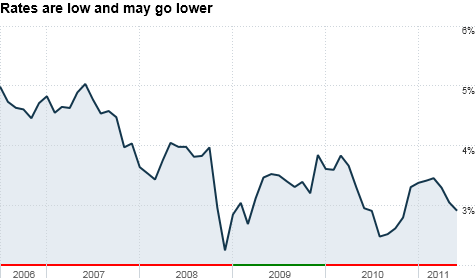

The 10 Year Treasury yield has a way to go before it hits crisis levels. But if the economy weakens more, some think 2% is not out of the question. Click chart for more on bonds.

NEW YORK (CNNMoney) -- Ben Bernanke might as well have worn bell-bottom pants at Wednesday's press conference.

The Fed chairman gave a dour outlook for the economy as the central bank lowered its growth forecasts and also raised its outlook for core inflation.

That may sound an awful lot like the stagflation nightmare of the 1970s. But the bond market is clearly focusing more on the "stag" and less on the "flation."

The yield on the 10 Year Treasury fell to about 2.9% Thursday. To put that in context, the yield was as high as 3.75% as recently as February.

But that was before the Japan earthquake, renewed fears about the European debt crisis and a slowdown in hiring in the U.S. It's no wonder then that economists, investors and consumers are now all acting like negative Nancies.

It's likely to get worse. Long-term rates may continue to fall since, in what may first seem counterintuitive, investors rush to buy Treasuries at times of economic weakness. (Rates and prices move in opposite directions.)

The conventional wisdom is that no matter how bad the economy may seem in the U.S., government-backed debt is still viewed as relatively safe. That's especially true now when you look at the debt situation in Greece.

So long-term bond yields don't usually trend higher until the Fed is willing to start raising interest rates. And that ain't happening anytime soon.

"As long as economic weakness remains and people are worried about risk in Greece, the Fed will be on hold indefinitely," said Michael Collins, senior investment officer for Prudential Fixed Income in Newark, N.J. 'It can't contemplate raising rates until there is a dramatic turnaround in the economy."

That turnaround doesn't seem to be in the cards. The latest weekly jobless claims numbers were ugly. New home sales are falling again.

And even though crude oil prices and gasoline prices have tumbled in recent weeks, the Department of Energy still decided to try and push prices lower by announcing Thursday it would release oil from the Strategic Petroleum Reserve.

To me, the decision is a clear sign of panic about the state of the economy. (Read why I thought tapping the SPR was a bad idea back in March.) And that's being reflected in both plunging stock prices and lower bond yields Thursday.

Add all that up and it means the Fed may not need to buy even more Treasuries, a so-called third-round of quantitative easing, to keep interest rates low. The bond market is doing the Fed's job for it.

"It is interesting. People were expecting higher rates after QE2. But it's just been a one-way trade lately with bond yields still going down," said Michael Mata, manager of the ING Global Bond Fund (INGBX) in Atlanta .

So how much further could rates fall?

Mata said he would not be surprised if rates dropped to around 2.75% in the next few months. He said that if the economy continues to weaken, they could go as low as the 2.4% to 2.5% level they were at last fall before the Fed finally made QE2 official in November.

Collins is even gloomier. He said that the financial crisis lows of about 2% from December 2008 are not out of the question if the economy doesn't pick up soon. But all things considered, he said a 10 Year yield of 3% is fair assuming the economy muddles along without taking a significant turn for the worse.

Still, will any of this actually help consumers? Low rates should be a blessing. That's the reason the Fed did QE and QE2 in the first place. But Collins said that is not enough to get the economy back on track.

"Low rates in of themselves have not spurred economic activity, lending or borrowing," Collins said. "Mortgages have been near record lows for a while and there has been little refinancing or new home purchases."

So as long as the bond market is keeping rates artificially low, don't look for the Fed to try and drive them down even further with QE3.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: