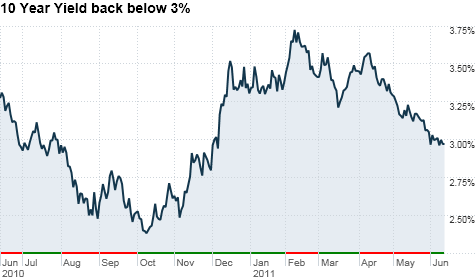

With interest rates already this low, is QE3 really necessary? Click the chart for more on bonds.

NEW YORK (CNNMoney) -- The Federal Reserve meets next week to discuss monetary policy.

Investors will be watching for any clues about what the central bank plans to do now that its controversial bond purchasing program is about to wind down at the end of the month -- just as the economy has hit a rough patch.

But for those who are holding out hope that the Fed will use the recent market sell-off as an excuse to instantly start up yet another Treasury buying binge, then -- in the immortal words of Judas Priest -- you've got another thing comin'.

Late last summer, Fed chairman Ben Bernanke made the case for the so-called QE2 program (the bulk of the first round of quantitative easing took place in late 2008 and 2009 and wound up totaling $1.8 trillion) because he was worried about deflation.

Bernanke used the D-word six times in an August speech at a Fed conference in Jackson Hole, Wyo. that was widely considered to be Bernanke giving his blessing to QE2.

The Fed wanted inflation. It got inflation. The $600 billion in new bond purchases through QE2 has been one reason why the dollar has weakened and commodity prices have surged.

Consider that oil prices were hovering around $75 a barrel just before Bernanke tipped the markets off that QE2 was coming. Today, crude is near $100 a barrel. And prices went as high as about $115 at the height of Arab Spring supply disruption fears earlier this year.

Food prices are rising as well as commodities, ranging from coffee and sugar to corn and wheat, which have all soared.

Consumers are starting to feel the pinch. According to inflation figures for April released by the government, consumer prices rose 3.2% in the past 12 months. That's the highest year-over-year increase since October 2008.

The Consumer Price Index for May will be released Wednesday morning. If the year-over-year increase in overall prices remains above 3%, that could give the Fed's inflation hawks enough evidence to fight Bernanke and more dovish members who may want to push through QE3.

So even though the job market and housing market still stink, it's highly unlikely that the Fed will rush to launch a third round of bond buying.

That's because the first iteration of quantitative easing and its sequel QE2 (which has gotten reviews more like "The Hangover Part II" than "The Godfather Part II") were never about jobs and lending in the first place.

Sure, the Fed talks a good game about wanting to keep interest rates low to stimulate the economy.

But despite QEs Uno and Dos, banks have not really eased credit standards for creditworthy consumers and small businesses.

Interest rates are already super low, with the 10-year Treasury yield below 3%. How much further does the Fed want to drive rates down? It's not as if a 10-year yield at 2.5% is going to all of a sudden spark huge demand for mortgages.

And companies still seem more willing to use all the cash they've got sitting on their balance sheets -- which is earning next to zilch thanks to Fed policies by the way -- on mergers, stock buybacks and dividends. They are not using cash to hire enough workers to make a noticeable dent in the unemployment rate.

"The problem is there have already been two rounds of quantitative easing and the increased liquidity the Fed has injected is not helping the job market," said Andrew Fitzpatrick, director of investments with Hinsdale Associates in Hinsdale, Ill.

I realize that the housing crisis could be viewed as a deflationary threat -- as my Fortune colleague Colin Barr astutely points out. (Read "How the housing depression spells QE3.")

And the pathetic job market is also not ringing any inflation alarm bells either. As long as wage growth remains stagnant, inflation in a classic economic textbook sense won't rear its ugly head.

But the Fed has to be careful to not overreact and break a bottle of champagne across the hull of QE3 until it's clear that the overall economy is actually in the midst of a sustained slowdown and not just a quarter or two soft patch.

I've said it before and will say it again. This looks like a continuation of a sluggish BBQ recovery, i.e. low and slow. That's not the same thing as a double-dip recession.

"One month does not make a trend and more instances of sub-100,000 job creation would be needed to conclude that QE3 would be warranted," wrote Pierre Lapointe, global macro strategist with Brockhouse Cooper, a brokerage in Montreal, in a report Monday.

Lapointe added that "the deflation threat is also significantly reduced, if not gone altogether, and inflation will continue to creep up over the coming months in our view. This makes the prospect of QE3 unlikely."

Make no mistake. The Fed probably won't sit idly by if the economy continues to stall. But more bond buying might not be the answer.

At a bare minimum, the Fed will keep interest rates near zero -- where they have been since December 2008 -- for the foreseeable future.

"I think at some point if the data continues to worsen, the Fed will have to do something," Fitzpatrick said. "The Fed may not call it QE3 but there will be more tools to get implemented. It's likely there will be more stimulus."

The Fed may even try new programs that could more directly impact job creation. Garett Jones, an economics professor with the Mercatus Center at George Mason University, argued that the Fed could cut, or even outright eliminate, interest payments on excess bank reserves as a way to get financial institutions to lend more.

Jones argues that banks have no financial reason to lend out excess reserves as long as they get paid to sit on that cash. But if banks no longer are rewarded for being misers and actually lend more, particularly to small businesses, that could help stimulate job growth.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates:

| Latest Report | Next Update |

|---|---|

| Home prices | Aug 28 |

| Consumer confidence | Aug 28 |

| GDP | Aug 29 |

| Manufacturing (ISM) | Sept 4 |

| Jobs | Sept 7 |

| Inflation (CPI) | Sept 14 |

| Retail sales | Sept 14 |