Click the chart for more on bonds

NEW YORK (CNNMoney) -- Inflation fears are everywhere these days thanks to surging commodity prices.

You're even starting to hear some experts talk about stagflation, a phenomenon that, much like disco and bell bottom pants, would be better off remaining a relic of the 1970s.

But the bond market isn't falling for the inflation talk. Yes, commodity prices are, to quote perennial New York state political candidate and YouTube star Jimmy McMillan, "too damn high." And that's starting to impact wholesale prices and consumer prices.

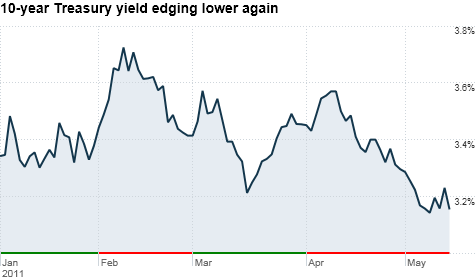

That isn't the same thing as inflation though. Inflation is usually the byproduct of a strong economy, particularly one where wages are growing rapidly. That's not happening now. And that's why the yield on the U.S. 10-year Treasury note is still a very low 3.16%.

Bond prices and rates move in opposite directions. Yields tend to go up when the economy is robust. That's because there is less incentive to buy stodgy Treasuries at a time when riskier assets like stocks look more rewarding.

So the fact that bond yields are still a lot closer to 3% than 4% shows that fixed-income investors are still nervous about the economy, a stark contrast to stock market investors who have a gung ho approach thanks to strong earnings

"The bond market doesn't seem to be worried about inflation but bond investors seem to be apprehensive about the economy," said John Kosar, director of research with Asbury Research in Chicago. "That's not a good sign. In general, the bond market is the one that tends to get it right."

The allure of U.S. bonds as proverbial safe havens also seems to have increased thanks to the latest debt woes in Greece and other parts of Europe. Fund tracking firm EPFR Global reported Friday that U.S. bond funds had their highest inflows of the year this past week.

Whether or not bond yields continue to remain this low after the Federal Reserve's second round of quantitative easing, a bond buying binge more commonly referred to as QE2, ends next month is an open question.

Some worry that rates will shoot drastically higher because the Fed will no longer be a buyer of last resort keeping yields as low as they have been.

But James Barnes, senior fixed income portfolio manager with National Penn Investors Trust Company in Reading, Pa., said he thinks the end of QE2 won't cause a massive spike in long-term rates.

Barnes said the 10-year yield could climb as high as 3.75% by the end of the year. While that would be noticeably higher than where rates currently are, they would still be pretty low by historical standards. And he thinks the move to 3.75% will be a steady grind up, not a dramatic pop.

It all comes back to the notion that the bond market just doesn't believe the inflation hype and is far more worried about the economy stalling.

Barnes said the only reason for rates to go higher is if inflation picks up -- and that will happen if the job market improves, not because of what's going on with oil and other commodities.

"It's all about the employment data. As the jobs picture gets better, rates should trend higher," he said.

Anthony Valeri, fixed income strategist with LPL Financial in San Diego, agreed. He said that rates could go as low as 3% before finally bottoming, but the economy will have to slow down much more in order for rates to slip below 3%. He thinks rates will end the year between 3.5% and 4%.

Again, that's not all that high, relatively speaking. Valeri said that's because the bond market is focusing more on the negatives tied to higher oil prices than the stock market currently is.

"The only inflation right now is in commodities and the bond market is thinking that companies won't be able to pass on all those costs to consumers," Valeri said. "That would be a negative for profit margins and the economy."

Still, some stock investors do seem to realize that super-low rates are a hint that the economy is weakening. Investors have been moving into more defensive stock sectors that tend to do better in a slower economy.

Healthcare stocks, for example, have been among the better performers this year. Consumer staples and utility stocks are also picking up steam.

Those sectors, in addition to being safer bets in an uncertain economy, also are areas that investors starving for steady income payments often flock to when bond rates are so low.

"It's hard to like fixed income. Why buy bonds when you can get a 3.5% dividend yield from many blue chip stocks," said James Denney, portfolio manager with Mohawk Capital Management in Schenectady, N.Y.

But investors can take solace that low interest rates aren't completely a worrisome sign. Valeri said most fixed-income investors think that there will be an agreement to raise the debt ceiling before the end of the summer.

Valeri said if the bond market was truly concerned that Congress won't let the Treasury Department borrow more, investors would be panicking and rates would be much higher than they are now, kind of like they are in Greece and other countries with truly onerous debt burdens.

"The bond market has confidence that the debt ceiling debate will be resolved," he said. "Nobody is selling Treasuries because of this."

Reader comment of the week. First off, I'm thrilled to see that our new Disqus comments pages look like a big improvement (i.e. less spam) than Facebook Connect. (Hopefully Facebook won't now hire a big PR firm to run a smear campaign against me because I just trash-talked them. Did you know that Paul R. La Monica hates puppies and sunlight?")

As for the comments, there were many great ones about Cisco (CSCO, Fortune 500). I previewed their earnings in Tuesday's column. The earnings turned out to be good but as I expected, the guidance was terrible. Several readers pointed out how boring food distributor Sysco (SYY, Fortune 500) has been a better stock than Cisco.

But someone using the name of massmedia on Disqus had my favorite comment. He referred to another Cisco/Sysco soundalike who we haven't heard from in awhile: R&B singer Sisqo.

"Ever since Cisco released the 'Thong Song', it's been downhill from there :P"

I don't know about you. But the thought of John Chambers singing "That thong thong thong thong thong!" just made my day.

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: