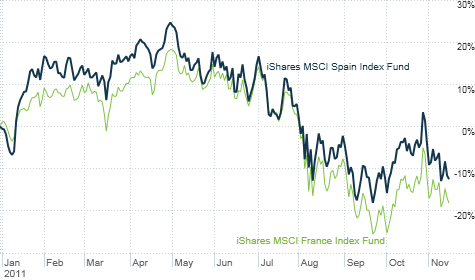

Europe's debt problems are spreading, with investors now worried about the health of France and Spain. Exchange-traded funds tracking the markets of both countries have plunged.

NEW YORK (CNNMoney) -- Next up on the 2011 Europe Financial Calamity tour? Spain and France.

Yes, government bond yields in Italy are still climbing -- even after the resignation of Silvio Berlusconi. With the Italian 10-year back above 7%, it's clear that investors are still very nervous about the debt problems in Europe's boot.

But perhaps more alarming is the fact that the market is now increasingly wary of Italy's Mediterranean neighbors as well.

Yields on Spain's 10-year bond have climbed to about 6.3%. That's dangerously close to the 7% level that many investors feel could signal the need for a Spanish bailout.

And France's bonds are starting to look like French toast. With yields now around 3.67%, that puts the "pain" in pain perdu. (Yes, I watch Top Chef.)

Two exchange-traded funds tracking Spanish and French markets -- the iShares MSCI Spain Index Fund (EWP) and iShares MSCI France Index Fund (EWQ) -- have been hit hard in the past few days. Shares of big Spanish banks BBVA (BBVA) and Banco Santander (STD) have tumbled as well.

The verdict from the experts I spoke to: Unless the European Central Bank steps up to the plate with a real plan to stop the bleeding, Europe will keep bleeding.

"The market keeps looking ahead to the next potential victim in Europe," said Jurgen Odenius, chief economist for Prudential Fixed Income in Newark, N.J. "Volatility is rising because there is no comprehensive, credible solution. It's becoming readily apparent that there's only one game in town, an ECB rescue."

Odenius said he doubts that Europe will be able to convince China and other global sovereign wealth funds to put up enough capital to increase the leverage of the European Financial Stability Facility bailout fund. That means the ECB may have to be the proverbial lender of last resort.

If the ECB does not take more bold action -- namely a strong commitment to keep buying more sovereign debt -- Odenius thinks Spanish yields may soon hit 7% like in Italy. And if that happens, France could also be in serious trouble.

"The French have problems in their banking system related to Italy, Spain and other countries. Investors are not suggesting that France is a crisis just yet, but it is murky," he said.

Michelle Gibley, senior market analyst with the Schwab Center for Financial Research in Denver, agreed. European leaders need to bust out a "bazooka" to deal with the debt crisis, she said.

That's a reference to the term that former Treasury Secretary Hank Paulson used in 2008 in response to questions about whether the United States would need to save floundering mortgage agencies Fannie Mae and Freddie Mac.

The implication was that the mere presence of said bazooka in his pocket meant that Paulson would not have to fire it. But as we all know, he eventually did. Fannie and Freddie were taken over by the government.

But the problem facing Europe right now is that leaders haven't even acknowledged they have a big financial weapon, let alone talk about a willingness to use it.

"I am concerned that European policy makers have yet to find the bazooka," Gibley said. "The crisis is rolling from one nation to the next. The contagion has not been contained."

Her biggest worry is that European governments are simply choosing to focus on austerity to deal with their fiscal problems. But while budget cuts, higher taxes and more responsible spending can help cut onerous debt loads, such actions do nothing to help stimulate their economies.

"The debt crisis is now potentially entering a dangerous cycle where austerity just reduces growth, borrowing costs continue to rise and credit ratings get downgraded. That's because nobody is addressing growth," Gibley said. "How much more turmoil does there need to be before the ECB does more?"

Still, the news in Europe is not all bad. Stuart Rosenthal, CEO of Factor Advisors in New York, notes that yields in Germany, Sweden and the Netherlands are still lower year-to-date.

But that may just show that the recent sell-off in French and Spanish bonds is not an irrational panic. Investors are adept at identifying winners and losers in Europe. The problem is that the number of losers is rapidly growing.

After all, yields on French bonds had been lower than where they started 2011 as recently as last week. Yields on Spanish debt were below 5% in early October. Sentiment has a funny way of changing on a dime.

"The contagion fears are not overblown. The bond market is pressing the Europeans for action," said Paul Christopher, chief international strategist with Wells Fargo Advisors in St. Louis. "They want the ECB to backstop European debt. That's why France and Spain are being targeted."

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: