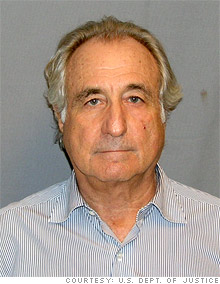

How Bernie did it

Madoff is behind bars and isn't talking. But a Fortune investigation uncovers secrets of his massive swindle.

NEW YORK (Fortune) -- The employees were transfixed. Standing on the mid-Manhattan trading floor of Bernard L. Madoff Investment Securities in late 2007, a half-dozen staffers stared up at the ceiling-mounted TV as CNBC aired a report on the mysterious Palm Beach death of a hedge fund manager who had been leading a double life. The police, it appeared, were even considering the possibility that he had been murdered. "Bernie," someone casually asked as Madoff happened to walk by, "have you heard of this guy?"

Madoff glanced at the screen, blanched, and exploded: "Why the fuck would I be interested in some shit like that?" The employees recoiled. "I never saw him react like that before," says a Madoff trader who witnessed the outburst. "It obviously hit a nerve."

Such a loss of control was highly out of character for the boss. But the traders didn't know at the time that Madoff had an extraordinarily elaborate second life going on just two floors below them, one that was building toward an epic, and inevitable, explosion. It took a special pass to get into the "back office" on 17, where Madoff was conducting his $65 billion Ponzi scheme. And even if a person could get in, there wasn't much to see: an antiquated IBM computer server kept in a locked room, piles of trading statements, and a staff of about 20 paper pushers and clerks.

In retrospect, of course, there were clues, as a Fortune investigation has discovered. The IBM server, for instance, an AS/400 that dated from the 1980s, was so old that some data had to be keyed in by hand, yet Madoff refused to replace it. The machine -- which has been autopsied by the government -- was the nerve center of the fraud. The thousands of pages of statements printed out from it showed trades that were never made.

Then there was the man who ran the floor, Frank DiPascali, Madoff's chief deputy on 17. He was a 33-year veteran of the firm, with a rough Queens accent and a high-school education, but nobody was quite sure what he did or what his title was. "He was like a ninja," says a former trader in the legitimate operation upstairs. "Everyone knew he was a big deal, but he was like a shadow."

There were other mysteries, as we shall see. But even after it detonated five months ago in a fireworks display of betrayal and recrimination, Madoff's scheme -- possibly the biggest investment fraud in the nation's history -- has remained among the hardest to penetrate. Most commonly, white-collar cases begin with a quiet, behind-the-scenes investigation, followed by a series of deals with junior employees, who are squeezed by prosecutors to cough up details about their superiors. Step by step, the prosecutors move up. Finally comes the denouement: the ringmaster hauled into court in handcuffs.

But with Madoff every aspect of that traditional narrative has been inverted. The case began with his flabbergasting confession, which set off the investigation. Madoff claimed he committed his crimes all by himself, but because they spanned decades and continents, a fog of suspicion immediately engulfed Madoff family members who worked at the firm, as well as employees and business associates.

Now that fog may be about to lift. Fortune has learned that Frank DiPascali is trying to negotiate a plea deal with federal prosecutors in which, in exchange for a reduced sentence, he would divulge his encyclopedic knowledge of Madoff's scheme. And unlike his boss, DiPascali is willing to name names.

According to a person familiar with the matter, DiPascali has no evidence that other Madoff family members were participants in the fraud. However, he is prepared to testify that he manipulated phony returns on behalf of some key Madoff investors, including Frank Avellino, who used to run a so-called feeder fund, Jeffry Picower, whose foundation had to close as a result of Madoff-related losses, and others. If, for example, one of these special customers had large gains on other investments, he would tell DiPascali, who would fabricate a loss to reduce the tax bill. If true, that would mean these investors knew their returns were fishy. (Lawyers for Avellino and Picower declined to comment. Marc Mukasey, DiPascali's attorney, says, "We expect and encourage a thorough investigation.")

The emergence of this potential star witness may well stand assumptions about the case on their heads: Some people widely assumed by the public to have been involved in the fraud may not have been, and a small group of Madoff investors who appeared to be innocent victims may not have been entirely innocent after all. But then, few things about the life of Bernie Madoff turn out to be as they seem.

Before it all went to pieces, Bernard L. Madoff Investment Securities appeared to be a charmed firm run by a tight clan. People believed in Bernie. Nasdaq made him its chairman; the SEC appointed him to industry panels; Congress invited him to testify. New York Senator Charles Schumer stopped by the office in the run-up to the Iraq war and gave a rousing talk on the trading floor. Everywhere you looked, there were signs that Madoff -- and by extension his firm -- had special status. Bernie was even able to arrange with his friends the Wilpons, owners of the New York Mets, for staffers to play charity softball games on the field at Shea Stadium.

If Bernie was the center of the firm's solar system, the nearest planet was his brother Peter, the head of compliance and de facto chief operating officer for the Madoffs' original, legitimate trading business. They were a savvy pair with a long-established dynamic. "They were the ultimate good cop/bad cop duo," says Christopher Keith, a former chief technology officer of the New York Stock Exchange who worked for the Madoffs on a side project (and who acknowledges that he clashed with them). Peter was the hands-on brother, the one immersed in detail, and most of all, the designated tough guy. "Peter was like five miles of bad road," Keith says.

Bernie's role was to glide in at the end and make peace, says Keith, who compares him to the biblical Solomon: "He was the type of person who was sort of above the fray -- the wise man."

Peter, now 63, was tethered to his BlackBerry. A lawyer by training, he was the driving force behind the firm's technology innovations. Though he couldn't write code, he could discuss software algorithms with surprising facility.

Bernie didn't have a BlackBerry. He didn't even use e-mail -- he could barely turn his computer on. His PC was configured essentially just to give him financial news, says Nader Ibrahim, who used to work on the technology help desk at Madoff's firm. "It was set up in a manner that the computer never shut off," Ibrahim explains. "So the format on the screens, how his windows were set up, and everything like that would just come up the same way. If he were to touch the stock menu and something [unexpected] came up in front of his system, he would get all flustered and call us."

Bernie and Peter were the first generation of the dynasty. The second was dominated by another set of brothers, Bernie's sons, Mark and Andy, now 45 and 43. Andy was the more cerebral one, with a better understanding of complex technological issues. But many viewed him as haughty and unapproachable, though those who know him say a kind person is concealed behind the reserved exterior. Andy survived a bout of lymphoma a few years ago (he is now in remission), and when he returned to the office, he ceased working on the firm's original trading operation and focused on other projects, such as the Madoffs' foray into energy trading, a business neither the company nor Bernie was involved in.

Mark was in charge of the main trading business at the time the firm collapsed. If he didn't have his younger brother's intellect, he had the people skills that marked him as heir to the Madoff throne. A frat boy, he was easygoing and low-key, occasionally driving his Vespa to work from his SoHo apartment. In his younger days, he would accompany his fellow traders to the topless bar Scores.

There was no question that the Madoffs were the firm's royal family. Mark and Andy worked among their colleagues on the trading floor, but they sat on a raised platform, a few feet above everybody else. And even star employees knew that they could rise only so high.

Still, for the most part people loved working for the Madoffs -- a surprising number stayed for decades. Bernie's wife, Ruth, was effervescent and gracious. She wrote lovely personal notes to employees. Bernie himself could be charming, even compassionate. In 2002 a rookie trader was seriously injured when he got hit by a car while training for the New York City marathon. "I passed out and woke up in the emergency room," the trader remembers. When he came to, he says, "I looked to one side of my bed, and my mom and dad were there. On the other side was Bernie."

But Bernie was moody, and he could make people uncomfortable. At times he would stare wordlessly into space. One former trader remembers being at a holiday party when he noticed that Madoff was glaring at him from across the room. And glaring. And glaring. "You in trouble?" the trader's fiancée whispered to him when she noticed the boss's icy gaze. Uncomfortable, the couple left early; they never got an explanation.

And Madoff could be less than sensitive. One day a female trader remarked to a colleague that she'd had a nightmare about being raped, not realizing that the boss was listening behind her. Bernie piped in: "That's not a nightmare, that's a fantasy."

Bernie had his quirks, and to a startling extent they colored the firm -- quite literally when it came to the décor. Virtually every piece of furniture, equipment, or decoration was black or gray. That extended even to the pushpins in employees' cubicles. "Bernie had the manufacturer just send boxes of black ones," says Bob McMahon, a former employee.

Madoff was even more obsessed, if that's possible, with cleanliness. Even while he was responsible for billions of dollars, it was not uncommon to see him dusting his office or the two-foot sculpture of a screw behind his desk. One staffer recalls getting off the elevator to find Madoff, clad in one of his innumerable tailored suits, on his hands and knees in the lobby, straightening the rugs so that they were aligned perfectly.

That was Madoff's third fixation. Everything needed to be symmetrical and in straight lines. When Madoff was in the office, all window blinds had to be aligned at the same height, all computer screens had to be arrayed at the same angle and position, and on and on. So insistent was he on perfect alignment that, more than once, he dropped his trousers in the office -- startling female employees -- to ensure that the line of his shirt buttons was precisely vertical. More than one writer has pointed out how odd it was that Madoff, a seeker of the parallel and the perpendicular, should have chosen to house his firm in the Lipstick Building, designed by Philip Johnson and John Burgee in the form of an ellipse.

The Madoff firm had 2-1/2 floors in that building. The trading floor was on 19, and the software programmers worked on 18. Employees in those parts of the firm knew there was a different, lucrative business on half of the 17th floor, but they didn't know exactly what it did. "We were all aware of this hedge fund that had had great returns for 20 years," recalls one trader. "We knew it was statistically impossible [to have the steady gains for which Madoff became famous]. As a collective, we always kind of wondered: How the hell does he do it? Every person was curious. But that's where it stopped. You'd stop yourself from wondering. You'd say, There couldn't be anything bad. The Madoffs had such a name -- and such an aura."

Peter Madoff, a trustee of the Lower East Side Tenement Museum, wrote a line on that institution's website about his family's roots: "My grandparents ran a Turkish bath in the area that served as a focal point for many new immigrants of different nationalities." Census and marriage records show that the Madoff grandparents came to the U.S. from Poland, Romania, and Austria between 1900 and 1905.

Bernie, when he rode through the area many decades later, would occasionally point out places where his family had lived or worked. But though he embraced the family's gritty immigrant success story, he avoided talking about his own parents and his more suburban upbringing. Bernie and Peter Madoff were raised in Laurelton, a middle-class area of Queens. Located beyond the end of the subway line on the border of Long Island's Nassau County, Laurelton felt more like a village in those days than a part of New York City. Families would run into each other at the local Chinese restaurant, the ice-cream parlor, and the Laurelton Jewish Center. The Madoffs -- the parents, Ralph and Sylvia; the boys, Bernie and Peter; and their older sister, Sondra -- lived in a modest three-bedroom brick house with a detached garage on 228th Street, a broad, tree-lined street with a grassy median.

Little is known about the career of Ralph Madoff, and no member of the extended Madoff clan would discuss the family. Ralph gave his occupation as "credit" on his marriage license, and one of Bernie's high school classmates, Ed Heiberger, recalls that he "was either a stockbroker or a customer's man" (the latter is the equivalent of a client or account representative). Years later he would work for his son Bernie's firm. "Ralph looked like a truck driver," adds Joe Kavanau, an old friend of Bernie's. "Kind of a rough-and-tumble kind of guy --not the kind of guy you screw with."

Ralph Madoff wrangled with the government on one occasion. Along with three people, he owed a tax debt of $13,245.28 (about $100,000 in today's dollars) that caused the IRS to place a lien on the Madoff home. The taxes were assessed in 1956, but the lien was not paid off until 1965 after the house was sold, suggesting that Ralph was either fighting the tax bill or unable to pay it.

Like Ralph, Sylvia had a run-in with the government. In August 1963, the Securities and Exchange Commission announced it was instituting proceedings to determine whether 48 broker-dealers, including "Sylvia R. Madoff [doing business as] Gibraltar Securities," had "failed to file reports of their financial condition ... and if so, whether their registrations should be revoked." Then, in January 1964, the SEC dismissed administrative proceedings against a number of the firms, including Madoff's, in what appeared to be a deal: No penalties if you promise to stay out of business.

What's mysterious is that Bernie Madoff's childhood friends don't recall his mother's being involved in stocks or bonds. For a woman to head her own securities firm in the early '60s was unusual. And given that the company's address was listed as the Madoff home in Laurelton, Bernie's friends would seem likely to have noticed the business. Yet they didn't and it's impossible to know why not. One could speculate that Ralph, his name tarnished by federal tax troubles, decided to put his wife's name on the application to open a stock brokerage.

Either way, one of Bernie Madoff's parents was involved in securities -- and got into trouble for it. And according to his friend Joe Kavanau, who attended law school with Madoff (before both dropped out), Madoff knew he was going to go into that line of work from a young age. "Bernie," he says, "was always going to have this business."

Perhaps that explains why most people's memories of the young Bernie Madoff concern his extracurricular activities rather than anything having to do with academics. Most of them, for example, recall his side business of installing sprinkler systems, which he launched as a teenager. "He was a very aggressive kind of kid that wanted to get ahead in life," says his high school classmate Heiberger. "He was a regular guy who was always hustling."

Madoff achieved little distinction at Far Rockaway High School. He was a lifeguard and made the swim team, specializing in the butterfly. But even in this, he didn't excel enough to compete in individual races on a regular basis, according to the team's co-captain, Fletcher Eberle. Instead, Madoff swam in the team relays.

The only other activity that Madoff cited in his senior yearbook entry was "locker guard." This, according to classmates, was a variation on the role of hall monitor. During a more innocent time, the mid-1950s, when fears of student misbehavior centered on truancy and pranks rather than drug use and shootings, the future Ponzi schemer was deputized by school authorities to prevent horseplay in the locker area.

One constant in high school was Ruth Alpern, Madoff's sweetheart. They were a couple, says Jane Kavanau, one of Ruth's old friends, "from early high school, maybe even from when she was in eighth grade." Bernie was smitten by the ebullient, energetic girl who also had an excellent head for numbers. Every morning he would pick Ruth up at home, and they would ride the train together to high school.

Madoff left home to attend college, passed a lonely semester at the University of Alabama, and then returned, according to two sources, because he was pining for Ruth.

He began commuting to what was then Hofstra College, 10 miles across the city line in Long Island. His studies seemed almost incidental. What mattered to him were work and family. The day before Thanksgiving in 1959, he married Ruth at the Laurelton Jewish Center. Two days later he found the time to fill out an SEC application to register his own self-named broker-dealer firm. He later appended a "financial statement" to the application. It consisted of seven words: "Assets: Cash on hand $200. Liabilities None."

Madoff hadn't even graduated -- that came in 1960 --and he had a tendency to get flustered or tongue-tied around people. But he didn't lack for determination. And he had another quality, which Joe Kavanau puts in earthy terms: "I guess the word is 'balls.' "

Even as Madoff continued his schooling -- he spent a year at Brooklyn Law School -- he plunged into the securities business. Six months in, he reported a single stock position: 12 shares of a company called Electronics Capital, worth a total of $300. But by the end of 1961, his initial $200 stake had grown to $16,140, according to his SEC disclosures -- a significant sum in those days for a firm that consisted solely of Bernie and his wife/bookkeeper, operating at first from a shared desk at her father's accounting firm.

Madoff specialized in over-the-counter stocks, the unglamorous, mostly small-company shares that didn't trade on an exchange. He was a wholesaler, a person who would buy and sell small-company stocks to brokers whose clients were looking to invest or to exit a position. "In those days," Madoff explained in a 2007 panel discussion, "over-the-counter stocks were traded always over the telephone with no automation. So you would call a broker; the broker would call up over the telephone any number of dealers like myself, and there were hundreds of dealers around the country that were making these markets."

This was not the staid institutionalized world of the New York Stock Exchange. Since they didn't trade on a centralized exchange and there was no technology to provide up-to-date prices, over-the-counter dealers could -- and did -- take all sorts of liberties with their quotes. "A lot of people started referring to the over-the-counter market as the under-the-counter market," said Gordon Macklin, the late president of Nasdaq, in the Wall Street history What Goes Up.

Madoff was successful from the beginning, and his capital account began mounting: By 1967 he was reporting $127,517 to the SEC. In 1969 it had reached $555,157, and in 1973 it was listed as $1.1 million.

By this point Madoff had also been quietly managing money for years. There was no hint of this on his SEC forms. But beginning sometime in the early 1960s, he had started taking on investors. It originated with a small nucleus of family and friends, and then spread outward in larger and larger circles. For example, Carl Shapiro, an apparel executive who had met the young investor and been impressed by him, gave him tens of thousands to invest in the early '60s. Shapiro would stick with him for close to half a century, losing around $545 million when Madoff's scheme collapsed.

Another key figure was Ruth's father, Saul Alpern. He not only let his son-in-law share a desk at his accounting firm but also channeled clients and friends to Madoff. Eventually, according to Michael Bienes, who joined Alpern's firm in 1968, Alpern began gathering smaller investors together and creating a fund that invested with Madoff as a single account. This was among the first of what came to be called feeder funds.

Madoff was adept at subtly cultivating relationships with people like Bienes. The accountant had represented Madoff in a successful audit in the late 1960s. Then, little by little, Madoff began drawing him in. "I got to know him," Bienes says. "I once went swimming naked with him. He invited me to the New York Athletic Club on Central Park South [where members swam in the nude at the time]. He asked me to come and meet him and get a rubdown ... We didn't discuss anything, really. I think he wanted to get the feel of me, you know, and bring me into his orbit." Bienes evidently won Madoff's trust, and when Alpern retired in the mid-1970s, his feeder fund was passed to his accounting partners and became known as Avellino & Bienes.

Around this time, Bienes recalls, Madoff invited him to the bar mitzvah of one of his sons. "It was a lunch," Bienes recalls, "a buffet lunch. And I was very impressed because he didn't go over the top. He was a wealthy guy, you know, but he did it in a very moderate way. And I remember my partner, Frank Avellino, and myself and Bernie meeting in the middle of the dance floor, and we were saying, 'Thanks for having us,' and he said, 'Hey, come on -- we're family, aren't we?' And at that moment, he had me. He had me. We were family. Oh, my God! I was in! It really took me because he had a presence about him, an aura. He really captivated you." Bienes, who ultimately lost his entire savings to Madoff, still seems dazzled decades later. (Another part of the appeal, according to Bienes's lawyer, Mark Raymond, was that Madoff led Avellino & Bienes to believe they were his only investing client. "I honestly thought we were the one and only," says Bienes, who says that he and his partner jokingly referred to Madoff as "our boyfriend.")

In those days Madoff would tell investors he was employing a much different investing strategy from the split-strike conversion approach that would later become synonymous with his fraud. Madoff explained the early strategy in a 1992 Wall Street Journal article: Before 1982 or so, "Mr. Madoff confirms ... [investors'] money was being used to engage in so-called convertible arbitrage in securities of such companies as Occidental Petroleum Corp., Limited Stores Inc. and Continental Corp." Madoff invested in high-yield issues that were convertible into common stocks while simultaneously short-selling the common stock, the article explained. Investors then earned "the spread between the higher dividend paid on the convertible securities and the lower dividend on the common stock, plus interest from investing the proceeds of the stock short sale."

Even as Madoff was planting the first seeds for his future role as a Ponzi schemer, he got a firsthand lesson in fraud: He was fleeced by one of the great charlatans of the 1960s. The perpetrator was a con artist with the evocative name of Jack Dick, who was sanctioned by the authorities multiple times and yet regularly managed to launch new schemes. His largest and most famous operation was known as Black Watch Farms, which sold investments in Angus bulls in the days when tax shelters were the rage. Dick himself became a wealthy and prominent figure in society. The New York Times' Gay Talese chronicled a 1964 bull auction conducted by Dick that was attended by the likes of U.S. Senator Al Gore Sr. and a representative for former President Dwight Eisenhower. Newspapers described Dick's "opulent" life in a mansion that had formerly belonged to the mother of an owner of the New York Yankees.

Then it all collapsed. Dick was accused of embezzling $3.2 million from Black Watch's bank but died before the case could be resolved. Madoff, who had committed $85,000, was one of many left holding the bag. The press descriptions of Dick's downfall resonate today. "He's one of the most brilliant persons I ever met," said one victim quoted in a 1971 Wall Street Journal article. The article noted, "If he has any flaw, one critic says, it's confidence in his own judgment that is so excessive it borders on a belief in his own infallibility."

Long before Madoff attained infamy as a criminal mastermind, he earned respect as a pioneer in electronic trading. Yet Madoff apparently wasn't satisfied with his place in history and was prone to embellish it on occasion. Such fibbing may be the moral equivalent of failing to plug the parking meter for your getaway car while you're inside -- in Madoff's case, robbing a bank of $65 billion. Still, he felt the need to puff up his credentials.

Consider how he described the creation of Nasdaq. Launched in 1971, it was a primitive computer system that displayed stock quotes -- hence the name National Association of Securities Dealers Automated Quotations. The system simply listed the bids and offers; it was not until a decade later that it became possible to use Nasdaq to trade stocks. Said Madoff at a 2007 panel: "In about 1971 computers were showing up and being used. So we -- meaning my brother and myself -- saw that there was an opportunity to bring automation in the over-the-counter marketplace and create some visibility and transparency in the marketplace. So we came up with the concept of developing a screen-based trading mechanism where prices would appear on a computer screen. That was the start of Nasdaq." The way Madoff told it, his firm and four others "made a proposal to build a screen-based trading system, which then became Nasdaq. Then that went through various stages of automation, so that you were able to turn on your computer screen and any brokerage firm in the country would list all the dealers that were willing to trade the security and the prices. Then that eventually went on to where you could actually trade the security automatically."

That account is largely correct -- except for Madoff's role in it. Says Charles "Dick" Justice, who started with the National Association of Securities Dealers in 1968 and was its chief technology officer for decades (and knows Madoff), "he wasn't involved in the founding of Nasdaq at all." Asked about a separate Madoff comment that he was "involved in the design of the Nasdaq technology," Justice says, "No, he wasn't."

According to Justice and others who played roles in early electronic trading, it was only in the late 1970s and early 1980s that Madoff made his mark. And when he did so, it wasn't because his firm created the concept of electronic trading -- it was because the Madoffs were among the first to recognize the value of the idea and designed software that could trade stocks electronically in seconds. "If you have a brokerage firm that advertises they will get their trade done with you in five seconds," says one longtime Madoff tech employee, "that's because our system will get it back to them in two. That's the innovation."

Trading through Madoff was not only fast -- it was cheap. Actually, "cheap" understates the matter. Rather than taking a fee for trading stocks, as NYSE specialists did, Madoff paid firms like Charles Schwab and Fidelity a penny or two a share for their orders, a practice known as "payment for order flow." In those days, there was a prevailing spread of at least 12.5¢ between the price that a "market maker" like Madoff's firm paid to buy shares and the price at which it would sell the same shares. Using its own software, Madoff's firm was adept at hedging the risk that buy-and-sell orders would be out of balance, preserving its profit. So even if he gave away a penny, Madoff could still make a tidy sum.

The allure for customers was obvious. And these ultra-cheap, fast electronic trades were among the things that helped discount brokers like Schwab and Fidelity slash commissions and bring stock trading to the masses.

By the early 1990s, Madoff's firm alone was executing 9% of the daily trading volume of stocks listed on the New York Stock Exchange. Madoff's realm was known as the "third market." His firm specialized in trading Big Board shares outside of the exchange. Such trading had existed for decades, but Madoff's firm led the charge as it went electronic. "He was viewed as the leading third-market firm on the Street," says former Nasdaq president Joseph Hardiman, who became close to Madoff. "He was very much respected and listened to by his peers."

His peers did not include the specialists of the New York Stock Exchange. That group viewed Madoff with disdain. They likened order payments to kickbacks. And they were incensed at being placed at a competitive disadvantage by this outsider. "We are being forced to play full-contact football in tennis whites," sniffed one specialist to the Wall Street Journal in 1990. The anger and condescension still linger today. "The Madoffs were poaching scallops from my plate," says one retired NYSE director. He dismisses Madoff himself as nothing more than a "chiffonnier" -- a ragpicker.

Call it shabby if you want. Payment for order flow was legal, and Madoff fought to keep it so. Under pressure from the SEC, the NASD, the securities industry's self-regulatory body, assembled a panel to study the issue in 1990. At the time, payment for order flow was highly controversial, and opposition was intense.

Madoff, who was named chairman of Nasdaq that year, played a key role. Not only did he serve on the panel, but he also suggested witnesses to interview. Managing to cast himself as a statesman who just happened to be the most knowledgeable man in the room rather than as an advocate fighting to protect his livelihood, Madoff took the lead in the discussions.

Slowly and subtly, he steered the group to his line of thinking, four members recall. "He wasn't pushy about his view," says David Ruder, a former SEC chairman and head of the panel. "He wouldn't say, 'We've got to protect my business.'" Instead, Madoff would tell the members, "You have just got to understand it." During the process, says Ruder, "we got pretty chummy."

When all was said and done, Madoff prevailed. The panel endorsed payment for order flow in its 1991 report, concluding that the practice was no different from other inducements offered on Wall Street. "The report put the NASD imprint on the process," says Norman Pessin, a committee member who admires Madoff's political skills. "It legitimized his business." Eventually the SEC followed, giving its own imprimatur to the payments as long as they were disclosed.

For Madoff it was a sweet victory, one that cemented his role as a force in trading. The years that followed marked the lucrative peak for Madoff's market-making firm, earning him millions in honest profits.

But beginning in 1997, the rules governing trading spreads changed. They were slashed from 12.5¢ a share to 6.25¢ that year and then dropped to a penny in 2001. Madoff's firm, which had eschewed traditional commissions and made its money on the spread, watched its profit margins evaporate. Madoff's market-making operation would never again be the prodigious cash generator it had been. Indeed, there were times after the turn of the century when it would dip into the red.

One of the reasons Madoff was able to perpetrate his fraud for so long was his preference for marketing his investment business by word of mouth. Until the scam's later years, people heard about it from friends. It was a private club, one that, famously, became only more desirable because of Madoff's seeming reluctance to admit new investors. One of the tacit conditions, as we know now, was an understanding that information about Madoff investments -- including their existence -- was to be held closely. Most investors complied. Who would want to anger Madoff and risk losing their privileges?

Still, despite his best efforts, every so often Madoff's secret investment business would emerge publicly. Each time Madoff would spring into action, showing a characteristic mix of reactions. He would take direct control, responding personally. And he would employ his self-deprecating charm.

In 1992, for example, Madoff's name surfaced in a major SEC investigation involving one of his feeder funds. Avellino & Bienes was accused of running an unregistered securities operation, issuing $441 million of notes that promised returns of 13.5% to 20%. SEC officials feared it was a Ponzi scheme. They raced into court, won an injunction to shut the firm down -- and discovered that all the investors' money was safely in the hands of one Bernard L. Madoff. According to court records, Madoff was able to return all the money to Avellino & Bienes in a matter of eight days. (The two men ultimately paid a combined $350,000 in civil penalties to the SEC.)

Once the money was produced, essentially, the SEC exhaled. It didn't occur to the agency to investigate Madoff. Much of the rest of the case was handed over to a court-appointed trustee whose job was to make sure investors were made whole, and to what was then Price Waterhouse, which tried to reconstruct the mostly nonexistent books of Avellino & Bienes.

What's striking is that Madoff appears to have played the role of model citizen in this case. Billing records show that Lee Richards, the trustee, and Joel Whitman, who then worked for Price Waterhouse, held multiple phone conversations and at least one meeting with Madoff, who was able to provide investing records when Avellino & Bienes couldn't. They also show Madoff personally handling requests for computer records and the like, the sort of routine queries that in almost any other firm would have been handed off to the chief technology officer or a more junior person.

Madoff's personal touch seemed to score points. Whitman testified that Madoff was "forthright" in answering his questions. (Whitman said he couldn't comment for this article unless Richards, his client, granted permission. Richards did not respond to e-mails and phone calls.)

In May 2001 a more probing spotlight was shone on Madoff, and once again he escaped. In that month, two articles -- the first in a trade publication called Mar/Hedge, the second in Barron's -- raised serious questions about Madoff's investment operation. For starters, its very existence was surprising: According to Mar/Hedge, its $6 billion to $7 billion in assets under management made it the largest or second-largest hedge fund in the world at the time. Yet it was unknown. The articles went on to note the improbability of Madoff's smooth and steady 15% annual returns. They wondered why Madoff charged no fees to run his seemingly successful investment operation and instead accepted only minimal trading commissions.

Once again, Madoff got personally involved. The Mar/Hedge article noted that "Madoff sounds and appears genuinely amused by the interest and attention aimed at [his] asset-management strategy," and he pooh-poohed his own investing success, waving it off as the benefit of a bull market.

Madoff does not appear to have swayed either reporter, and both articles had a skeptical tone. Barron's asserted, for example, that "some on the Street have begun speculating that Madoff's market-making operation subsidizes and smooths his hedge-fund returns." Madoff was quoted dismissing that notion as "ridiculous." (As it happens, the opposite hypothesis was common among employees of Madoff's legitimate business. "We had a sense he was probably paying rent from the asset management," says a trader who worked for Madoff at the time.)

So what happened when two publications, one of them among the most prominent on the subject of investing in the country, raised questions about Madoff? Nothing. What seemed like clear warnings disappeared into a void of indifference. Even inside Madoff's firm, the reaction was a shrug. "We knew about the Barron's article," recalls the trader. "We went on about our business as if it was another firm that had nothing to do with us."

As it would later turn out, Madoff's illegal investment business was indeed subsidizing his legal trading operation. Among the charges to which Madoff pleaded guilty in March were three counts of money laundering, which involved transferring millions of dollars from Madoff's fraudulent business through his London operation to his legitimate New York business. At least $250 million was transferred in this manner, according to the charges.

Then came the closest call: The SEC launched an investigation in 2006. A whistleblower named Harry Markopolos had spent years trying to persuade the SEC that Madoff was running a Ponzi scheme (he had been a key source for the Mar/Hedge article). The SEC also examined whether Fairfield Greenwich, a giant feeder fund, was properly disclosing the extent of its reliance on Madoff.

Madoff had always been terrified of the SEC. "Every time the SEC came into the office," remembers one longtime employee, "Bernie was a basket case." Wherever Madoff was in the world, he would fly back, even for a routine examination. He peppered employees with questions about their preparedness. "What's up?" he would ask nervously. "What's up? What's up?"

This time Madoff was being asked specifically about his fraudulent investment business. Once again he prepared -- not only himself but also his customer Fairfield Greenwich. A phone conversation with representatives of Fairfield Greenwich in December 2005 was taped, transcribed, and made public as part of a Commonwealth of Massachusetts suit charging Fairfield Greenwich with essentially abdicating its responsibility to protect its investors. The transcript provides a revealing example of Madoff's thinking and his ability to manipulate.

"Obviously, first of all, this conversation never took place ... okay?" Madoff began. ("Yes, of course," was the reply from Fairfield Greenwich's risk manager, though the company has since asserted that it informed the SEC of the conversation at the time.) Madoff proceeded to spin a strange, fragmentary -- he seemed to interrupt himself every few words -- self-contradictory set of talking points for Fairfield to follow in its SEC interview.

In reality, Fairfield's Sentry funds had their entire $6.6 billion stake invested with Madoff, and he controlled every investing decision (though, of course, in this case, "investing decision" meant Madoff simply took whatever money was sent his way). But he reminded them of their cover story: "You've approved the parameters of the strategy, and I've agreed to follow these." Fairfield, he kept repeating, had selected the strategy and a range of stocks, and Madoff's only role was to control the timing of when these investments were entered into and exited. "[W]e never wanted to be looked at as the investment manager," he said. "So in the past, if we've ever been asked about what our role is with any of these types of funds, it has always been that we are the executing broker for these transactions." Having just said that Fairfield had the sole power to choose the investing strategy, Madoff turned around and explained to them that he had changed the "trading directives" several years ago and was only now getting around to informing Fairfield Greenwich that its strategy had changed. "I'll send you up the new trading instructions today," Madoff said blithely.

Madoff was telling Fairfield to deny the obvious: that he was managing their money. At the same time, he portrayed his firm's role as something well known to the SEC. "They're aware of the fact that we do this," Madoff said, adding later, "The commission knows how we -- how we operate." (An SEC spokesman declined to comment.)

Madoff went on to disparage the SEC investigation as a "fishing expedition," saying that "these girls" -- the SEC's lawyers -- might not understand the strategy, and implying that they might not press too hard because SEC lawyers have ambitions to go into lucrative private practice and don't want to alienate the sorts of firms that might hire them. "It's none of their business," he added. Madoff, who appeared at times to be reading from a list of bullet points, also advised the Fairfield Greenwich team on the tone they should take. "You don't want them to think that you're concerned about anything ... You're best off [if] you just be, you know, casual." Fairfield has said it told the truth to the SEC.

