Better disclosure would help. Your average credit card application is easier to decode than many mortgage documents. Alex J. Pollock of the American Enterprise Institute, in testimony to the House subcommitte on financial institutions today, says that banks should give all borrowers a one page document with the following information.

-Amount of loan -LTV [loan-to-value] ratio -Final maturity -Prepayment fee, if any -Balloon payment, if any -Points and closing costs -Initial rate on loan in % and monthly payment in dollars -How long this rate is good for=when higher rate starts -Fully indexed rate on loan in % and monthly payment in dollars -Your household income on which this loan is based -Initial monthly payment as % of income, and payment plus taxes and insurance as % income -Fully indexed monthly payment as % income, and payment plus taxes and insurance as % income -A name, number and e-mail for you to contact with any questions -An authorized signature of the loan originator -The signature of the borrower.

What's amazing is that all this isn't standard practice already.

(By the way, I'll be blogging fairly lightly this week. The day job is looking like it will be a day-and-night job for a bit.)

At CreditSlips.org, Tara Twomey tells us about one-way ARMs:

The Senate Banking Committee has invited representatives from the top five subprime lending companies to "explain their lending practices in the subprime mortgage market" at a hearing scheduled for tomorrow, March 22. With all the recent focus on teaser rates and no document loans, the one-way adjustable rate mortgage (ARM) probably won't get much attention. An analysis of the actual terms of recent ARM loans, however, shows that one-way ARMs are yet another example of how subprime lenders stack the deck against borrowers.

In its simplest form an adjustable rate mortgage is one in which the interest rate for the loan is pegged to an "index" and for which the interest rate is adjusted at set intervals (e.g., 6 months, 1 year, etc.). If the index increases, the borrower's interest rate increases, if the index declines, the borrower's interest rate goes down. The floating rate structure of the ARM allows lenders and borrowers to share the interest rate risk. In exchange for assuming some of this risk, borrowers generally receive lower initial interest rates. This economic reward for risk-sharing is the justification for ARM loans--at least in theory.

In practice, the one-way ARM, which is ubiquitous in the subprime market, only adjusts upwards from the initial rate. By the terms of the note the interest rate can never drop below the initial rate even if the index goes down. As a result, borrowers, not Wall Street, bear the brunt of any interest rate volatility.

Please buy this annuity. My daughter needs surgery.

Investment News, a trade newspaper for financial advisers, reports:

Some insurers are taking away their advisers' group health insurance and other employment benefits if proprietary-product quotas aren't met, advisers say.

..."For some advisers, health insurance is a bigger incentive than trips to Rio [de Janeiro, Brazil], extra commission income or plaques and trophies," [investment adviser Chris] Cooper said.

Harvard Law School bankruptcy expert Elizabeth Warren points to these numbers in this blog post at one of my new favorite wonk sites, CreditSlips.org. Here's Warren:

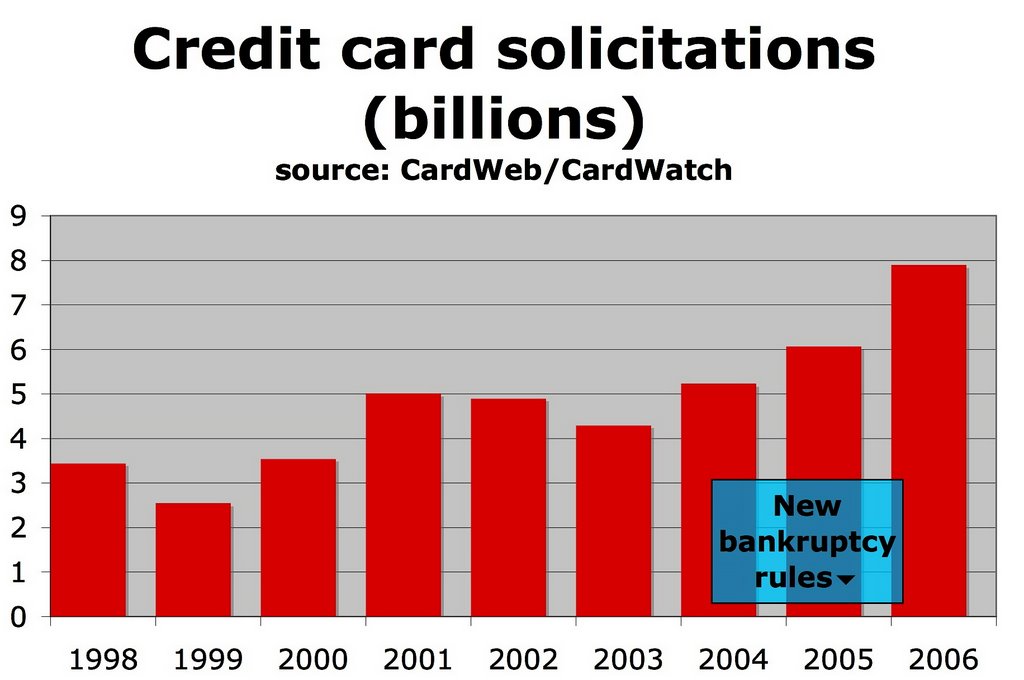

In 2005, Congress gave the credit industry what it wanted: tighter bankruptcy laws. In 2006, the credit industry responded by mailing out 8 billion credit card solicitations--up 30% from 2005. Larry Ausubel and others predicted during the debates over the bankruptcy laws that if Congress made it tougher to go bankrupt, then lenders would engage in riskier lending as they tried harder to get people to borrow.

What kinds of risks are the card companies willing to take on? With about 110 million households in the US, that's about 73 card offers per household. If the average card offers is about $5,000 in pre-approved credit, that about $365,000 in offers for every American household--or about $1000 a day, every day of the year....

If debtors have no bankruptcy option, Ronald Mann points out that creditors can keep them in the sweat box longer. Perhaps if bankruptcy were outlawed altogether the mailings would go to 16 billion, and if debtors' prisons were reinstituted, could the mailings top 25 billion? Ah, the possibilities.

By the way, you can call (888) 5-OPT-OUT if you want to stop getting these mailings. Click here for more info from the Privacy Rights Clearinghouse.

Senator (and Presdential hopeful) Chris Dodd is talking about it. After all, 2.2 million American households are at risk. Maybe more. But what would a bailout look like?

For a start, there's moral suasion. Before we considerany major government spending, lenders are going to have to take their licks. Here's Berkeley economist Brad DeLong, arguing that the problem here isn't simply that some homeowners got in over their heads. The whole system failed, and that means everyone with a stake in it has to pitch in to prevent a crisis:

I can see one constructive thing that bank regulators can do: they can publicly note [to lenders] that foreclosure is an appropriate response to individual cases in which payments are not being made because idiosyncratic things have gone wrong with individual household's finances, but that foreclosure is not an appropriate response to a systemic problem triggered by macroeconomic risks that have come calling. The appropriate response [for lenders] when it is an aggregate rather than an idiosyncratic shock is to renegotiate the loan--not to foreclose on a homeowner. And banks that do the second rather than the first are not fulfilling their responsibility to the system of which they are a part.

