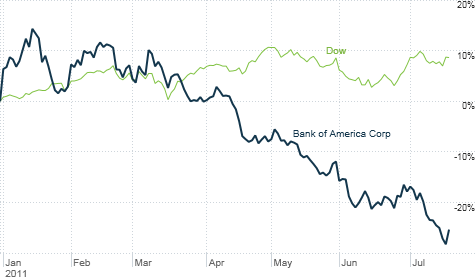

Bank of America is THE dog of the Dow. Shares have plunged this year due to legal worries and concerns it may have to raise more capital.

NEW YORK (CNNMoney) -- It is a company that faces enormous legal risks. Critics claim the CEO is not the right man for the job. Its stock price has tanked.

No. I am not talking about News Corp. (NWSA, Fortune 500) and Rupert Murdoch. I am referring to Bank of America (BAC, Fortune 500) and Brian Moynihan.

BofA posted an $8.8 billion quarterly net loss on Tuesday. Sure, this was expected. But that didn't matter to traders.

The stock fell 1.5% Tuesday -- a day when the broader market and several other top banks, including Wells Fargo (WFC, Fortune 500), JPMorgan Chase (JPM, Fortune 500), U.S. Bancorp (USB, Fortune 500) and Keycorp (KEY, Fortune 500), enjoyed gains. BofA hit a new 52-week low. It's down 25% year-to-date and recently surpassed Cisco (CSCO, Fortune 500) as the worst performer in the Dow.

Although shares bounced back 4% Wednesday, BofA's stock price remained below $10. Ouch! That's important because investors tend to view stocks with single-digit prices as the financial equivalent of lepers.

Bank of America has a lot going against it. Many state attorneys generals are still looking into problems tied to the mortgage foreclosure robo-signing scandal. And a group of angry investors is threatening to block BofA's proposed $8.5 billion settlement with large institutions over a bad batch of mortgage securities.

The sentiment is undeniably negative, which is a stunning turn of events for BofA and CEO Moynihan.

It was only last year that many financial experts were dubbing Moynihan as President Obama's favorite banker. The thought was that BofA was taking the lead on various financial reforms proposed by the White House. (Heck, CNNMoney had a story with the headline of "Bank of America's King Midas" in May 2010.)

Moynihan was believed to be doing a good job of cleaning up the messes tied to the bank's disastrous purchase of subprime lender Countrywide Financial and its desperate acquisition of investment bank Merrill Lynch on the eve of Lehman Brothers's bankruptcy in September 2008.

Controversy surrounding those two deals contributed to the fall from power of Moynihan's predecessor, Ken Lewis, who was forced out as chairman in April 2009 and announced his retirement as CEO a few months later.

Now Moynihan has gone from King Midas to a pariah.

Todd Sullivan, co-founder of Rand Strategic Partners and author of the ValuePlays blog, joked in a Direct Message tweet to me on Tuesday (what a strange new world we live in) that "Moynihan could get up, walk across water and people would say 'Moynihan can't swim.' "

Even investors in the company acknowledge that it's not one of their favorite holdings.

"Do I have to confess that I own some?" joked Blake Howells, portfolio manager with Becker Capital Management in Portland, Ore. Howells said his firm has a small position in Bank of America. And he believes the biggest problem is that investors simply don't trust what management has to say.

The bank has repeatedly maintained it won't need to raise more capital to meet regulatory requirements. Several analysts have agreed with Bank of America and said in reports following Tuesday's earnings that they don't think the bank will need to raise more capital.

A spokesman for the bank added Wednesday that new capital regulations are phased in over time and that Bank of America expects to have levels twice the minimum required ratio by the beginning of 2013.

But some investors don't seem to believe this claim since many banks said similar things in 2008 before the financial collapse. So it may be a case of "the bank doth protesting too much me thinks" if you want to go all Hamlet.

Howells said it all comes back to what investors view as broken promises.

"I don't think Moynihan is Ken Lewis 2.0 since Lewis was a serial acquirer. But investors have been frustrated with estimates that management has made that are now getting changed for the worse," he said, referring to the rising cost to settle some of its legal claims.

You can hardly blame investors for doubting the financial health of BofA. While many other rivals were given approval earlier this year to boost their dividends, the Federal Reserve turned down BofA's request. It's still stuck with a measly quarterly payout of a penny per share.

Making matters worse, it actually looks like credit quality, save for mortgages, is improving for big banks, including BofA.

But because of the Countrywide hangover, BofA was not able to benefit as much as its rivals. Better quality trends helped lift second-quarter profits at JPMorgan Chase, Wells Fargo and even Citigroup (C, Fortune 500), the only bank to receive as much bailout money in 2008 and 2009 as BofA. (They both got $45 billion.)

So BofA is lagging at a time when banks finally do appear to be getting their act together. If that continues, Howells says Moynihan's job could be in trouble. But he thinks investors will give him until next year before exerting more pressure on the bank's board to do something.

That's because BofA could actually bounce back sharply if everything goes its way. If it doesn't really need to raise more capital and if it doesn't have to pony up even more than expected to settle all the Countrywide-related legal expenses, Howells said the stock could double from current levels.

But those are big ifs. And if the worst-case scenario unfolds, namely that BofA is forced to raise more capital, the stock could tumble a lot more from here.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()