AIG's rescue has a long way to go

When will the government's costly bailout of the deeply distressed insurance giant be over? Don't expect it to be anytime soon.

|

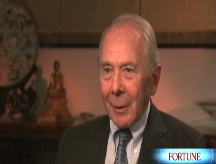

| Autos and homes were Liddy's insurance beat at Allstate. The vastly more complex world of AIG has left him dealing with problems of enormous depth. |

NEW YORK (Fortune) -- Within insurance giant American International Group, but known to only a few people, is something irreverently called the "kill list."

It was created by AIG's controller, David Herzog, on Tuesday, Sept. 16, the wild day when the company plunged toward bankruptcy only to be bailed out instead by the U.S. government. Very late that night, Herzog, then 48, sat in the company's New York City headquarters, brooding about the day's events.

Robert Willumstad, CEO for only three months, had learned from the Federal Reserve that he was out, on the theory no doubt that the government can't extend an $85 billion credit line to a company and leave things in the hands of existing management.

The AIG board had been told that the new CEO was to be Edward Liddy, who had decades before overseen a Sears Roebuck restructuring and then become head of a Sears spin-off, Allstate Insurance. More important to the crisis at hand, Liddy's career had made him a business friend of Secretary of the Treasury Henry Paulson and a member of the Goldman Sachs board.

Minutes before midnight, at 11:54 p.m., Herzog - called by one former AIG officer "a prince, a straight shooter" - wrote a short e-mail to the deposed Willumstad, first thanking him for having stepped up months earlier to the "difficult challenge" of running the company.

Then Herzog flung his e-mail grenade: "Before you leave, I ask only one thing. Please clean the slate for Mr. Liddy. I urge the following dismissals immediately." Herzog next listed the names of one vice chairman, two executive vice presidents, five senior vice presidents, and one vice president. AIG's general counsel was in the pack, and so were the heads of finance, investments, strategic planning, risk, credit, and human resources.

These executives, according to Herzog, "have shown ... a clear pattern of ineptness that contributed to the destruction of one of America's greatest companies. Please, don't make Mr. Liddy figure this out on his own." Herzog thought AIG's 120,000 employees deserved better than that and also "some sense of accountability" for what had happened. "We need leadership," he said, "and these individuals are simply not leaders."

In the one day before Liddy took over, the authority-shorn Willumstad did not fire any of Herzog's designees. In Liddy's regime, two have left. One was Richard Scott, a senior vice president, and the other - the highest-ranking executive on the list - was vice chairman and chief financial officer Steven Bensinger, to whose CFO job Liddy promoted Herzog. The remaining seven executives on his list still work for AIG, as five of them did in fact for longtime chairman Maurice "Hank" Greenberg (who was forced out by the board in early 2005) and his successor, Martin Sullivan (ousted last June).

Asked in mid-December about the midnight blast of David Herzog, new CEO Liddy says it was "one of many information points" he had looked at on his way to making his own decisions about people. Herzog himself recants. "At midnight," he tells Fortune, "after watching a great company crumble, and along with it nine years of my life's work, I sent an emotional and rash e-mail that I deeply regret. It was a product of frustration and fatigue. I disavow it completely, and I have apologized to my colleagues."

That e-mail was given to Fortune by someone who knows AIG well and thought that any article about its present and future should take note of management's long-running contribution to its extraordinary problems.

Deciding to publish the e-mail, we sought reactions from the nine people Herzog named. One person, Brian Schreiber, head of strategic planning, accepted our invitation to comment. He says angrily that after learning of the e-mail, he asked Herzog to give an example of anything Schreiber had done that had harmed AIG. "He thought a long time and he could not think of a single example," Schreiber says. "He then emphasized that he views me as important to the success of AIG's restructuring effort."

At the least, the e-mail episode is a vivid illustration of the extreme stress racking the company. Vastly global, spread out indeed over 130 countries, AIG is today a sorely wounded gladiator, with a market value that has crashed from $180 billion in 2007 to $5 billion. Competitors sensing a kill are attacking the company however they can, trying to poach its best people and customers.

These aren't just AIG's problems, they're ours. September's $85 billion from the government - Plan A, let's call it - proved to be too little, and the terms of the deal were more than AIG could handle.

So in November the feds moved to Plan B , whose complex parts add up to a mind-bending bailout of about $150 billion (which, to supply some perspective, is more than the assets of Procter & Gamble). This deal includes a $60 billion credit line from the Federal Reserve; $40 billion of preferred stock that makes the Treasury a 79.9% owner of AIG; and two Fed-sponsored financing vehicles that magically rid AIG's financial statements of about $50 billion of trouble. The aim of the package, as management sees it anyway, is to keep AIG afloat while it works toward reemerging as a standalone private company and getting Washington out of its life.

The theoretical cost here - $150 billion - may be reduced by amounts the government derives from owning AIG. Most of all the feds are set to be the beneficiary of a big plan, mapped out originally by Willumstad and unfolded by Liddy, for AIG to sell major assets. These are to include the bulk of both AIG's noninsurance properties and life insurance companies, for a total of perhaps 20 to 25 different sales. Completion of the plan, says CEO Liddy, would reduce AIG's annual revenues from around $100 billion to perhaps $40 billion and return the company to its roots, property-and-casualty insurance. Some estimates say the proposed sales could bring in $60 billion, an amount equal to the loan portion of the bailout.

Both AIG and the government are burning to make these sales. But unfortunately, prospective buyers for AIG's properties - which Liddy calls "our incredibly world-class assets" - are scarce right now. Many insurance companies that might normally bid have been crippled by investment losses, and acquirers in general can't rustle up financing. Were it forced to unload quickly, says Liddy, AIG would be looking at fire-sale prices that would benefit no one on the selling side. So AIG needs breathing room, and Plan B accommodated, extending the term of the government's main credit line to AIG from two years to five. Two side parts of the deal even have a term of six years and are "subject to extension."

-

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More -

This group of companies is all about social networking to connect with their customers. More

This group of companies is all about social networking to connect with their customers. More -

The fight over the cholesterol medication is keeping a generic version from hitting the market. More

The fight over the cholesterol medication is keeping a generic version from hitting the market. More -

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More -

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More -

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More -

Once rates start to rise, things could get ugly fast for our neighbors to the north. More

Once rates start to rise, things could get ugly fast for our neighbors to the north. More