Don't provide direct financial support to homeowners in trouble, urges Nouriel Roubini of Roubini Global Economics:

Public funds to help borrowers should be used with care for several reasons. First, some forms of borrowers' financial support end up bailing out also the culprits of this mess; thus, these specific forms of support of homeowners under financial distress should be avoided. For example, direct subsidies to households who cannot afford their now-reset and excessively high mortgage payments end up helping the victims as well as the culprits.

By "culprits" Roubini means the lenders. Instead, he says, the feds should force the lender to renegotiate payments:

For example, suppose that the value of a home (with zero down-payment) has fallen 10% (following the current housing bust) and that the borrower cannot now pay the full value of the mortgage debt servicing payments that are now being reset at much higher interest rates. Then, if the borrower can afford a lower string of service payments that, in NPV [net present value, I think--P.R.] terms, is 10% lower than the initial terms of the mortgage (and equal to the true value of the home), the solution will be to allow a reduction of 10% (in NPV terms) of the debt-servicing payments for the borrower.

Hillary Clinton wants to make it easier for people to refinance out of onerous loans. From Bloomberg:

Clinton proposed eliminating pre-payment penalties that she said are "designed to trap borrowers" by imposing high fees for paying off loans ahead of time. Such penalties apply to 70 percent of subprime loans and less than 5 percent of prime loans, she said.

[Update 3/19:Here are Clinton's remarks. On reading it again, I see it's not clear if she's proposing to change the terms of current subbprime loans. Seems like not.] Washington Post columnist Steven Pearlstein suggests a new mission for Fannie and Freddie:

...what's needed is some mechanism to encourage the faceless investors who now hold those mortgages to accept less money than they were expecting, while at the same time helping homeowners to refinance their homes with more appropriate mortgages.

This, it seems to me, is a perfect assignment for Fannie Mae and Freddie Mac, which were chartered by the federal government with the express purpose of stepping in when private markets fail. They have the ability to raise and commit billions of dollars to the refinancing effort. They have active networks of lenders with necessary skills in financial counseling and loan workouts. And what better way for them to atone for their recent accounting sins and burnish their affordable-housing bona fides than to provide a market-based solution to this mess?

Even then, it won't be easy. Getting investors to forgo further interest payments and take 60 or 80 cents on the dollar they are owed may require some financial sweeteners. And to pay for those sweeteners, homeowners -- who, by the way, have some responsibility here -- would have to agree to share any profits they earn from selling or refinancing their homes in the future. Through the magic of securitization, Fannie and Freddie could turn that future stream of income into needed cash today.

[Update 3/19: It's worth underlining the point that the ideas discussed above don't require, as a first order of business, a direct government subsidy. But from the news story I linked to, it certainly sounds like Dodd is willing to have Congress stump up some cash.] Nicole Gelinas at the conservative City Journal makes the case for government just butting out:

If the government, or its proxy, now steps in and purchases those mortgages, or otherwise systematically bails out borrowers, it will create a hazard for the future. The next generation of mortgage lenders won't take the high risk of subprime home loans seriously, because they'll expect that, in the event of another crisis, the government will step in and bail them out again. So they'll be even more eager to approve the risky subprime mortgages that are getting so many borrowers into trouble in the first place.

And what about all those afflicted borrowers? It’s a harsh but unavoidable truth that many of them are in trouble now because they borrowed overpriced houses that were way beyond their means. If a family didn’t do the hard work of saving for a down payment and buying a house on which it could afford to pay a normal 30-year mortgage, it's unfair for the government to bail it out—and its lender. Remember who would subsidize that bailout through federal taxes: the family down the street that rented for a few years while it saved up money, or that bought a smaller, older house within its means.

By the way, my family is "the family down the street" that kept on renting rather than overstretching our finances to buy in a market we can't afford. So I sympathize with that last point. But this kind of cool tit-for-tat analysis seems a little unmoored from everyday experience. For the sake of argument, let's set aside the issue of whether lenders were deceitful or predatory, or whether the government encouraged this kind of behavior. I know I'm going to get lots of comments about 25-year-old idiots with $45,000 salaries buying McMansions and giant plasma screens and fancy cars that they couldn't afford. But I suspect that many people who are in trouble now were mostly trying to buy into a safe, stable neighborhood with good schools. The real-life choice for many families in bubble markets isn't between a fancy McMansion and a modest older home. It's between a house in a school district that works, and a house in one that doesn't.

Still, who could really argue that the government should prop up unrealistic home prices? Clearly, the air has to come out of some of these markets. The question is: How quickly? If mortgage blow-ups are really a dire threat to the overall economy, perhaps even those who were prudent all these years could grudgingly accept a carefully limited government intervention. Forced into a choice, I'd rather keep my job than satisfy my sense of cosmic justice.

A preview of the coming national health care debate

It used to be that political advertising was mostly limited to the election season. But lately, during the 11 o'clock news, New Yorkers have been treated to a back-and-forth ad battle between liberal Democratic Gov. Eliot Spitzer and a coalition of hospitals and the big healthcare-workers union. Spitzer wants to reduce state health spending, especially Medicare payments to hospitals; he also wants to expand Medicaid coverage for the uninsured. Here's a sample of the ads. First the ad from the union and hospitals:

The New York Post is reporting today that the hospitals group has pulled out of the campaign. Here's the ad from the governor:

So... scrappy, compassionate nurses, or angelic sick kids. Which do you like better?

We're going to see more of this kind of thing all across the country, and eventually it's going to become a feature of the national debate. Whether we end up with a system of universal care, or plod along with the current "private" system in which the government pays for 45% to 60% of spending, or do something market-based, this country is going to have to figure out a way to control health care costs. If we move towards more, rather than less, government involvement in health care--and that's my prediction--voters will have to make some choices.

Should we hold down the salaries of hard-working nurses? Squeeze the incomes of expensively trained and dedicated doctors? Put pressure on the profits of the drug companies that develop all these great new treatments? Shut down hospitals in vulnerable communities? Raise taxes on Joe Citizen? Provide only spartan care to the young, the poor, and the aged? Every potential loser will have a sympathetic case to make. And every one of them will buy an ad, except for the young and the poor. Insurance companies will have a tougher time getting anyone to feel sorry for them, but they'll eat up plenty of air time to call for preserving "choice."

This is one of the most challenging debates we can have in a democracy. I'm hopeful that it will move beyond dueling 30-second ads. But they'll be a factor.

(By the way, the Albany Times-Union has been doing a better job than most at clearing through the noise in the New York debate. Click here and here for more detail on what's at stake.)

Real estate can only fall 10% to 20%, right? Right?

You've probably read this before: Even when housing prices slump, they don't fall all that much, at least compared to stocks and other risky investments. I've passed on this bit of "wisdom" myself. And it it's not a totally ridiculous thing to say: Even in the big California bust of the mid-1990s, prices in the L.A.-Orange County metro area fell only 20% peak to trough in the region's worst five years. That's no Nasdaq. But, well, there's a bit more to it than that....