When it was his turn to be interviewed by the SEC, in May 2006, Madoff flat-out lied. When he was asked, for example, "Is it correct, then, that the equities are traded in Europe?" he responded, "Yes." (Madoff often told people he made all sorts of trades in Europe, where it would be harder to verify what he was doing.) Needless to say, there were no equities being traded in Europe or anywhere else.

Madoff's lies paid off -- at least, at the time. The SEC "found no evidence of fraud," as a staff attorney wrote in a "case closing recommendation" (this despite the fact that the SEC had previously noted that Madoff's firm "misled the examination staff" and withheld information). The punishment: Madoff's firm had to register as an investment adviser.

Today, the radio announcer intoned solemnly, the New York Mets have lost one of their greatest fans: Roger Madoff. Bernard Madoff's 32-year-old nephew, Peter's son, had died on April 15, 2006, from complications related to leukemia. The announcement, aired on the Mets' radio station, was an unusual acknowledgement of a fervent Mets fan. It also reflected the decades-long bond between the team's owners, the Wilpon family, and the Madoffs. (The Wilpons also had millions invested with Madoff, and lost the money.)

Roger's protracted illness shook the entire Madoff family. It was especially devastating for his sister, Shana, a compliance lawyer at the firm. Roger and Shana "were like stamp and envelope," recalls one employee. "You couldn't separate them." Peter Madoff was in even worse shape. Peter had been a frequent visitor to the hospital, bringing bagels for the nurses and newspapers for his son. A doctor once entered Roger's hospital room to find Peter tenderly applying ointment to his dying son's feet. Chauffeured home in his BMW on the Long Island Expressway, Peter would weep quietly in the back seat.

Cancer reached deep into the Madoff family. Peter had survived a bout of bladder cancer in 2000, and Bernie's son Andrew was in treatment for lymphoma. Another nephew, who also worked at the firm, was preoccupied with his young daughter's leukemia treatment. "We should curse the Madoff bloodline," Roger wrote in a posthumously published book on his struggle with the disease.

As Roger got sicker and sicker, the family channeled most of its philanthropy, which swelled into eight figures, into cancer research. "I hadn't realized the extent of the wealth that existed there," Roger noted with some surprise in his book.

By then, Bernie Madoff's "investment business" had ballooned. According to research by Harry Markopolos, it grew from as much as $7 billion in 2000 to as much as $50 billion by the end of 2005. What had started decades before as a small-time recruiting effort by Madoff agents at country clubs had gone global. Massive international institutions such as Grupo Santander, Fortis Bank, and Union Bancaire Privée were all funneling billions -- sometimes through intermediaries -- to Madoff, lured by the call of steady 10% to 12% returns. Even one of the world's biggest sovereign funds, the Abu Dhabi Investment Authority, ended up sinking tens of millions of dollars into the Ponzi scheme via its investment in one of the big feeder funds.

"Bernie's world" is the phrase Bob McMahon uses to describe the operations on the 17th floor. McMahon, a project manager specializing in information technology, was brought in to help rationalize the company's systems from 2007 to 2008. The situation he found was odd, especially for a firm whose legitimate business had been built on software prowess.

Traders had begun grousing about the firm's proprietary MISS software and the decades-old mainframe it ran on. The system was designed to trade equities; reconfiguring it to trade anything new was cumbersome. But replacing the mainframe wasn't so simple, says McMahon. It would also entail replacing a venerable IBM server, the AS/400, which served as the investment business's main computer backbone.

"Managing the AS/400 was getting to be a very, very hands-on, manual process," recalls McMahon. But "Bernie never wanted to get rid of [it]. That was the books and records of quote 'the company.'"

There were other idiosyncrasies in Bernie's world that might have raised suspicions. Around 2002 he proposed eliminating e-mail throughout his firm but was persuaded not to. Lots of Wall Street firms were talking about restricting it in the wake of corporate scandals featuring incendiary messages, but Madoff ultimately did the opposite of what you'd expect. He allowed e-mail for staffers at his trading business -- the one the SEC regulated -- while abolishing it for the people working in the unregulated investment business on 17.

Madoff took another step. He decreed that e-mails would no longer be stored electronically. First he decided that each of the firm's e-mails would be printed and then stored in boxes, but he was persuaded by others that such a plan was impractical. In the end, Madoff ordered that old e-mails be transferred to microfiche, a cumbersome process that costs much more than archiving the records digitally. Why would Madoff want to increase his archiving costs? Perhaps it had to do with the fact that microfiche is orders of magnitude more difficult to search than electronic records.

The 17th floor seemed like a galaxy far removed from the rest of the company. Most of the people there were a different breed from the overachievers upstairs. Many had arrived at Madoff's firm straight out of high school. "This was the only world they ever knew," says McMahon. "It was the old analogy of mushrooms: You keep them well fed and happy in the dark."

For weeks at a time, it was a torpid operation. Employees tended to disappear for long stretches of time -- for lunch, for vacation, for anything. Then, six to eight times a year, a frenzy would erupt. Madoff's purported investing strategy was the "split-strike conversion." We'll spare you the details -- they seem beside the point, given that Madoff didn't actually execute this strategy -- other than to note that he claimed it consisted of a "basket" of 35 or so large-company stocks hedged with stock options. In theory Madoff's investing genius consisted of knowing the best time to enter or leave the market. Ostensibly, every so often Madoff's team was "buying" or "selling" massive quantities of stocks and options. Each time that happened, the 17th floor team would spring into action and spend all-nighters churning out trade confirmations for thousands of customers.

Presiding over this process was Frank DiPascali. Raised in the blue-collar Queens community of Howard Beach, he was a high school graduate who had arrived at Madoff's firm in 1975 -- and then spent the next three-plus decades there moving through an unusual combination of legitimate jobs (at various times he was a gofer, a stock trader, and the person who coordinated the firm's move to new offices in 1987) before assuming his ultimate role as the chief lieutenant in Madoff's investment business.

DiPascali shared his boss's love of the sea, and like Madoff, he spoke with a distinct New York accent. In his mouth, the word "three" had no "h." DiPascali came to work in an incongruously starched version of a slacker's uniform: pressed jeans, a sweatshirt, and pristine white sneakers or boat shoes. He could often be found outside the building, smoking a cigarette.

Some customers found DiPascali off-putting. "I'd call Madoff and they would put me on with Frank," recalls Carl Englebardt, a longtime investor. "Quite frankly, when I was talking to him, I thought I was talking to someone in the Mafia. He didn't sound very professional to me. He never inspired a lot of confidence."

He may not have looked or acted like a financier, but when giant customers like Fairfield Greenwich came in to talk, DiPascali was usually the only Madoff employee in the room with Bernie. Madoff told the visitors that DiPascali was "primarily responsible" for the investment operation, according to a Fairfield memo.

As the business ballooned to ever more massive proportions in its final years, DiPascali complained of overwork. He even begged Madoff not to add more customers. "No more! No more!" he was heard pleading on several occasions. But the boss kept signing them up until the very end.

