Bailout plan under fire

Paulson, Bernanke urge immediate action on $700B plan - cite fear of meltdown. But senators from both sides voice more questions than support.

NEW YORK (CNNMoney.com) -- The debate over whether Washington should enact an extraordinary bailout of the nation's financial system reached a fever pitch at a Senate hearing on Tuesday.

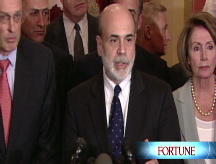

Treasury Secretary Henry Paulson and Federal Reserve Chairman Ben Bernanke said Congress needs to act swiftly to preserve the health of the U.S. economy and stem a widening crisis that started with housing and has spread to other areas.

But the two faced strong criticism from both Democrats and Republicans on the Senate Banking Committee. The pair spent almost as much time conceding problems with the plan as they did championing it as the solution to the nation's current financial problems.

"You know, I share the outrage that people have," said Paulson. "It's embarrassing to look at this, and I think it's embarrassing to the United States of America."

Paulson is asking that Congress pass a law giving Treasury broad powers to buy as much as $700 billion in troubled assets - primarily mortgage-backed securities that have seen their value plunge due to rising foreclosures and a prolonged slide in home values.

The program, which Paulson and Bernanke first unveiled five days ago, would amount to the most sweeping economic intervention by the government since the Great Depression.

Lawmakers have criticized the Bush administration for asking for a "blank check." On Tuesday, Paulson and Bernanke argued that too many restrictions on the program would limit its effectiveness at a critical time.

"The financial markets are in quite fragile condition and without action they will surely get worse," Bernanke said. "This will be a major drag on the U.S. economy and be a major drag on the ability of the economy to recover."

While expressing concern about the economy, senators voiced wide-ranging doubts about the plan.

Sen. Richard Shelby of Alabama, the top Republican on the committee, said the government's previous efforts to save mortgage finance giants Fannie Mae and Freddie Mac, as well as its role in keeping Bear Stearns out of bankruptcy last spring, show the limitations on attempts to fix markets.

"You can't assure us this will work because you thought the other plans would work," Shelby said.

Paulson said he believes the new plan will address the root cause of the crisis because it attacks the credit crunch that has followed the collapse of the market for mortgage-backed assets held by banks and Wall Street firms.

"I share in your frustration," Paulson said. "This is not something I ever wanted to ask for. But it's much better than the alternative."

Some senators condemned the proposal as a bad idea, while others said they worried about taking fast action on such a momentous program.

Sen. Jim Bunning, a conservative Republican from Kentucky and a long-time Federal Reserve critic, said that he could not support the proposal.

"It will not help struggling homeowners pay their mortgages. It will not bring a halt to the slide in home prices," Bunning said. "This massive bailout is not a solution. It's financial socialism and it's un-American."

Sen. Sherrod Brown, a liberal Democrat from Ohio, said calls from his constituents about the plan have been universally negative. He told the story of one constituent who drove to Washington.

"He quite rightly asked why we were rushing to bailout companies whose leaders got rich gambling with other people's money," Brown said.

Brown asked if Wall Street owed the rest of America an apology. Paulson, who served as CEO of Wall Street firm Goldman Sachs for seven years before becoming Treasury Secretary in 2006, pointed at both Wall Street and others for the nation's current crisis.

"There is a lot of blame to go around," Paulson said. "A lot of blame [belongs] with big financial institutions that engaged in this irresponsible lending."

But Paulson also said some blame rests with regulators, rating agencies and others - "people who made loans they shouldn't have made, people who took out loans they shouldn't have taken out."

Even senators who said they believed that they must push legislation forward expressed misgivings with at least some aspects of the broad powers the Treasury was seeking.

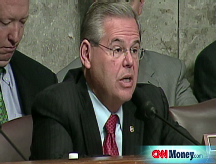

Sen. Christopher Dodd, D-Conn., who chaired Tuesday's hearing, praised Paulson and Bernanke and said quick action is needed but added that time must be taken to ensure the bailout struck the proper balance between Wall Street and taxpayers.

"There is no second act to this," Dodd said. "It is critically important that we get this right."

After the hearing, Dodd told reporters that the Treasury plan was "not acceptable," according to the Associated Press.

Paulson said he put forward a brief, three-page proposal without details about how the program would be overseen for a reason. He said he felt it was proper to work with Congress on such details.

"I want it, we all want it," he said about oversight.

Lawmakers were also concerned about the program's risk to taxpayers.

Bernanke stressed that most or even all of what the government spends to buy the assets would be recovered when the assets are eventually sold.

Senators pushed the witnesses about whether the government should get equity in the firms it helps.

Bernanke and Paulson both argued that such a provision would limit the firms that would participate and undermine the effort.

"If we keep the range of participants too narrow, only failing institutions, for example, then we won't have a robust, competitive auction," said Bernanke. "The more participants we have, the more people who are involved in offering these assets, (then) we'll have a competition."

Paulson echoed Bernanke in calling for the fewest restrictions possible.

But Dodd vowed that lawmakers will add a provision reining in the pay of executives at firms being bailed out. "Count on it," he said.

Drafts of counter proposals have emerged from both chambers. The Senate effort is led by Dodd. The lead negotiator in the House is Barney Frank, D-Mass., chairman of the Financial Services Committee.

The situation is fluid as Congress presses to craft a bill that addresses concerns from members of both parties. The key add-ons being debated are:

- Give the government an equity stake in the companies it helps

- Change the bankruptcy law so that judges can modify the mortgages of filers' primary residence

- Curb executive compensation on the companies participating in the bailout

- Impose oversight of the Treasury program

- Require the government to promote sustainable homeownership through loan modifications and use of the new HOPE for Homeowners Program on the mortgages underlying the assets it buys in the bailout.

The markets have been on high alert in recent days as investors await the outcome of the debate in Washington. U.S. stocks had a major sell-off Monday and another dismal showing on Tuesday, with the Dow Jones industrial average losing 373 points and 161 points in back-to-back sessions.

On Tuesday, Paulson conceded that there are still more questions about the program than answers. But he said he's convinced that it's the best course for the economy.

"You've not heard me say there's not risk to the taxpayer. You've heard me say there's less risk to the taxpayer with this course," Paulson said. "What the cost to the taxpayers will ultimately be will depend upon how the economy recovers, what happens in the housing market and how we execute this program." ![]()