Below is a chart I made from data in a 2005 FDIC report. It shows the worst peak-to-trough five-year nominal performance for housing prices in several markets. Sorry--the labels are a bit hard to read. (Try clicking on the chart to open it in a new window.) The blue cities are in California, the green ones are in New England. In red, dropping by as much as 40%, are "oil patch" towns, which cracked in the late 1980s right along with oil prices.

It's easy enough to dismiss the evidence from the oil patch, if you want to. Prices there were forced down by an unusual, and very local, economic shock. The economies of L.A. and Boston are better diversified. Then again, if the oil boom-and-bust of the 1980s was an anomaly, what should we call the easy-credit-driven housing inflation of the early 2000s? Liar loans, interest-onlys, option ARMs, and aggressive subprime lending have changed the rules. History wouldn't seem to be a very reliable guide right now.

One reason real estate prices tend to be less volatile than stocks is what housing economist Karl Case calls "downward stickiness." When prices fall, many people just decide to stay in their houses rather than cut their price low enough to make an easy sale. But that also means there's a lot human pain behind a housing decline of "just" 10%. People get stuck in their houses, and that can change their lives. There's a good story in today's USA Today about workers who can't relocate to find better jobs:

Forty-six percent of companies say recruiting employees is becoming more difficult as the housing market turns tepid, according to a 2006 survey by Prudential Relocation.

Three in 10 of those who turned down a relocation did so because of housing and mortgage concerns, according to a 2006 survey by Atlas World Group. That decision can come at a price: More than half of companies had an employee decline a relocation, and 35% of employers say turning down a move hinders an employee's career.

It's been a startling change for companies that must move employees because of corporate growth or local talent shortages. At Petco's corporate headquarters in San Diego, job candidates today want to know about relocating. The company is also doing more to supplement temporary-housing costs for employees who are transferring.

The silver lining here, I guess, is that companies are complaining about real-estate job lock, and they're shelling out a little bit to help entice reluctant workers. That means the job market is still reasonably tight, which should help the economy. If it holds. If.

Update 3/15: For the record, the chart has been corrected since the initial post. (I added "5-year" to the label.)

Update 3/16: Lots of good points in the comments below about the true cost of real estate losses. They should be drilled into the head of every Realtor.

A few things worth expanding upon:

I only have data for nominal (that is, before inflation) losses on real estate. Losses after accounting for inflation are much, much more common: The FDIC report found that since 1978, some 142 metro areas have seen real losses of over 15% over a five year period. That's compared to just the 21 cities in the chart with 15% or greater nominal declines.

Even a nominal loss of 20% looks pretty small compared to nearly 60% (also nominal) for the Nasdaq in the five years after the crash. And while some houses in the LA market may have fallen more like 40%, some Nasdaq stocks went to zero.

The big difference, though, is that most people have a lot more in their house than they do in the Nasdaq. And most people aren't diversified in real estate, whereas that's very easy to do with stocks. Bottom line: It's difficult to make apples-to-apples comparisons of the returns on real estate to the returns on stocks. In real life--that is, in the lives of non-professionals with a limited ability to diversify and a primary goal of purchasing shelter--equities and housing are very different assets. Beware of people in the real-estate industry who use simple average-returns comparisons to convince you that a house is an easy money machine.

Finally, leverage adds to the risk of real estate. But don't forget about imputed rent. You have to live somewhere. The fact that some of your investment pays for a necessary consumption good dampens your risk exposure.

Pat I would like to see you bet your entire portfolio on the chance our positive economic cycle will be extended, especially in light of the recent economic indicators showing increasing downside risk. I remember a monstrous economy called Japan and their banking environment. You should review your notes and return to the boy scout motto; Better to have it and not need it, then need it and not have it. Best of luck. --Mark Anthony

All you've said is that experts are not likely to be correct, let alone always right. Fair enough. But where is the substantiated evidence and reasoning to prove they are talking gibberish? The predictions re housing troubles is only wrong in one major respect: timing. As usual, things take a little longer to pan out. But I've been reading about the expected problems with subprimes and housing decline for 3 years. It's analogous to naysayers against predictions of Dow at 36,000 and New Economy before the dot com bust. Eventually gravity prevails. --Tom Ngi

Pat Regnier must be hurt at his falling home price from this desperate attempt to spin this article. It is ALREADY happening, Pat... Wake up! --Andrew Johnson

For the record, I rent.

I am the sweet,chiming voice of reason:

Big Overreaction! They are confusing true Subprime with hybrid mortgage loans. True subprime has been holding the economy from a true recession.I have 24 years as owner of large mortgage firm. --Scott G.

Pat, As a longtime mortgage broker, 20 years, I read with interest - no pun intended - your story. Very good insight and humor! Tempest in a teapot. --Michael O'Connor

Good points Pat. What continues to amaze me are some of the predictions that point to complete economic catastrophe. Yesterday Bill Fleckentstein said there was about to be a credit freeze in housing. I disagree.There are certainly things to be concerned about, but a complete economic collapse is not one of them.--Nigel Swaby

Should I worry that all these guys are in the mortgage business? Hmmmm.....

Finally, Alexei Turchin of Moscow points me to a paper, "Cognitive biases potentially affecting judgment of global risks," by EliezerYudkowsky of something called the Singularity Institute for Artificial Intelligence in Palo Alto, Calif. SIAI is devoted to the development of artificial intelligence and to making sure that the thinking machines we create don't go all Matrix on us. That's right--this paper is, in part, about the risk of killer robots destroying the world! I know it sounds like I'm making fun here, but I'm not. It's a very thought-provoking little essay on how to think about risk.

Bear with me a moment: This really does have something to do with what I said Monday about the risk of subprimes bringing down the economy. Drawing on some of the same psychological literature that Philip Tetlock has, Yudkowsky lays out the basic mental errors people make when trying to predict uncertain outcomes. Then he offers this caution:

Every true idea which discomforts you will seem to match the pattern of at least one psychological error.

Robert Pirsig said: "The world's biggest fool can say the sun is shining, but that doesn't make it dark out." If you believe someone is guilty of a psychological error, then demonstrate your competence by first demolishing their consequential factual errors. If there are no factual errors, then what matters the psychology? The temptation of psychology is that, knowing a little psychology, we can meddle in arguments where we have no technical expertise-- instead sagely analyzing the psychology of the disputants.

...Despite all dangers and temptations, it is better to know about psychological biases than to not know. Otherwise we will walk directly into the whirling helicopter blades of life. But be very careful not to have too much fun accusing others of biases. That is the road that leads to becoming a sophisticated arguer--someone who, faced with any discomforting argument, finds at once a bias in it. The one whom you must watch above all is yourself.

Well said. And I felt slightly chastened as I read this. On Monday, I basically said that experts like NourielRoubini are giving us compelling new information and telling us very vivid tales that end in the economy crumbling, but that you shouldn't get too carried away by this because even experts are often blinded by their own great stories. Yudkowsky reminds me that this kind of argument can quickly degenerate into sophistical anti-intellectualism: "Don't listen to that guy. It sounds like he actually might know something."

I've been reading Roubini's blog for a while, and he clearly knows a whole lotta somethings. The counter-argument to Roubini's case is real, but sounds a bit blasé at the moment: Financial markets are mostly resilient, there's still lots of liquidity out there in world, unemployment is low, the Fed's on the case... After last week and the big market drop yesterday, Roubini's going to get a lot of credit for ringing the alarm bell on lender's insanely lax standards and the risk that posed not just to borrowers but to the whole financial system. He deserves that credit. Getting economic predictions right is to some extent a matter of luck and timing (a stopped watch and all that), but Roubini's work would have been valuable even if we weren't sitting here today wondering only how bad things are going to get. A year ago, most of the experts had convincing stories to tell about how everything would be okay. Investors and home-buyers alike needed to hear more about the risks that were building up in real estate, so that they could take steps to protect themselves. Your portfolio and your mortgage payment should never depend upon on best-case scenarios.

Now I risk descending from the sophistical to the banal: Anything could always happen. Duh. But for practical purposes, this is important to keep in mind during volatile, nervous periods like this one. Let's say you find the subprime-crash = recession argument compelling. (After yesterday, I'm 70% there myself.) What would you do about that now? You probably wouldn't be buying an investment property in San Diego. And you might be reluctant to stretch much to buy a bigger house. That's prudent. But would you sell your house ASAP? Dump most of the stock funds in your 401(k) and buy gold or cash equivalents? Bad ideas. I'm not an expert on asset-backed derivatives and how pricing problems might flow through to the wider market for credit. (The whole point about yesterday is that almost nobody understands this stuff very well, including the owners.) But I have spent my entire career covering people who make their living predicting market trends in hopes of investing ahead of them. I've seen the smart ones get it wrong, and not-so-smart ones get wildly lucky. The problem with market predictions isn't that people make factual or even psychological errors, but that markets are very, very complex. The pros struggle with this, and they have a lot more information and money to play with than we civilians do. I hope that a month ago your financial plan took account of the possibility of a housing-led recession; I hope that your financial plan today will work to your advantage if the market survives this bout of volatility. If you did it right, between then and now you shouldn't have had to change much.

Photo of Michael Smith's robot collection by Michael Smith

Kotlikoff is comparing the present value of all future government health benefits to the present value of all future gross domestic product. (Present value is what you would pay today in exchange for money at a future date.) Lots of caveats apply here: Projections like this are extremely sensitive to the guesses you make about future trends, as well as to the discount rate you use to come up with the present value figures. For these projections, Kotlikoff assumed health care benefit spending would grow at the rate it has since 1970 for the next four decades, and then grow on pace with per capita GDP thereafter.

So these numbers are really just a warning of what would happen if we stick to our present course. But what a warning. The other countries on this chart all have something approaching universal health care. But all Kotlikoff is measuring for the U.S. is projected spending on Medicaid and Medicare. "The U.S. is, under stated assumptions, on a course to spend close to one fifth of all future output (measured in the present) on two health care programs that, to repeat, cover only a minority of the population," writes Kotlikoff. That's right: We'll get all the cost and big government associated with universal care, only without the universal part.

Is this the subprime apocalypse? (Or is it just a scary story?)

In February, I posted here about Roubini Global Economics' prediction that defaults in subprime mortgages would ripple through the financial system and set off a recession. The next week, the stock market tanked, and lots people blamed subprimes. What's the link between subprimes and the rest of us? Here's how I summed it up last month:

[The] argument is pretty simple: Mortgage borrowers with the worst credit are defaulting, and the financial institutions that own these loans are taking a hit they didn't see coming. That's going to make them more cautious about lending money--and not just to subprime borrowers, but even to those of us with sparkling credit scores. What's more, Roubini observes, even many prime borrowers are low on savings and haven't had a serious raise for a while. And falling real estate values have taken some of the air out of their home equity.

Stir this witches brew together long enough and you get a very unhappy consumer. We're about due for an economic slowdown as it is. Roubini thinks the credit crunch might turn that slowdown into a "hard landing."

Actually, I oversimplified things a little bit here. You might, while reading this, picture in your head a single bank that has given out some loans to prime borrowers, and some other loans to subprime borrowers. When the subprime borrowers start missing payments, a nervous bank president looks at his balance sheet and calls the head loan officer and tells him to tighten up lending requirements across the board. While that's not a bad way to think about it, in reality we're not talking about individual banks but an entire financial system. Banks sell their mortgages, which get bundled into trade-able securities, which in turn become the raw material for all manner of fancy financial derivatives. This stuff ends up on the books of mutual funds, hedge funds, insurance companies, pension funds, etc. (Yes, I'm oversimplifying here, too.) Yesterday in the New York Times, Gretchen Morgenson painted a vivid, rather scary picture of this market, strongly suggesting that it's set to go pop! in our faces any day now. Felix Salmon raises some questions about the Times analysis here.

So what's going to happen? I dunno. But when I'm weighing the likelihood of a prediction coming true--or worse, making a prediction myself--I try to remember some of what I've learned from psychologist Philip Tetlock. He's made a study of expert predictions, and he's found that they really aren't very good. They do about as well, he says, as "the moderately attentive reader of good newspapers."

That doesn't mean you shouldn't listen to experts like Roubini; you just shouldn't overvalue them. But what's even more interesting about Tetlock's work is why experts make mistakes. One problem experts tend to have is loquacious overconfidence: They have a lot of information, so they can put together very convincing stories to describe extreme outcomes. Tetlock also found that experts were more likely to predict extreme events if they were forced to imagine specific story-lines. For example, they were more likely to predict the disintegration of Canada if they were asked to put odds on a set of scenarios--such as an economic downturn, combined with political victories for Quebec separatists--than they were if they were just asked about the chances Canada breaking up. Imagination is powerful.

I'm no expert. But three weeks ago, if you had asked me whether subprimemortages were a threat to the economy I would have shrugged and said, "Ehhhh.... probably not." Statistically, that's a fairly safe response. The status quo has a way of staying that way, give or take. But in the past few weeks I've been reading Roubini, Morgenson and Salmon, and blogs like Calculated Risk. I'm talking about this stuff at the office, and I'm following the anxious comments on the subject on this blog. I'm learning all about CDOs, HELs, AltAs and the ABX. (Three weeks ago, if Alex Trebek had asked me what those were, I'd have answered, "What are the worst fraternities in Urbana-Champaign?") I have lots of information now. Suddenly, the possibility of a housing credit crunch that breaks the economy is much more vivid to me. That doesn't necessarily mean it is any more likely.

Update 3/14: See my new post for more on our credit-cruch conversation.

When I bring up taxes on this blog, inevitably the conversation in the comments turns to the "FairTax." It's simple! Just replace today's complex, costly system with a national retail sales tax. Says Jan in Atlanta:

Easy solution to it all: implement the Fair Tax (www.fairtax.org). This incredibly well-studied system of taxation would eliminate the AMT, eliminate the IRS and all the costs associated with tax collection, and implement a consumption tax instead of an income tax, so each individual can control his taxation amount by controlling how much he spends. This way people would no longer get punished by excessive taxation for providing value to society.

The FairTax has a surprisingly strong base of activist supporters. They get a lot right: The current tax code really is a mess, and taxing consumption instead of just income could solve a lot of problems. But I seriously doubt the FairTax--or rather, the version of a sales tax that could actually get passed--would work nearly as smoothly as its supporters think. I wrote this in 2005:

Many mainstream economists and tax experts like the idea of some kind of consumption tax -- in fact, the superiority of consumption taxes is almost conventional wisdom these days.

But many of the same people point to serious problems with the FairTax plan. (A sales tax is just one way to levy a consumption tax. Competing plans include the European-style value-added tax, or VAT, as well as variations on the flat tax Steve Forbes made famous.)

Critics claim the FairTax has two major flaws: It wouldn't work in practice and, even if it did, it wouldn't raise enough money. The first problem has to do with the fact that people cheat on their taxes; they do it now, and they'd find ways to do it under a sales tax. With all of the taxes we'd owe being lumped into one big sales tax, lots of people might be tempted to try evading it, with black markets springing up everywhere.

Joel Slemrod of the University of Michigan's Office of Tax Policy Research says that only six countries in the world have tried to collect a sales tax north of 10 percent, and four of them eventually adopted alternatives like a VAT. Consumers might also be unpleasantly surprised by all the things that get taxed: Not just milk at the grocery store, but legal fees, rent on an apartment, even health-care expenses.

[Congressman and FairTax sponsor John] Linder [R-Ga.] says the administrative problems with a sales tax have been over-blown. Really, he asks, is your local big box store going to help you cheat on your taxes? And the FairTax frees millions from filing tax returns and gets the hated IRS out of their lives.

"I want a system that doesn't have an agency that knows more about you than you are willing to tell your own family," says Linder. This is crucial. FairTaxers seem to care as much, if not more, about getting rid of the IRS as they do about the economic and budgetary impact of reform....

A knottier problem is what the rate would have to be.

The FairTax bill pegs it at 23 percent in order to fund the government at current levels without raising the deficit. (If you think of the FairTax like a state or local sales tax, you'd say that this is a markup of 30 percent on prices at the store. See the chart above.) But economist William Gale of the Brookings Institution says that this number is way, way too low. "They're telling kind of a big lie about tax reform," he says.

Gale calculates that a 23 percent rate would blow a $7 trillion hole in the budget over 10 years, and that a more realistic rate is 31 percent, and higher still if you allow for evasion. And if lobbyists convince lawmakers to exempt things like health care or other necessities--a real possibility, given the culture of Washington--the gap looks even bigger.

FairTaxers respond that Gale isn't taking into account the huge economic growth they believe would occur once the tax system started encouraging investment. And besides, they add, whatever rate you'd pay is comparable to what you now pay. Counting Social Security and payroll taxes, your marginal rate may be north of 30 percent. "To talk about [sales tax rates] independent of what we're currently facing is slightly unprofessional," says Boston University economist and FairTax supporter Laurence Kotlikoff, speaking of Gale.

Kotlikoff has recently written a paper claiming that Gale was wrong and 23% really is the right figure. This is based on a complex set of calculations and data crunching, and I'm not going to try and guess who's right. But in a recent AEI debate, Gale argued that even if Kotlikoff's baseline number is right, it's still based on some optimistic assumptions about tax evasion and ignores legislative erosion--that is, the tendency of legislators to create more and more exceptions and loopholes. Kotlikoff and Gale are both good economists, but I think Gale is especially persuasive in his judgement of how Washington works.

I dropped by the New School University this morning to see a panel discussion on the state of the U.S. economy. The line-up included Nobel Prize winning economist Robert Solow, CNBC'sLarry Kudlow, economist and superbloggerBrad DeLong, and Robert Hormats of Goldman Sachs. Former Nebraska Senator Bob Kerrey, the president of the New School, moderated. The general view from the panel was that the economy is in fairly decent shape, but that during the Bush administration we've squandered an opportunity to invest for the future and to improve our fiscal health. I'm guessing "Goldilocks"Kudlow doesn't sign on to the second half of that formulation, but I came in near the end of his opening remarks and he left before the discussion really opened up. That's a shame--it might have been a fun debate to watch.

In any case, I picked up some interesting insights:

Consumption taxes are coming. That's the forecast, at least, of panelist Robert Shapiro, a former undersecretary of Commerce during the Clinton administration. He thinks we're likely to see two additional federal taxes imposed in the next 20 years. First, a carbon tax to address global warming. Second, a "value added" tax just to pay for Medicare. "Under anything like the current political constraints, we will have to find enormous new resources to pay for Medicare," he said. "And that's how you get to a VAT."

A VAT is similar to a sales tax, except that the money is collected from all the businesses involved in making and distributing a good. (To a consumer, it can still look exactly like sales tax, depending on the design.) According to Taxing Ourselves by Joel Slemrod and Jon Bakija, almost every other industrialized nation uses a VAT.

Shapiro's prediction for a Medicare VAT sounds pretty plausible. Of maybe it will be a bigger, broader Health Care VAT. As another panelist, Julie Kosterlitz of the National Journal, observed, polls suggest that most Americans would be willing to pay higher taxes in exchange for universal health coverage. And Kerrey, the long-time politician, said that the public is usually more accepting of taxes that are earmarked for a specific purpose.

As I pointed out in an earlier post, if future tax hikes come in the form of consumption taxes, you'll pay them even if you stashed your savings in a Roth account. Maybe that's another reason for lawmakers to like them.

Yes, China could be a problem. China has been lending us lots and lots of money, which in turn has made it easier for us to buy all their t-shirts, blenders and televisions. They do this even though our dollar is clearly overvalued; as its value falls, so will China's return on its loans to us. Most observers think that won't be a problem--the imbalance will unwind slowly as China's economy matures. You'll also hear that a falling dollar really isn't so bad, since it would boost the overseas demand for goods manufactured here. (We do still do that.)

But DeLong pointed out that what matters here is velocity. What if China really isn't okay with lousy returns on its dollar-denominated assets? And what if it realizes this, as DeLong vividly put it, "in the middle of the night," in a panic? A fast decline in the dollar would still boost foreign demand for the stuff we make, but to benefit we'd have to shift a whole lot of our workforce out of the service and construction sectors (which would be hurting) and back into manufacturing. Just how quickly can we retrain interior decorators and Home Depot managers and turn them into auto workers?

DeLong said he isn't betting on such a catastrophe. He was suggesting that we need some "fire insurance," just in case. Since I don't think State Farm wants to write the entire U.S. economy a policy, the only "insurance" would be to get the budget in better shape. DeLong's analysis poses a bit of a problem for liberals. (DeLong worked in the Clinton administration.) People like Paul Krugman and James Galbraith are arguing that Democrats should lose their obsession with balanced budgets, so that they can get big things done if they win all the marbles in 2008. And it's true that deficits aren't always so terrible. But this would have been an easier case to make in 2000. As it stands today, deficit spending for health care, education or the rest of the Democrats' wish list will have be piled on top of the deficits generated by what DeLong calls Bush's "three big projects:" tax cuts, the war, and Medicare Part D.

