Click chart for more stock market data.

NEW YORK (CNNMoney) -- Next week all eyes will be on inflation and Greece.

Markets dropped sharply Friday as rumors of a possible Greek default circled the globe. The default could come as early as this weekend. Whether or not something happens in Greece will largely rule market sentiment as the market opens in New York Monday.

"I think if we don't hear anything on Greece, there could be a relief rally on Monday," says Sam Ginzburg, head of capital markets at First New York.

Investors sold stocks Friday in fear that Athens may not get its next installment of bailout money from the European Union, International Monetary Fund and European Central Bank and that the bankruptcy could come to light over the weekend.

Meanwhile investors continue to cling to any reading on the fragile state of the economy. On Thursday, the Commerce Department will release the consumer price index, the government's main inflation gauge.

The CPI index will be the final reading on inflation ahead of the two-day meeting of the Federal Reserve beginning September 20. Investors are betting that if the U.S. economy shows evidence of deflation, the Fed may be more willing to take steps to shore up the economy.

Investors could bid up stock prices if they expect the Fed to introduce another round of bond buying, or so-called QE3, after the meeting. According to minutes from the previous Fed meeting, the three so-called inflation doves dissented against Fed intervention because the U.S. economy showed signs of a healthy rate of inflation.

"The market wants to handicap every event so they might take any indication of deflation or no inflation as a sign that dissent within the Fed won't be significant," says Clark Yingst, chief market analyst at Joseph Gunnar.

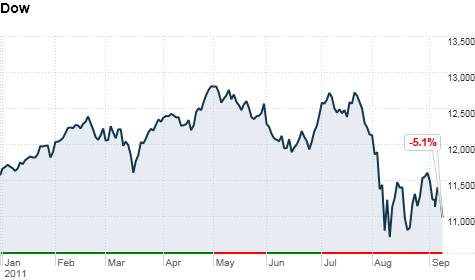

Stocks ended sharply lower Friday, as bad news out of Europe kept piling up. The day's steep losses pushed all three indexes to end in the red for the week. The Dow declined more than 2%, the S&P fell 1.7% and the Nasdaq slipped 0.5%.The sell-off triggered the sixth weekly decline in seven weeks for the Dow and S&P 500.

One thing investors should bet on: continued volatility. "The market is in a really binary situation. Investors think the world is going to get better or worse," says Ginzburg. "Macro factors and psychology are the most important factors for investors right now and are more important than the fundamentals of any one company."

Monday: Investors will anxiously await Bank of America (BAC, Fortune 500) CEO Brian Moynihan's 9 a.m. presentation at the Barclays investors conference in New York for any insights into the bank's plans.

Tuesday: A report on August's import and export prices is due in the morning.

Big-box retailer Best Buy (BBY, Fortune 500) will report quarterly earnings before the opening bell.

Wednesday: The Producer Price Index, a measure of wholesale inflation, is due out from the Commerce Department ahead of the opening bell. The index is expected to have stayed the same in August after rising 0.2% in July. The so-called core PPI, which strips out volatile food and energy prices, is expected to have risen 0.2% after increasing 0.4% the previous month.

Economists expect the Commerce Department to report that retail sales rose 0.2% in August after a 0.5% rise the previous month, according to consensus estimates gathered by Briefing.com. Sales excluding volatile autos are expected to have ticked up 0.3%.

The July reading on business inventories, due from the government later in the morning, is likely to show an increase of 0.5%.

Thursday: The U.S. consumer price index is expected to show that prices rose 0.2% in August, after rising 0.5% the previous month. Economists expect consumer prices excluding food and energy to inch up 0.2%, matching July's uptick.

The government's weekly report on initial claims for jobless benefits is expected to drop to 410,000, from 414,000 the previous week.

The Empire Manufacturing survey is also due before the start of trading. The regional reading on manufacturing is forecast to have risen to negative 4 in September from negative 7.7 in August, according to consensus estimates from Briefing.com.

Government data on industrial production and capacity utilization for August are also due before the market opens.

Also out at 10 a.m. ET in the morning is the Philadelphia Fed index for September, a regional reading on manufacturing. The index is forecast to fall to negative 10, up from negative 30.7 the previous month.

BlackBerry maker Research in Motion is scheduled to report earnings after the markets close.

Friday: Shortly after the opening bell, the University of Michigan will put out its initial reading on consumer sentiment in September. Economists expect the figure to move slightly higher to 56.3 up from 55.7. ![]()

| Index | Last | Change | % Change |

|---|---|---|---|

| Dow | 32,627.97 | -234.33 | -0.71% |

| Nasdaq | 13,215.24 | 99.07 | 0.76% |

| S&P 500 | 3,913.10 | -2.36 | -0.06% |

| Treasuries | 1.73 | 0.00 | 0.12% |

| Company | Price | Change | % Change |

|---|---|---|---|

| Ford Motor Co | 8.29 | 0.05 | 0.61% |

| Advanced Micro Devic... | 54.59 | 0.70 | 1.30% |

| Cisco Systems Inc | 47.49 | -2.44 | -4.89% |

| General Electric Co | 13.00 | -0.16 | -1.22% |

| Kraft Heinz Co | 27.84 | -2.20 | -7.32% |

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates: