. More -

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More -

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More -

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More -

Once rates start to rise, things could get ugly fast for our neighbors to the north. More

Once rates start to rise, things could get ugly fast for our neighbors to the north. More