Why you can't afford New York real estate, part 2. Bob Kerrey said that on the island of Manhattan, 16% percent of the population works in finance or insurance, but that those people earn 65% of the borough's income. I'm not sure where he's getting those numbers, but they certainly sound about right.

One common response to concerns about rising inequality is to say that it's just a side-effect of our incredible system of higher education. The economic return for going to college or graduate school is very high--and who would really want it to be otherwise? Well, New York has no shortage of educated people. You can't swing a cat on 14th Street without hitting five or six people with advanced degrees. But a Ph.D. and six bucks will just about buy you a Metrocard in this town. Teachers, nurses and scientists--productive people with lots of training--are barely hanging on here. It's important to reward people who invest in their brains, but is it just maybe possible we're rewarding the narrow slice of smart people who invest in MBAs a little too much?

Hey, Patriot-News of Harrisburg, PA, it's supposed to be blogs that raid newspapers for material! (See last post.) Not that I'm complaining.

EDITORIALS ANGRY FOLKS: Day of reckoning on its way with stratospheric tax hikes

There are some truly mean-spirited people on the Internet. Take this from James in Monument, Colo.:

"Let me offer my personal thanks to the worst generation (the baby boomers). You have [mismanaged] this country royally and we, your children, would like to tell you what to do with yourselves. Thanks for all the debt and irresponsibility. I hope your nursing homes treat you like crap."

What did Mom and Dad do to this guy? Spend his inheritance?

Well, yes, in a manner of speaking.

James in Monument was responding to Money senior editor Pat Regnier, writing on the "Generation Risk" blog (which can be found at www.cnnmoney.com). Regnier was offered this interesting bit of advice by Robert Gordon of Twenty-First Securities in New York City: "Draw a chart of tax rates -- if that was a stock, you'd buy it now."

In other words, taxes are headed for the stratosphere.

Click here for the rest of the editorial. You might even be quoted in it.

At yesterday's House hearing on the alternative minimum tax, Republicans blamed Bill Clinton for the ever-expanding reach of the AMT. (More on that here.) I suspect they were channeling this Wall Street Journaleditorial:

Remember the 1993 tax hike that was supposed to fall only on the rich? In addition to raising gas taxes and Medicare payroll taxes and income tax rates, the Democratic Congress that year also raised the AMT: from a 24% flat rate to a dual tax rate of 26% on AMT income up to $175,000 and 28% on AMT income above that amount.

It's true that the 1993 bill slightly increased the AMT's family income exemption, but Democrats refused to index those exemptions for inflation. So the combination of the higher rates and the failure to index for inflation has caught more and more middle-class taxpayers in the AMT's maw. From 1992 to 2002, this Clinton stealth tax hike increased sixfold the number of filers paying the AMT, to nearly two million from 300,000.

A Joint Tax Committee (JTC) analysis requested last year by Senator Charles Grassley of Iowa shows that about 11 million more Americans will have to pay the AMT next year thanks to the higher post-1993 AMT rates.

Here's a response to that argument from Wayne State University tax law prof Linda Beale, who blogs at ataxingmatter.blogs.com. (The emphasis is hers.)

The Journal blames Clinton for the AMT because the Clinton administration did the sensible thing--when top rates were raised, the AMT rates were raised as well so that the AMT could continue to function parallel to the regular system the way it was intended to. (Clinton also increased the AMT exemption--permanently, unlike the Bush Congress.) If the Bush administration had applied the same logic that the Clinton administration applied, it would have lowered the AMT rates (and again increased the exemption permanently, because of inflation) when it lowered the regular tax rates, so that the AMT would have continued to function parallel to the regular system in the way it was intended to.

A House Ways and Means subcommittee held hearings on the fixing the alternative minimum tax this afternoon. My colleague Jeanne Sahadi wrote a clear and concise guide to the options lawmakers have in dealing with the AMT mess, which you can read here.

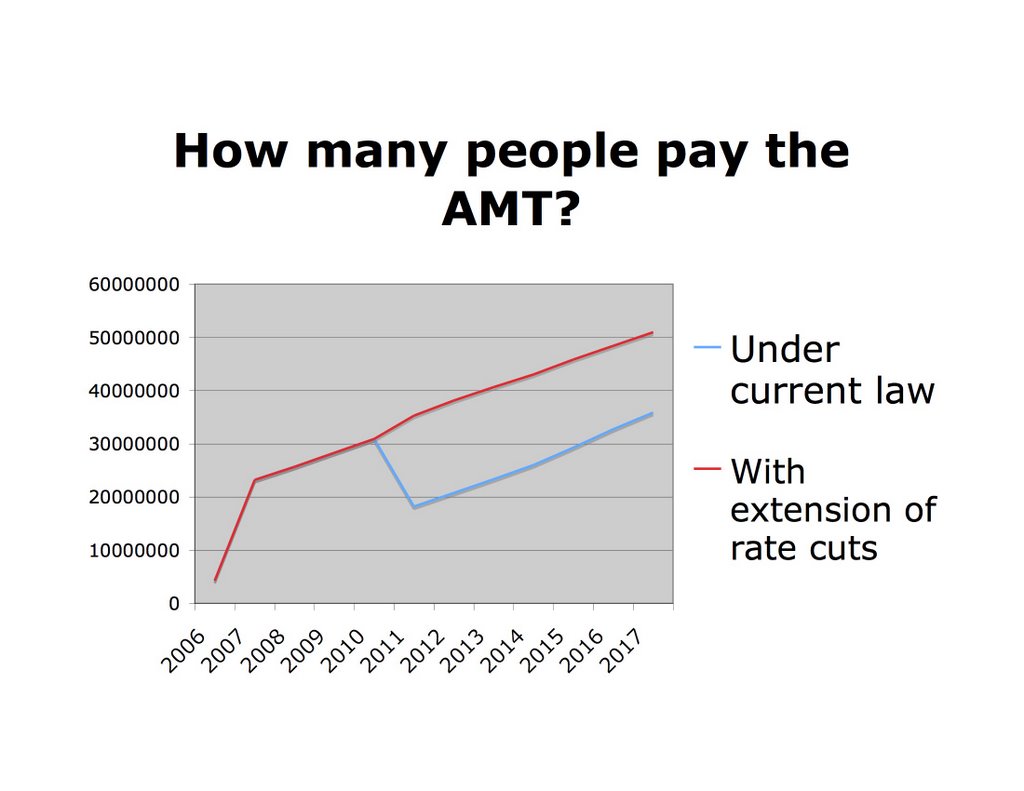

Check out this chart, which is based on data from the Joint Committee on Taxation. The blue line is how many people will be snagged by the AMT under current law. The red line is how many people will have to pay it if the 2001 rate reductions are renewed. (They are set to "sunset" in 2011.) Extending the tax cuts will dramatically increase the number of people who will have to deal with two separate tax systems, even as fewer and fewer people enjoy the benefits of the cuts. That's because without those tax cuts, more people would have a high enough tax under the regular system that they wouldn't be moved into the AMT. One thing to be clear about: This chart does not mean that the Bush tax cuts will actually raise the taxes of those who end up on the AMT. As Alan Viard of the American Enterprise Institute explains in his Ways and Means testimony today:

Suppose that, without [the recent tax laws], a hypothetical taxpayer would have a $100 tax liability under regular tax rules and a $90 tax liability under AMT rules. The taxpayer would then be on the regular income tax and would have a $100 tax liability. Suppose that those laws reduce the taxpayer’s liability under regular tax rules to $85 while leaving his or her liability under AMT rules unchanged at $90. Because liability under the AMT rules is now higher than the liability under the regular tax rules, the taxpayer moves onto the AMT and has a $90 tax liability.

