Although the yield on the 30-year Treasury is already low, some think the Fed should consider pushing them lower with a new version of "Operation Twist" -- a program from the 1960s.

NEW YORK (CNNMoney) -- The Federal Reserve may have one last thing it can do to help stimulate the economy that wouldn't necessarily be considered "treasonous" by a certain presidential candidate.

Time for Ben Bernanke to put on his dancing shoes?

With the global financial markets convulsing yet again, some experts are suggesting that the Fed could try and calm things down by bringing back a tool it used in the 1960s called "Operation Twist."

That name was partly a reference to the popular dance craze and hit Chubby Checker tune. But it also was a description of what the Fed wanted to do: twist the so-called yield curve by selling short-term bonds and buying longer-term securities. That would bring short-rates up and long-term rates down.

Of course, the Fed already tried something similar late last year with a second round of quantitative easing, a program to buy bonds that was dubbed QE2. In fact, the San Francisco Fed published a paper earlier this year comparing QE2 to Operation Twist.

While many Fed critics have blasted QE2 for failing to help the economy, it's still telling that some on Wall Street are desperately hoping the Fed will soon try something else.

After all, Congress has proven itself to be unwilling to address short-term economic problems. And Europe is a cluster-(word that rhymes with truck).

That leaves the Fed. And despite the fact that it has pledged to just sit tight and leave short-term rates near zero until 2013, some experts don't think Bernanke and Co. will really remain so passive. Hence, the calls for Operation Twist. But why now? Besides the whole markets imploding thing?

Well, Bernanke prepared the market for QE2 last August during a speech at the Kansas City Fed's annual econopalooza in Jackson Hole, Wyoming.

Guess what? Bernanke speaks at Jackson Hole Friday. So it's no wonder that some investors are hoping that Bernanke will twist again like he did last summer. (I'd watch Bernanke, Dallas Fed president Richard Fisher and others take part in "Dancing with the FOMC Stars!")

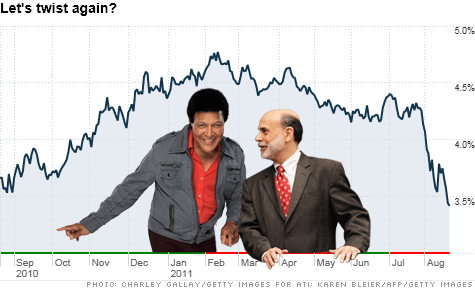

How could a new Operation Twist (perhaps renamed Operation Dougie to bring it into the 21st century) work? The Fed could specifically target the 30-year Treasury. The 30-year currently yields about 3.4%.

While that's down from about 4.3% when this recent bout of market volatility began in late July, the spread (or difference) between it and the 10-year Treasury yield is still fairly wide. The 10-year yield is about 2.1% now (having briefly dipped below 2% Thursday). The 10-year was at 3% a few weeks ago.

And some bond experts argue that the spread between the 30-year and the shortest of short-term bonds, the 3-month bill, is most problematic. Typically, if the difference between the 30-year and 3-month is above 3%, that's a bad sign for the economy. Right now, the 3-month bill yields practically nothing. It's just 0.01%.

So a new Operation Twist could help bring short-term rates up and the 30-year down.

And an advantage to another Operation Twist -- as opposed to a QE3 -- would be that the central bank could technically buy bonds without having to increase its balance sheet. It could just sell a certain amount of short-term debt and buy the equivalent amount of long-term debt.

But would bringing down long-term rates actually do anything to help the economy or would it just be a ploy to satisfy investors who can't get enough Fed liquidity? Sadly, probably just the latter.

It's hard to imagine how even lower long-term rates will boost growth. Mortgage rates are already at record lows. But that doesn't do anyone good when banks are tightening credit and consumers are scared to buy houses anyway because of falling prices.

"The fact that the 30-year is where it is now has nothing to do with the Fed. It's the economy," said John Lekas, CEO of Leader Capital in Portland, Ore. "Housing prices have gotten lower. Banks won't lend money until prices start going up."

Lekas does think that a stabilization process is slowly taking place in housing though. So he believes the Fed should not try and push rates any lower. Instead, it should let the market sort things out --- as painful as that may be.

"We may be getting to a real natural bottom. It just takes time," said Lekas, who manages the Leader Total Return Fund and Leader Short Term Bond Fund. "Hopefully the message from Bernanke at Jackson Hole will be no message."

But can Bernanke really get away with a speech that doesn't present a plan? It depends. If the market insanity (inanity?) extends into next week, it may be impossible for Bernanke to ignore growing comparisons to a few years ago.

"The bar for QE3 or anything else should be a lot higher. There will need to either be a full blown market collapse or worries that a major bank has to be nationalized," said Graham Summers, chief market strategist with Phoenix Capital Research in Charlottesville, Va. "But it is more likely that we could have a 2008-like event."

Bernanke has time and time again shown he is willing to step in when the markets appear to be this close to falling into the abyss. So the chances seem to be growing that he will say something significant at Jackson Hole -- even if he shouldn't.

"I don't think the Fed is going to give up," said Paul Simon, chief investment officer of Tactical Allocation Group in Birmingham, Mich. "But I do think the Fed should get out of the way."

"In fact, if the Fed did do another Operation Twist, they can make things worse," Simon added. "There is very little to be gained and the risk could be massive inflation."

Reader comment of the week. HP stands for Hewlett-Packard. But I joked over on Twitter that it should stand for Help Please!

The stock is getting killed Friday after disclosing that it may dump its PC unit, is killing off its smartphone and tablet business (a year after inheriting it from Palm) and spending more than $10 billion to buy software firm Autonomy.

The fact that HP is now on its third CEO in ten years and that he is making some of the same stumbles as his predecessors is not lost on one savvy reader.

"If $hpq executive staff doesnt want to be lynched by a mob of shrhldrs, they'd be wise to stop the purposeless spending sprees," tweeted @DayTradinShrink. "$hpq made same mistakes as palm. Why execs are allowed to run rampant like this still surprises me. board has explainin' to do."

The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

| Overnight Avg Rate | Latest | Change | Last Week |

|---|---|---|---|

| 30 yr fixed | 3.80% | 3.88% | |

| 15 yr fixed | 3.20% | 3.23% | |

| 5/1 ARM | 3.84% | 3.88% | |

| 30 yr refi | 3.82% | 3.93% | |

| 15 yr refi | 3.20% | 3.23% |

Today's featured rates:

| Latest Report | Next Update |

|---|---|

| Home prices | Aug 28 |

| Consumer confidence | Aug 28 |

| GDP | Aug 29 |

| Manufacturing (ISM) | Sept 4 |

| Jobs | Sept 7 |

| Inflation (CPI) | Sept 14 |

| Retail sales | Sept 14 |