The storm broke in 2008. The markets began a calamitous and accelerating decline. With their non-Madoff investments pulverized, more and more customers turned to what they thought was their most solid holding: They began requesting withdrawals from Madoff's fund.

For a time, Madoff seemed to defy the worst collapse since the Great Depression. While double-digit monthly drops suddenly became common, Madoff was somehow eking out a heroic positive return, ostensibly 4.5% through October.

Madoff's investors nervously hung on the firm's every word in e-mails that read now as tragicomedy. On Sept. 15, when Lehman Brothers collapsed and Merrill Lynch announced its sale, Fairfield Greenwich executives circulated e-mails describing Frank DiPascali's reassurances that Madoff wasn't using those firms as counterparties and his assertion that Madoff did "not want to sell into weakness." On Nov. 4, another Fairfield executive reported that DiPascali had told him that "they have their buying hats on."

Madoff appeared to be his smooth old self. In November he sat down with members of the investment committee for the American Jewish Congress, one of the nation's oldest Jewish philanthropic organizations. The group's president, Richard Gordon, asked how Madoff could be making money in one of the worst markets in history. "I could explain it to you, Richard, but it's really complicated," Madoff replied evenly. "I'm a steady and true investor." He gently tried to put Gordon on the defensive. "Aren't you happy with the returns?" Madoff asked. Gordon left the meeting as confused as he had been when he arrived. But he had no reason to doubt Madoff's integrity, he says, or to imagine there was a problem. Madoff, he says, was "extraordinarily avuncular -- calm, direct, and to the point."

Madoff was keeping up his façade at work. But at home his desperation had begun to show. In November and early December, he asked his wife to make two transfers totaling $15.5 million from a brokerage account to her personal bank account so that the cash would be at hand. Madoff had never made such a request before, two sources say. Ruth has insisted her husband didn't inform her of the fraud until the day before he was arrested. She maintains, according to one of these sources, that Bernie said he needed the cash to pay customer redemptions.

By this point, $15.5 million was a pittance compared with what he needed. As of early December, investors had demanded the return of some $7 billion. If Madoff truly withdrew his wife's money for that purpose, he had reached the point where he was rooting around in the sofa cushions for loose change.

The man once famous for rebuffing potential investors was now openly soliciting the ultrawealthy: Ken Langone, the Pritzker family, and others were invited to invest. And Madoff leaned on some of his most loyal investors for cash infusions. Carl Shapiro ponied up $250 million. Some of the principals at Fairfield Greenwich added another $15 million. But it just wasn't enough.

On Dec. 8, Madoff's cool veneer finally cracked. He berated Jeffrey Tucker of Fairfield Greenwich over that fund's inability to replenish the money that had been withdrawn from the firm. He threatened to close Fairfield's account and warned that there were plenty of other institutions that could take its place. His traders, Madoff said, were "tired of dealing with these hedge funds."

There is no better indication of the hold that Madoff exerted over his investors than Tucker's response. Tucker, after all, was co-founder of a $6.6 billion investor in Madoff's firm. In normal circumstances, a client of that magnitude would expect to be coddled. Instead, Tucker fretted about what he could do to placate Madoff. "We best talk," he told colleagues in a worried e-mail that day. "I think he is sincere."

Two days later Tucker sent a pleading letter to Madoff. He apologized for not keeping him better informed. "Our firm is very dependent on its relationship with your firm," he continued. "You are our most important business partner and an immensely respected friend ... Our mission is to remain in business with you and keep your trust." Tucker's lawyer, Marc Kasowitz, says his client "was deceived by Bernie Madoff just like the SEC and hundreds of other very sophisticated investors."

Madoff may never have seen the letter, for that was the day his fraud came apart. That afternoon Madoff drove up to his apartment with his two sons. There, as the world would soon learn, he apparently confessed his entire crime.

Afterward the sons proceeded to their lawyer's office, setting in motion the chain of events that led to their father's arrest. Madoff himself came downstairs a few minutes after the sons. According to one person who saw him then, he was as "calm as ever." Madoff returned to the office and then joined his wife at the company's holiday party at a local Mexican restaurant. According to employees who were present, Madoff seemed his usual self. But Mark and Andy never showed up.

As his black Mercedes S550 made its way north from Manhattan's federal courthouse to his apartment the afternoon after the holiday party -- the day he was arrested -- Bernie Madoff told his driver nothing about why he had been at the judicial complex for hours. It wasn't uncommon for Madoff to be silent, and only later did the driver grasp the meaning of the one observation Madoff did make: "All my life, I've watched the evening news. But tonight I sure won't be watching."

Within hours, Bernard Madoff, wise man of Nasdaq, had been transformed into Tabloid Bernie, the $65 Billion Villain. Almost as fast, Madoff's life collapsed into isolation. Only two people would visit him and his wife during his three months under house arrest, and neither was a close family member. Mark and Andy haven't called since Bernie's arrest. "They've had no desire to talk to their parents," says a person close to the sons.

Dozens of agents from the Federal Bureau of Investigation, the SEC, and the Securities Investor Protection Commission descended on the offices of Madoff's firm. The 17th floor was designated a crime scene, and guards were posted. The staffers who worked on 17 were herded to a small conference room near the coffee machines on the 18th floor, where they sat nervously in what some of them called "office arrest." One by one they were taken to be questioned by the FBI. The company's computer and e-mail systems were shut down, so dozens of staffers passed the time watching movies, playing cards, and talking.

Several days after the feds had locked down the office and told staffers not to remove anything, Peter instructed several employees to carry four boxes and two shopping bags filled with documents downstairs, where his driver was waiting with his own Ford Explorer (the company vehicles were now off-limits). The driver was halfway to the offices of Peter's lawyer when the authorities discovered what was happening. An agitated federal agent called the driver and told him to turn around immediately. When the driver arrived back at the Madoff offices with his cargo, a teary Peter told him, "Sorry I got you involved in this." Peter was assigned an armed FBI "escort" to accompany him wherever he went on the premises that day and later was told not to return at all. A lawyer for Peter Madoff, John Wing, calls the incident "a misunderstanding" between Madoff's office and the FBI over "the removal of his personal files and other personal items."

The Bernie Madoff who appeared in court in March was a diminished figure, a sad version of the vital, regal person he'd been just a few months before. Gone was the smirk that some had detected in the videos of him right after his arrest. From 10 feet away in the jury box, where a handful of reporters were seated, one could detect what looked like turbulent currents under the placid exterior. Even with his eyes closed, Madoff blinked furiously at moments, his eyebrows spasming above the top of his rimless glasses. His hands betrayed his tension: At times he gripped and twisted his pen; he cracked his knuckles; he steepled his hands so hard that his fingers trembled.

The impression was of a mighty attempt at control. And somehow, Madoff managed to preserve a modicum of dignity, even as he pleaded guilty to 11 charges of fraud, theft, money-laundering, and perjury and absorbed the anger directed at him from the audience, where his victims watched. One of them addressed Madoff directly: "I don't know whether you had a chance to turn around and look at the victims," he said angrily. Madoff hesitated and then wheeled awkwardly in his seat as the judge admonished the victim for speaking to Madoff rather than to the court.

When the judge remanded him to custody that day, Madoff silently pulled his shoulders back and allowed himself to be handcuffed. The cuffs, which gleamed as if freshly polished, seemed somehow suited to the fastidious elegance of the defendant. And then Madoff was gone, likely never to take another step on free soil. He awaits sentencing on June 16. And even if he doesn't get the maximum 150 years, whatever he does receive will effectively be a life sentence for a 71-year-old.

The federal investigation proceeds. Less than a week after Madoff's plea, the firm's outside accountant, David Friehling, was charged with criminal fraud for years of signing off on phony statements. (Friehling's lawyer, Andrew Lankler, declined to comment.) The charges did not assert that Friehling knew of the Ponzi scheme. Friehling now appears to be trying to negotiate a deal with prosecutors.

Investigators continue to try to locate Madoff assets -- a bit more than $1 billion has been discovered so far, with specialists now fanning across the world's offshore locations. The court-appointed trustee, whose job it is to gather assets, has hired lawyers in the Cayman Islands, Gibraltar, and Luxembourg, with more jurisdictions likely to come. They're uncovering $50 million here, $75 million there. What isn't going to happen is the miraculous discovery of a giant vault with $65 billion in cash. That's because that $65 billion -- the most widely cited figure for the size of Madoff's heist -- is a fiction and always was. It's a tally of the stated value of all the account statements of every Madoff account holder as of Nov. 30. The total includes, in some cases, decades of fabricated returns. According to experts, the actual amount investors gave to Madoff over the years is probably closer to $20 billion. But even that outlandish sum will never be found; it was chipped away year after year after year. That, after all, is the definition of a Ponzi scheme: Most of the cash put up by new investors went to pay the old ones.

Put another way, if Madoff had still enjoyed access to large sums of cash in December, he would have continued paying his investors. The collapse of a Ponzi scheme means there is no money left. In the end, victims will likely collect only a tiny fraction of what they lost -- and some substantial portion of that will come from other Madoff investors who had appeared lucky enough to pull their cash out before the entire edifice crumbled.

This is arguably the most prominent financial crime ever, and the prosecutors -- who declined to be interviewed -- have to be aware that the public's rage won't be placated with the conviction of Bernie Madoff. So it will likely come as a huge relief to the Madoff family that DiPascali is telling prosecutors they were not participants in the scam. After all, nobody, apart from Bernie Madoff, is better positioned to describe who took part. But it's worth remembering that such a statement represents less than a full exoneration.

One of the most widely made assumptions is that various family members "had to know" what was going on. Frank DiPascali, of course, is not in a position to say what the family knew or didn't know. Representatives for all the family members have declared their innocence.

Even if Bernie Madoff never informed his family members of the fraud, there were a number of events that could have -- perhaps should have -- raised their suspicions. As the people in charge of the legitimate Madoff businesses, Peter, Mark, and Andy knew or should have known, for example, that some $250 million had been transferred from the Madoffs' London office to their business. That cash, Madoff later admitted, was money laundered from the illegitimate operation to the legitimate one. (Those funds, it turns out, were crucial. In court, prosecutor Marc Litt asserted that "at times, his [legitimate] firm would've been unable to operate but for the cash generated by this Ponzi scheme.") A lawyer for Mark and Andy Madoff says, "They had no knowledge whatsoever that their father engaged in any fraudulent activities, including allegedly fraudulent transfers of funds through Madoff Securities International in London."

Whatever happens, Peter, Ruth, and to a lesser extent the other Madoffs have many years of civil litigation to look forward to as various individuals, funds, and government entities try to recover whatever assets they can find.

As for DiPascali, his potential testimony may provide some good news for at least one feeder fund. According to a person familiar with the matter, DiPascali has no evidence that Fairfield Greenwich's top brass knew of the scam.

But DiPascali could spell trouble for certain key Madoff customers. DiPascali, according to this source, admits manipulating the returns of several clients, jiggering them up or down -- phantom gains added or reduced -- to suit their needs. Says the source: "This is a group of inside investors -- all individuals with very, very high net worths who, hypothetically speaking, received a 20% markup or 25% markup or a 15% loss if they needed it." The investors would tell DiPascali, for example, that their other investments had soared and they needed to find some losses to cut their tax bills. DiPascali would adjust their Madoff results accordingly.

According to this source and a second one familiar with the investigation, these special deals for select Madoff investors have become a central focus for federal prosecutors. The second source describes the arrangements as "kickbacks" and "bonuses." A spokesperson for the U.S. Attorney declined to comment. But a little-noticed line in a public filing by the prosecutors in March supports at least part of these sources' account. The document that formally charged Madoff with his crimes asserted that he "promised certain clients annual returns in varying amounts up to at least approximately 46 percent per year." That was quite a boost when most investors were receiving 10% to 15%. It appears to reflect the benefits that accrued to those who helped bring large sums to Madoff.

As for Madoff himself, he has traded a 4,000-square-foot penthouse for a 76-square-foot jail cell. The bespoke charcoal suits have been replaced by an orange jumpsuit. Even so, one person close to the family says he's bearing up well in jail. He's exercising. He is reading a lot of books. "He makes the best of it," adds this person, who says that Madoff looks surprisingly good these days. Perhaps that's because for the first time in decades, Madoff has no secret weighing him down.

That burden has been passed. To his family members, whose name is eternally blackened whether or not they were involved. To his former employees, who lost their livelihoods and are now struggling to get new jobs with the taint of his company's name on their résumés. And most of all, to his victims, many of whom are struggling to make ends meet. Madoff left a historic mess. It's going to take a long time to clean it up. ![]()

-

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More

The retail giant tops the Fortune 500 for the second year in a row. Who else made the list? More -

This group of companies is all about social networking to connect with their customers. More

This group of companies is all about social networking to connect with their customers. More -

The fight over the cholesterol medication is keeping a generic version from hitting the market. More

The fight over the cholesterol medication is keeping a generic version from hitting the market. More -

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More

Bin Laden may be dead, but the terrorist group he led doesn't need his money. More -

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More

U.S. real estate might be a mess, but in other parts of the world, home prices are jumping. More -

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More

Libya's output is a fraction of global production, but it's crucial to the nation's economy. More -

Once rates start to rise, things could get ugly fast for our neighbors to the north. More

Once rates start to rise, things could get ugly fast for our neighbors to the north. More