Although these laws cause the taxpayer to move onto the AMT, they do not raise his or her tax liability, relative to prior law. On the contrary, the laws reduce the taxpayer’s liability from $100 to $90. Moving onto the AMT merely reduces the size of the tax cut, which would have been $15 without the AMT, to $10. In colloquial terms, the AMT “takes back” one-third of this taxpayer’s tax cut.

Even so, the AMT clearly erodes the constituency for extending the tax cuts. Not to mention driving people crazy.

Update 3/8: Want to pin the AMT mess on the Republicans? Or maybe on the Democrats? Check out my post, "Alternative minimum blame."

We journalists love giving names to generations.* It's a bad habit, but hard to resist once you get started. Just yesterday, I pronounced my children members of Generation Won't-Use-The-Potty. I think I've identified a powerful demographic trend among the 2-and-under set--I could give you more than three examples--but I'm hoping it's not a durable one.

The international edition of Newsweek has a story on "The Lost Youth of Europe." (Hat tip to the highly useful Informed Reader.) According to the article, the kids of baby boomers are locked out of good jobs and can't afford decent homes. We also learn that Europeans, too, have a flair for demographic shorthand. In France, 20- and 30-somethings are known as "GénérationPrécaire," or the Precarious Generation. In the UK, they're the Boomerang Generation, Maggie's Children (that's as in Thatcher), and (ugh) IPODs--insecure, pressured, over-taxed and debt-ridden. In Germany, it's Generation Intern, because so many young folks can't snag permanent gigs.

Anything we can learn from this? You could use it as an argument against expanding the social safety net here--the Newsweek story says that "the same labor rules that protect the jobs of the middle-aged shut out the young [and] dwindling birthrates mean there will soon be fewer workers to support the retirees." But the U.S. is a long way from looking like France, and we'd still have one of the most flexible economies in the developed world if we adopted universal health care and, say, wage insurance.

The European experience does show that there's a downside to booming housing markets. (I mean besides the occasional crashes.) Says Newsweek:

Across the continent, spiraling property prices and poor job prospects are conspiring to keep youngsters living at home. According to the Italian Institute of Social Medicine, 45 percent of the country's 30- to 34-year-olds still sleep in their old beds and enjoy Mama's home cooking. In France, the proportion of 24-year-olds now living with their parents has almost doubled since 1975, to 65 percent. Even in the U.K., with its enviable record of job creation, the average age of the first-time home buyer has climbed from 26 in 1976 to 34 today. Property prices are now eight times higher than the median earnings of the ordinary twentysomething.

I lived in the U.K. for a couple of years, and even to an expatriate New Yorker the real estate market seemed insane. (Back in the five boroughs, we have not yet felt the need to come up with a slang term equivalent to the British "gazump"--meaning to accept a bid on your house and then renege upon receiving a better offer. As in, "I thought I had that flat in Rising Damp Mews, but I was gazumped.") So I was interested to read the work of economist Andrew Oswald of the University of Warwick, who contends that encouraging more and more home-ownership can be counterproductive. Oswald writes:

High home-ownership levels block young workers' ability to enter an area to find a job: if we look at countries like Spain, with its 80% home ownership rate, a key part of the problem is young jobless people living at home, unable to move out because the rental sector hardly exists any more. Here the difficulty is not that unemployed people are home owners; it is that unemployed men and women cannot move to the appropriate areas.

Inefficiencies caused by high home-ownership rates impair the creation of jobs in more subtle ways.

In an economy in which people are immobile, workers do jobs for which they are not ideally suited.... The resulting inefficiency is harmful: it raises the costs of production and lowers real incomes.

On the other hand, of course, home-ownership has given middle-class people a chance to build a nest-egg over time, and probably encourages more stable communities. But it's always possible to have too much of a good thing--whether you're talking about the European Dream of job security and income stability or the American Dream of owning a home.

*Note: Obviously, this isn't the post on the Medicare funding gap I foolishly promised in my last post. That's still in the works.

60 Minutes ran a Steve Kroft report last night about David Walker, the comptroller general of the United States. Basically, he's our accountant. Walker has been traveling the country warning that we're headed for a fiscal meltdown.

In response, economist Dean Baker, blogging for the liberal journal AmericanProspect, unleashes his fists of fury:

60 Minutes declared war tonight on Social Security and Medicare.... [I]f they wanted to be accurate, the 60 Minutes crew could have pointed out that almost the whole horror story is driven by projections of exploding health care costs, not "entitlements" for the elderly (e.g. Social Security). As is clear to anyone who is moderately competent at arithmetic, the projected budget problems are due to a projected explosion in health care costs, not demographics. If U.S. health care costs were more in line with those in any other wealthy country, there wouldn't be much of a budget crisis to talk about.

I missed the show tonight, but if the web version of the story is any reflection of what viewers saw, the 60 Minutes crew actually does say that health care is the 800 lbs. gorilla here:

Part of the problem, Walker acknowledges, is that there won't be enough wage earners to support the benefits of the baby boomers. "But the real problem, Steve, is health care costs. Our health care problem is much more significant than Social Security," he says.

Asked what he means by that, Walker tells Kroft, "By that I mean that the Medicare problem is five times greater than the Social Security problem."

The problem with Medicare, Walker says, is people keep living longer, and medical costs keep rising at twice the rate of inflation....

So Baker and Walker agree, I think, that the way we pay for health care is basically ridiculous and that we can't afford to sustain our current spending patterns.

The question is, what do we call this problem? Is this a fiscal crisis? Or a health care crisis? This sounds like an abstruse philosophical debate, but it has enormous political and practical implications.

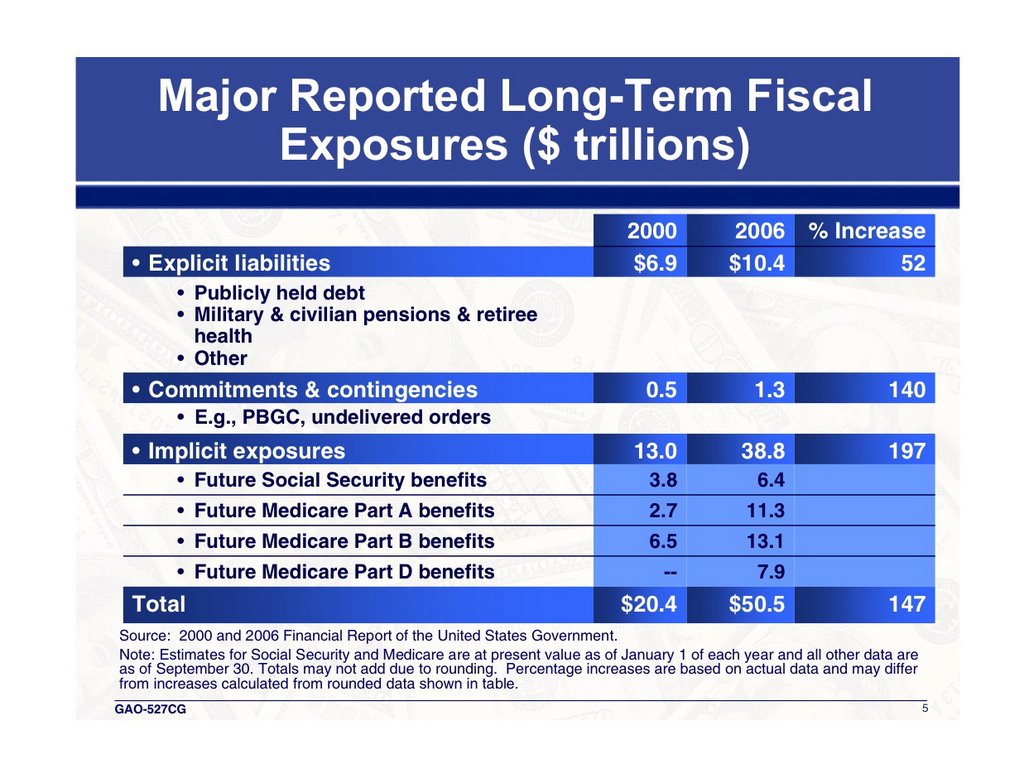

If you add the projected cost of future Medicare benefits to the basic federal debt and other obligations, you get some mind-bogglingly big numbers--in the neighborhood of $50 trillion. (See the slide from one of Walker's talks at left.) That's one way to ring the alarm bell, I suppose. Maybe all this bankruptcy talk will eventually get voters and policymakers focused on fixing the health care system, so that those projections don't come true.

But talking about this primarily as an accounting problem--too much going out, not enough coming in--can confuse as much as it clarifies. The government could, in theory, solve most of its balance sheet woes by simply phasing out the Medicare program. But this country would still have a health-care financing mess. That's Baker's point.

So should we just call it a health care crisis? More on that in my next a coming post....

I hesitate to open this particular can of worms, but there was a debate over the "FairTax" at the American Enterprise Institute this week. You national sales tax geeks out there--you know who you are, and I love ya!--can listen to it here.

But this post isn't about the "FairTax". It's about something interesting William Gale, an economist at Brookings Institution, pointed out during the debate:

We had an episode earlier in this decade where the government cut taxes, and one of the arguments was that this was going to force Congress to cut spending. Exactly the opposite happened. Spending skyrocketed. Historically, that has been the pattern. When we cut taxes spending goes up, and when we raise taxes we cut spending and impose fiscal discipline on both sides of the budget. That's what happened in the 1990s.

So what's up with that? Why hasn't "starving the beast" worked? William Niskanen of the libertarian Cato Institute has suggested a possible explanation: Cutting taxes makes government cheaper--for now, anyway--and people usually want more of something when it gets cheaper.

In other news: The folks at the Wall Street Journaleditorial page really should debunk this.

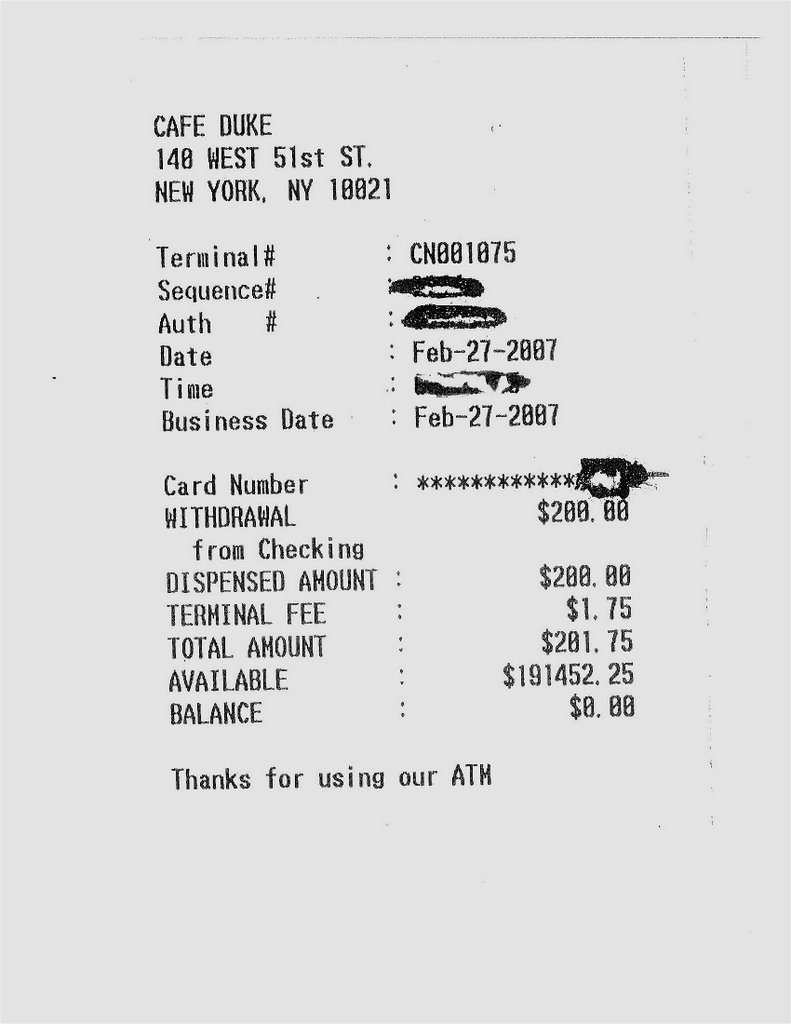

Maybe it's because you'd be bidding against this guy.

To whoever left this at the Cafe Duke ATM: You won't be keeping that money for long if you keep paying those $1.75 terminal fees. You know your bank charges you an extra dollar on top of that, right?

(Thanks to my colleague Sam Grobart for stumbling on this and donating it to Generation Risk.)

Or feel free to send a letter to the editor about this story.

CNNMoney.com Comment Policy: CNNMoney.com encourages you to add a comment to this discussion. You may not post any unlawful, threatening, libelous, defamatory, obscene, pornographic or other material that would violate the law. Please note that CNNMoney.com makes reasonable efforts to review all comments prior to posting and CNNMoney.com may edit comments for clarity or to keep out questionable or off-topic material. All comments should be relevant to the post and remain respectful of other authors and commenters. By submitting your comment, you hereby give CNNMoney.com the right, but not the obligation, to post, air, edit, exhibit, telecast, cablecast, webcast, re-use, publish, reproduce, use, license, print, distribute or otherwise use your comment(s) and accompanying personal identifying information via all forms of media now known or hereafter devised, worldwide, in perpetuity. CNNMoney.com Privacy Statement.